Alumina wake-up call for the aluminium supply chain

Alumina, which sits in the aluminium production process between bauxite and refined metal, has historically been a highly efficient link in the supply chain.

It hasn’t generated many headlines over the years because it has largely avoided any newsworthy disruption.

It is, to quote Greg Wittbecker, analyst at the CRU research house, one of those markets “people have taken for granted”.

Not any more

A series of supply hits have sent the alumina price on a rollercoaster ride this year, at one stage threatening the closure of several European aluminium smelters.

This volatility poses some hard questions for aluminium producers, not least as to how alumina is priced.

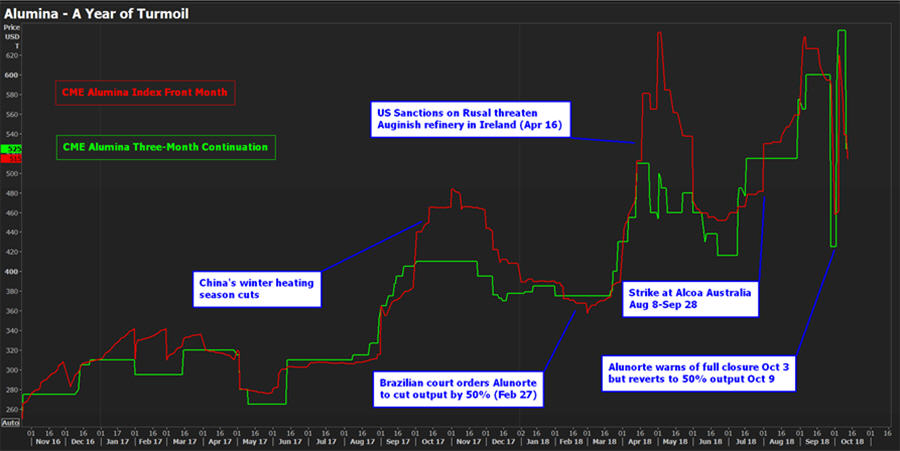

A year of living dangerously – part 1

Alumina’s year of turmoil began in February, when a Brazilian court ordered the part suspension of Hydro’s Alunorte refinery after heavy rains raised concerns about leakage from the plant’s tailings ponds.

Alunorte, with capacity of 6.3 million tonnes a year, is the world’s largest single alumina production site and has been operating at half capacity ever since.

Hydro threatened full closure of the plant on Oct. 3 as the existing tailings area reached capacity, but it reversed the decision on Oct. 8 after the authorities granted permission to use a new residues facility.

Alunorte has reverted to half-capacity operation, as have the bauxite mines that feed it and the Albras aluminium smelter that takes some of its product.

The CME alumina price has whipsawed on the latest Alunorte developments, surging from $425 a tonne to $620 on the full-closure news before retreating back to $515 on confirmation it would resume 50 percent production.

Alunorte, CRU’s Wittbecker told an LME Week seminar last Tuesday, has been “a reality check to pay more attention to alumina”.

A year of living dangerously – part 2

The market’s Alunorte woes were compounded in April, when the United States slapped sanctions on Oleg Deripaska and his Rusal aluminium empire.

That blew a hole in alumina’s complex supply chain, threatening the closure of Rusal’s Aughinish refinery, which in turn placed at risk the European smelters that rely on the Irish plant’s output.

The sanctions deadline has been extended again to Dec. 12 and the market’s assumption is that it is only a matter of time before they are lifted fully.

However, the fragility of the alumina supply chain has been brutally exposed, serving as wake-up call for the aluminium sector and the U.S. and European governments, who received a short, sharp lesson in the multiple interdependencies of this previously uncontroversial commodity.

A six-week walkout by workers at Alcoa’s Western Australia bauxite mines and alumina refineries simply added to the pricing turbulence before a peace deal was struck at the end of last month.

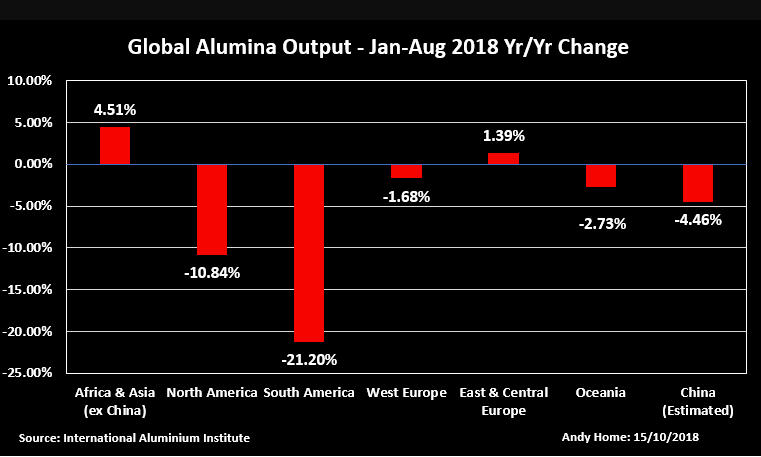

The combined effect of these supply scares has been a 5 percent year-on-year drop in global alumina output in the first eight months of this year, according to the International Aluminium Institute.

South American output has slumped by 21 percent because of the continuing loss of production at Alunorte.

CRU is forecasting the world outside of China to record a 400,000-tonne alumina supply deficit this year.

China constrained

China, the world’s largest producer of both alumina and aluminium, has helped to fill the supply gap in the rest of the world.

Historically a net importer of alumina, China has flipped to net exporter this year as overseas sales have been driven by the high international price.

But there is a practical limit on how much alumina China can divert to overseas markets.

CRU’s Wittbecker says alumina in China tends to be bagged, which means it has to be unpackaged before to shipment to the international market. Exports this year are unlikely to exceed 2 million tonnes, though even this is “unprecedented”.

Moreover, China, is also expected to be in the unusual position of facing a supply deficit this year, to the tune of 843,000 tonnes, CRU says.

The industrial curtailments during the winter heating season took a heavier toll of the country’s alumina producers than its aluminium smelters.

Environmental checks on the bauxite sector this year also caused some alumina operators to curtail production, while a slew of new projects have been cancelled in the face of local opposition.

China, in short, is unlikely to be able to continue rebalancing the global market for any sustained period.

Price volatility

At current alumina prices, a significant amount of global smelting capacity is losing money – about 40 percent of it, according to CRU.

The aluminium production sector is now paying the price for changing the way alumina is priced.

Historically, the alumina price was linked to that of primary aluminium metal on the London Metal Exchange (LME), the ratio rarely deviating much from the 17 percent level.

Earlier this decade, however, producers such as BHP Billiton and Alcoa engineered a switch of pricing to spot indices, arguing that the LME linkage undervalued alumina.

This, arguably, has simply added to this year’s price volatility because the spot market is still highly illiquid.

Some of the price spikes have been based on a very limited number of spot cargoes, meaning that a 130 million tonne global market has been upended by the pricing of a couple of hundred thousand tonnes.

The CME contract, based on S&P Global Platts’ assessment of the spot market, is still immature. Turnover this year has totalled 547,500 tonnes, up only marginally on last year’s levels.

The LME is planning to launch its own futures contract next year, while the Shanghai Futures Exchange (ShFE) is also studying a potential offering.

However, such contracts will also depend on assessments of what is currently a low-liquidity spot marketplace.

Evidently, the alumina futures market has a lot of growing up to do – and fast – if producers are going to be able to hedge what has become an exceedingly volatile market.

That volatility looks to be here to stay, even if both the Alunorte and Rusal disruptions are resolved.

No one will be taking alumina for granted any more.

(By Andy Home; Editing by David Goodman)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments