BHP’s costs crash diet is running out of steam: David Fickling

Going on a crash diet seems great while you’re shedding the pounds. The problem is sticking with it for the long term.

That’s what seems to be happening to the world’s miners, which have spent the years since the commodity boom peaked in 2011 holding down salaries, eking out efficiencies and extracting the highest-quality parts of their deposits to keep costs in line with deflating prices.

The cycle looks to be turning, though: Controllable cash costs at BHP Billiton Ltd. rose by $1.24 billion in the year through June, the company reported Tuesday, mainly because of declines in oil and gas fields, operational problems at two coking coal mines and issues around processing costs at two copper mines. That was enough to overwhelm the $1.02 billion gain to Ebitda from higher volumes at the company’s two biggest operations, the Escondida copper mine and its Australian iron ore business.

BHP isn’t alone in this. At Rio Tinto Group, operating costs in the six months through June rose $392 million from a year earlier, owing in large part to the increasing price of raw materials for its aluminum business such as caustic soda and petroleum coke. Copper miner Antofagasta Plc saw unit costs rise more than 20 percent in the first half as reduced volumes pushed operations closer to their fixed-cost base.

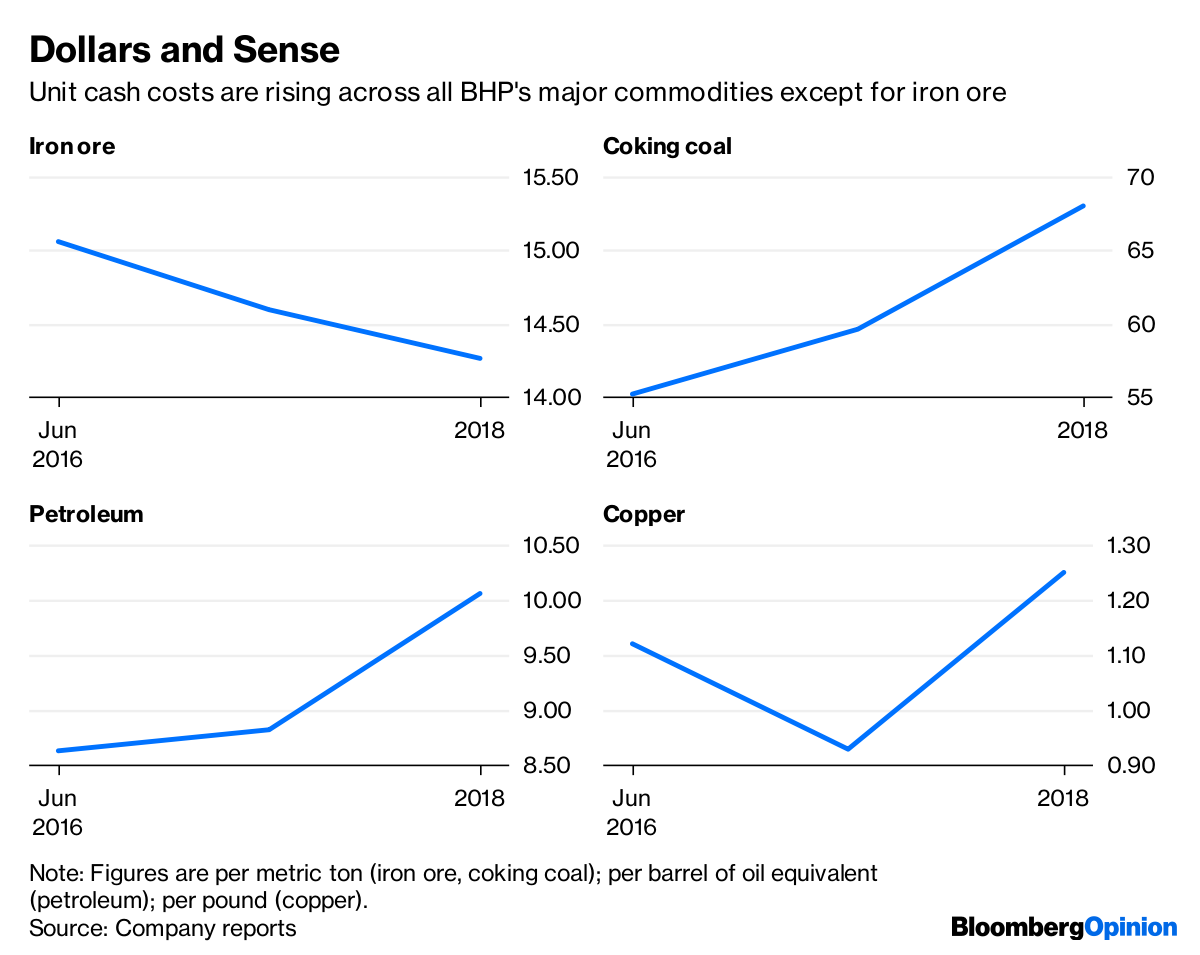

Still, BHP’s weakness looks notably broad-based. Across its four major commodities – iron ore, coking coal, petroleum and copper – costs were only in decline at the iron ore unit, and even there they faced a headwind from the strength of the U.S. dollar, which raises the costs of dollar-denominated equipment and fuel. At Escondida, where BHP has spent billions bringing water up to the Atacama desert and trying to offset declining concentrations of copper in its ore, costs came in at $1.25 a pound, well above the ranges around $1 a pound the company forecast with first-half results in February.

Some of this is just a matter of bad timing. The fixed element of mining costs doesn’t change much, regardless of how many tons are being produced, so the declines in output from mines such as the Olympic Dam copper pit and the Broadmeadows and Blackwater coking coal operations in Australia pushed up the average. Mostly, such shutdowns are a chance to improve performance, so they should result in better cost performance once they’re in the past.

Some of this is just a matter of bad timing. The fixed element of mining costs doesn’t change much, regardless of how many tons are being produced, so the declines in output from mines such as the Olympic Dam copper pit and the Broadmeadows and Blackwater coking coal operations in Australia pushed up the average. Mostly, such shutdowns are a chance to improve performance, so they should result in better cost performance once they’re in the past.

“We’ve consistently said that productivity gains will be lumpy,” Chief Executive Officer Andrew Mackenzie told an analyst call Tuesday, “and in 2018 that’s been evident.”

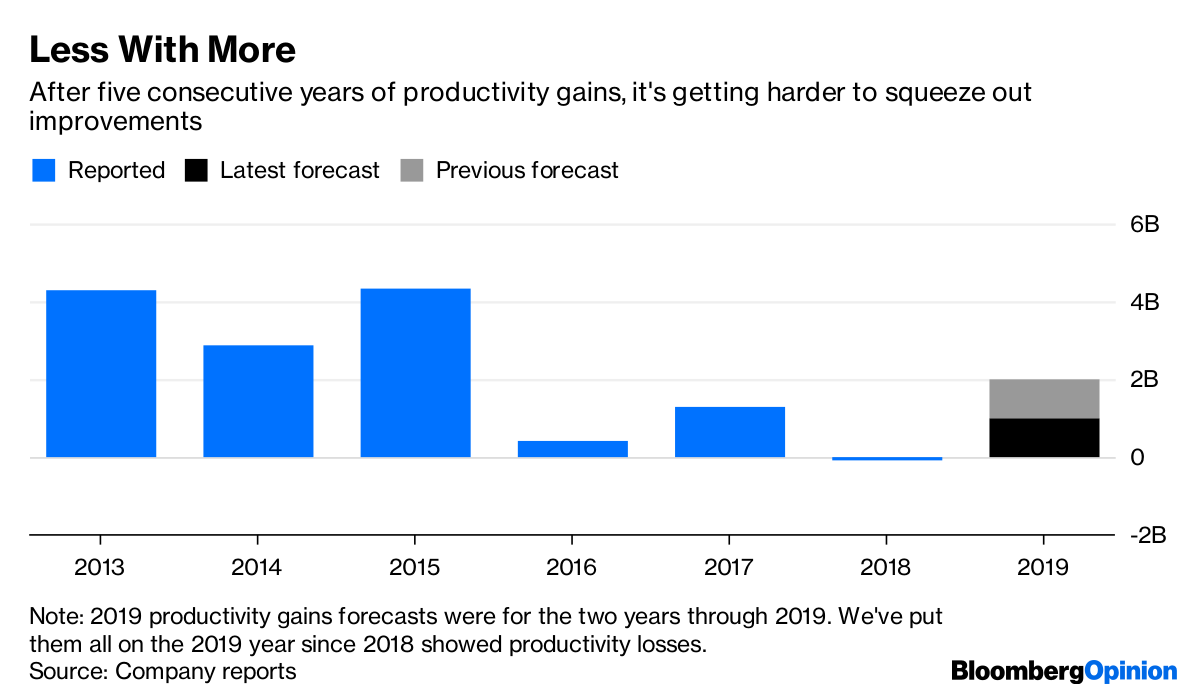

Still, there’s evidence too of deeper issues. Productivity decreased to the tune of $96 million during the year, and gains in 2019 will only come to $1 billion rather than the $2 billion previously forecast, according to BHP. Unit costs for coking coal, iron ore and thermal coal will be stuck more or less in line with the 2018 result over the next 12 months, and will rise further for petroleum. At Escondida, which has been aiming at costs around $1 a pound, the medium-term forecast is now $1.15 – and the drumbeat of labor unrest remains a perpetual threat. Energy costs, which have generally contributed to earnings or only slightly reduced them in recent years, sucked $224 million out of Ebitda as diesel prices rose.

As we’ve argued before, in many ways the world’s mining companies are in rude health. Profits at BHP are at their highest level in four years and dividends are at records. But the discipline that’s underpinned the industry is slipping, leaving companies more and more dependent on commodity prices that are also starting to look shaky. For miners enjoying their recovery from the crash of 2015, the best years may already be in the rear-view mirror.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments