Aluminum trader’s huge LME position ignites battle for stock

One of the world’s biggest metals traders has built up a dominant position in one part of the London Metal Exchange aluminum market, creating a squeeze on exchange stocks and putting focus on the availability of non-Russian metal.

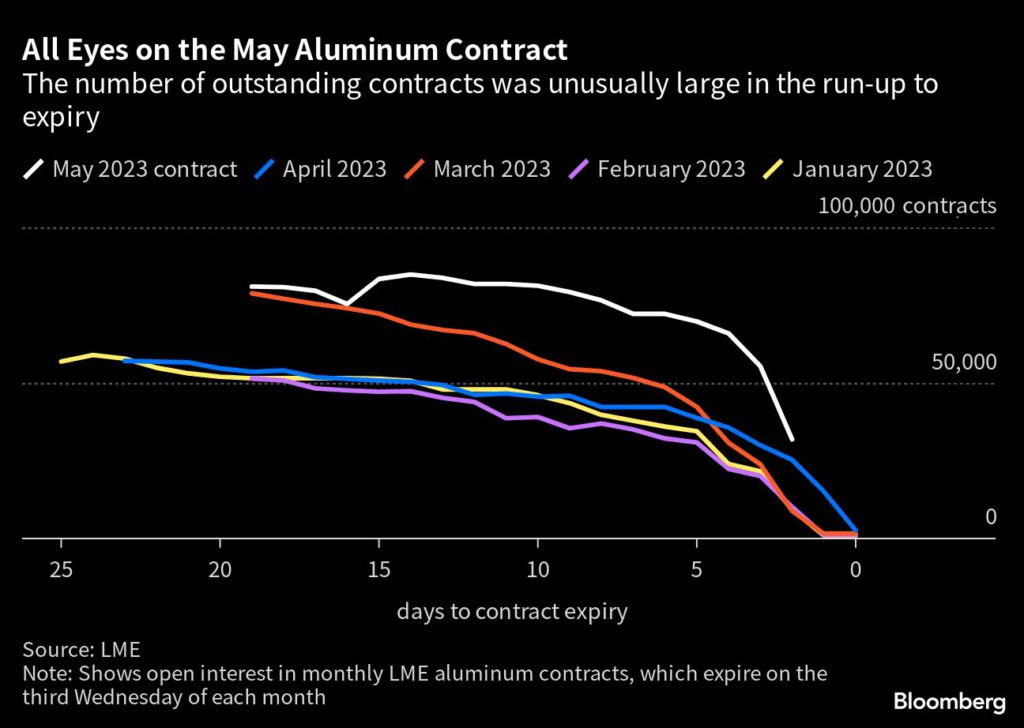

IXM, owned by China’s CMOC Group Ltd., has built up an unusually large position in the LME’s aluminum contract for delivery tomorrow, which as the third Wednesday of the month is a key focal point for liquidity, according to people familiar with the matter who asked not to be identified discussing private information.

The trade has thrown a spotlight on a battle for aluminum inventories among top traders including IXM and Trafigura Group that looks set to drain non-Russian metal from the LME and leave the exchange’s contract much more dependent on Russian aluminum. The position has become a hot topic among traders in the aluminum market, where the outlook is dominated by weak demand on the one hand and production problems on the other.

As of the end of last week, the IXM position was over 318,000 tons of aluminum, worth more than $700 million, according to exchange data which does not identify the trader behind it. That compares to a total of just over 370,000 tons available for delivery from LME warehouses.

For IXM, the position could allow it to pick up large volumes of aluminum from LME warehouses once the May contract expires, potentially strengthening its hand in the physical market if industrial demand starts to rebound. But a large withdrawal of Indian aluminum from the exchange last week means that IXM would likely be taking ownership of Russian metal that some consumers are trying to avoid.

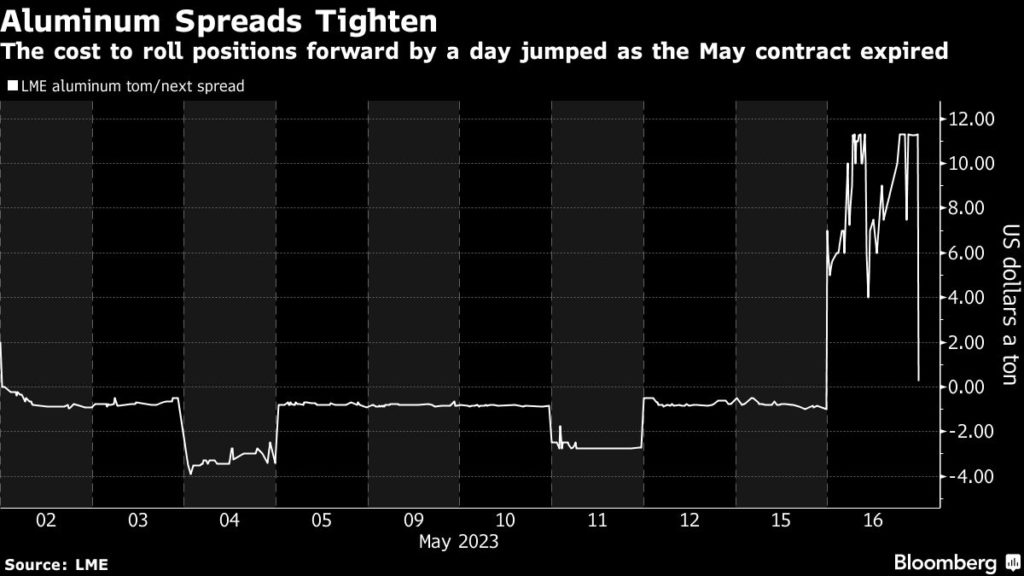

The existence of the large position resulted in contracts for delivery on Wednesday trading at a large premium over contracts for the following day — a condition known as backwardation that points to a tight market, and can put pressure on holders of short positions who need to buy their contracts back as they approach expiry.

The LME has measures to prevent market squeezes and corners, including a rule compelling traders with dominant positions to lend them at set rates. Traders with positions equivalent to between 50% and 80% of available inventories must lend at a rate of 0.5% of the price of the metal per day. For aluminum that rate is currently $11.30 a ton — the same level where the so-called “tom-next” premium peaked on Tuesday.

Representatives for IXM declined to comment. The LME is monitoring the market carefully, a spokesperson said.

“LME market surveillance team has been carefully monitoring the recent large long position in aluminum and engaging with the parties involved to ensure market orderliness and conduct are maintained,” the exchange said.

The squeeze is focused on aluminum for immediate delivery and hasn’t impacted the wider market, where benchmark prices for delivery in three months were trading at $2,254 a ton on Tuesday, near the lowest this year. Still, some traders believe that prices could rally as a drought in key Chinese producing region Yunnan threatens to curb supplies.

It’s not unusual for traders to take large positions on the exchange, and they can sometimes try to take delivery of large quantities of LME material in order to “sift” warehouse receipts for particular brands of metal held in convenient locations.

Regardless of IXM’s intentions, the trade has already had the effect of reducing the amount of non-Russian aluminum on the exchange.

Last week, more than 130,000 tons of aluminum was requested for delivery from the exchange, which was principally Indian metal that had originally been delivered in by trader Trafigura, according to people familiar with the matter.

Withdrawing it from the exchange ensured that IXM could not snap it up, while also meaning that the LME’s rules forcing IXM to lend out its position would kick in at a lower threshold.

“The cancellation caught the market off guard and everyone’s been talking about what a smart move it was,” said Alastair Munro, an analyst at Marex Group. He declined to comment on the identity of the party that had canceled the material or of the holder of the long position. “It meant that the long became subject to the LME’s lending guidance sooner rather than later, and from the trading activity we’ve seen, it does looks like that they’ve been letting some of their position go.”

The concentration of Russian metal is a fraught question for the LME, which last year faced calls from western producers and traders to ban deliveries of Russian metal but ultimately decided not to. As of the end of last month, Russian-origin metal made up just over half of the 492,000 tons of aluminum on the LME.

The LME spokesperson said that the exchange continued to monitor the market carefully, but that Russian metal was continuing to be consumed “which supports the conclusion reached in the discussion paper undertaken at the end of 2022.”

(By Jack Farchy, Mark Burton and Archie Hunter)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments