Canadian diamond discoveries could close pending supply gap

Story by Paul Zimnisky of Diamond Analytics

On November 1st, De Beers said that it will be closing its nearly depleted Victor diamond mine in northern Ontario in early 2019. Victor is the first in a line of legacy diamond mines world-wide that will be closing over the next 5-years.

Most notably, Rio Tinto’s illustrious Argyle mine in Australia is expected to shut operations in 2021. At peak production, in the mid-90’s, Argyle produced over 40M carats annually. To put that into perspective, total 2017 global diamond output is estimated at less than 150M carats.

De Beers Voorspoed mine in South Africa is on pace to reach end-of-life by the end of the decade, and a slew of the company’s alluvial mines in Namibia are planned to be phased out by 2022.

With global diamond demand forecast to grow at approximately 3.5% annually over the next five years, driven by middle class consumers in Mainland China and India, the industry’s fastest growing large markets, a supply gap down the line seems inevitable if forecasts hold.

Globally there only two new diamond projects in the works with annual production potential of in excess of 1M carats, one in Angola, the other in Russia. Further, new diamond project exploration has been limited by challenges in the upstream diamond industry’s primary jurisdictions.

Greenfields diamond exploration in South Africa is at multi-decade lows due to delays in granting of prospecting licenses and perceived risks of a new Mining Charter, and this year there was a production disruption at the Williamson diamond mine in Tanzania related to government changes in mining legislation.

In Botswana, home to De Beers’ primary asset base, the country has been heavily explored and most major diamond discoveries are assumed to already have been made. In Russia, most major diamond production in is controlled by government entities.

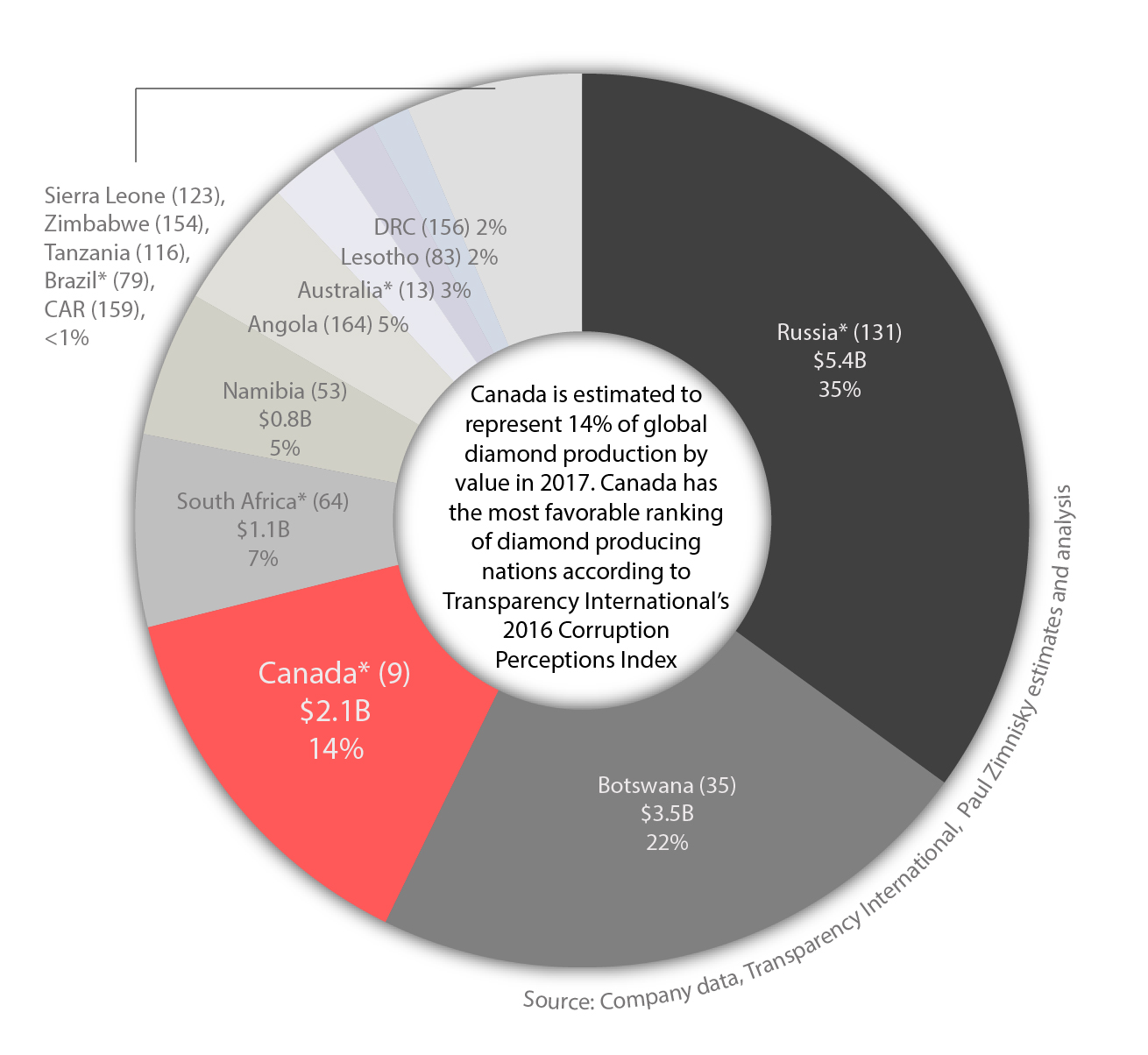

Estimated global diamond production by nation in value in 2017. Total 2017 global diamond production estimated at $15.6 billion. Source: Paul Zimnisky

Notes: Asterisk notes G20 nation. Number inside parenthetical notes country’s ranking in Transparency International’s 2016 Corruption Perceptions Index (1-“very clean”, 176-“highly corrupt”). Dollar figure is estimated 2017 value of diamond production by nation. Percent figure is nation’s estimated contribution to global diamond production by value in 2017. All figures in USD.

This makes Canada, already the third largest diamond producing nation in the world by value (see chart above), arguably the most prospective diamond exploration jurisdiction in the world. In May of this year, Canada’s leading diamond producer, Dominion Diamond (private), pledged to spend C$50M on exploration over next 5 years, the company’s first major greenfields exploration since 2007.

After being acquired for US$1.2B in July by private-held the Washington Companies (at a 44% premium to where the stock was trading the day before initial indication of interest was made), on November 1st Dominion reiterated plans of “reinvigorating” exploration programs in Canada.

Dominion is partnered with North Arrow Minerals (TSX-V: NAR) on the prospective “Lac de Gras” property, which is located within a diamondiferous kimberlite field in the Northwest Territories that is the source to some of the richest diamond deposits in the world, including Dominion’s two world-class mines, Ekati and Diavik.

Dominion’s partner is known for making 2 of the only 5 kimberlite discoveries made in Canada over the last 5 years, and both of North Arrow’s discoveries were diamond bearing. Just last month North Arrow announced a discovery at the company’s 100%-owned Mel project in in the Nunavut territory of Canada. The company has plans to set up an exploration camp and drill the property next year.

Mel is approximately 200km northeast of the North Arrow’s 100%-owned Naujaat property which already has an inferred resource of over 26M carats and contains fancy yellow and orangey-yellow diamonds. In September, the company completed a C$2M drilling and mini-bulk sampling program at the property with results expected in the coming months. North Arrow also has pending results from a till sampling program at its Pikoo project, a 100%-owned diamond bearing kimberlite project in Saskatchewan that was discovered by North Arrow in 2013.

This coming March, Dominion will lead a drill program at the aforementioned Lac de Gras joint-venture (69% Dominion/31% North Arrow) in hopes of discovering new diamondiferous kimberlites. At around the same time North Arrow will also be drilling at its 100% owned Loki project, also in the Northwest Territories, and approximately only 30-40km away from both Ekati and Diavik.

With active programs across multiple worthy projects in Canada’s premier diamond territories, North Arrow appears well positioned to add to previous success and maintain its status as Canada’s leading publicly-traded stand-alone diamond explorer.

Disclosure: Paul Zimnisky has been compensated by North Arrow Minerals to produce the above content. The content includes views that are based on observations and opinions. The author has made every effort to ensure the accuracy of information provided, however, accuracy cannot be guaranteed. The above content is strictly for informational purposes and should not be considered investment advice. Consult your investment professional before making any investment decisions. None of the parties involved accept culpability for losses and/or damages arising from the use of content above.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments