China’s coal spending boom contrasts with industrial slump

While China’s industrial sector crashes, one corner is booming. Oddly enough, it’s probably bad news for participants.

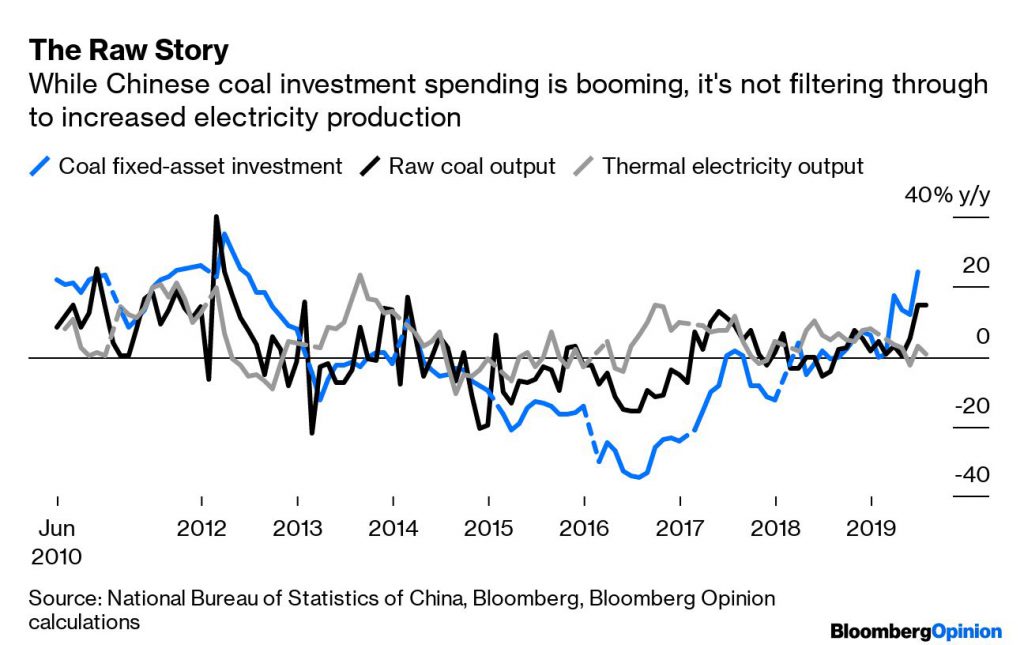

Fixed-asset investment in mining increased 27.4% from a year earlier in July, continuing an extraordinary run this year that puts growth at the fastest pace in a decade. One commodity is likely to have dominated: Investments in mining and preparing coal have been growing at double-digit rates so far this year, in contrast to contractions in the other major mined commodity, ferrous metals.

That’s odd, because the mood-music for coal hasn’t been so hot. Cargoes at the port of Qinhuangdao with 5,500 kilocalories per kilogram have fallen to 576 yuan ($82) a metric ton, nearing their lowest levels in three years, and stockpiles at major generators have mounted as seasonal floodwaters boosted China’s hydro generation. At Australia’s Newcastle port, one of the main export harbors for Asian soot, 5,500 kcal coal is down 17% on the year.

How to explain so much money chasing such a weak market?

One answer lies in one of President Xi Jinping’s favorite terms, zili gengsheng or “self-reliance.”Xi has used the term repeatedly in official speeches and visits as the trade war with the U.S. has intensified over the past year, to stress the importance of local industry being self-sufficient and not depending too heavily on imported goods and materials.

You can see how that’s played out in difficulties reported by coal importers getting their product through Chinese customs so far this year. The main suppliers to China have historically been Indonesia, Australia and Canada, none of which are particularly sympathetic to Beijing in the current trade conflict. It shouldn’t be surprising that Russia has seen the biggest increase in import trade, or indeed that China seems determined to use investment spending to build its domestic output to the point where it barely needs imported carbon.

China has been restructuring its coal sector for years, and the efforts may only now be starting to bear fruit. Raw coal output was lackluster throughout 2018 and picked up only fitfully earlier this year, but in June it was 333 million tons, posting the fastest growth from a year earlier since 2014. With investment still flowing into the sector at a furious rate, it wouldn’t be surprising if that pace is sustained over the coming months.

That’s a worrying result for the global climate, given that China accounts for more than a quarter of global carbon emissions. On the other hand, there’s reason not to be too despondent. It’s possible that most of the fixed-asset investment is being spent on washing and upgrading low-quality raw coal to make a product that produces fewer smokestack emissions. That would explain the disconnect between strong investment and raw coal output and China’s weak industrial performance and thermal-fired electricity demand, which don’t appear to be demonstrating increased usage.

Miners who depend on exports to the country should be on notice, though. So far this year they’ve been hit by hold-ups at ports but have benefited from a market where China’s local coal prices are far higher than those of seaborne product. Should a flood of domestic supply wipe out that price differential, the current dismal conditions for the seaborne trade will look like a picnic.

(By David Fickling)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments