This is the scariest mining chart you’ll see today

For the last three years the mantra at mining companies has been cut costs and cut budgets.

Projects have been delayed, expansions have been shelved, exploration stalled and expenditures deferred.

Project investment at BHP Billiton this year will be a stunning $10 billion below its 2013 peak. The world’s number one miner only has four projects in the works, two of which are almost complete, compared to 18 mine and infrastructure developments just two years ago.

The situation is no different at other majors but belt-tightening extends from the top tier right through the industry.

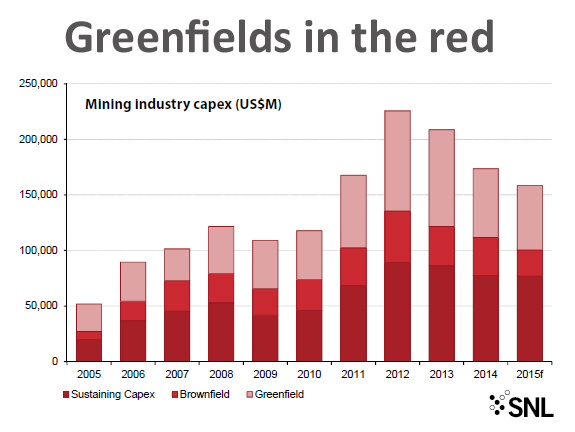

A new report by SNL Metals and Mining finds total capital spending across all mining companies has declined by around $70 billion since the 2012 peak to just over $150 billion forecast for this year.

Source: SNL Metals & Mining

Mark Fellows, director of consulting for the mining research firm, says while sustaining capital expenditure is down 13% since the peak in 2012, capital expenditure on new developments has been even harder hit.

Spending on brownfield expansions is down 25% while greenfield project expenditure has plummeted by nearly one third.

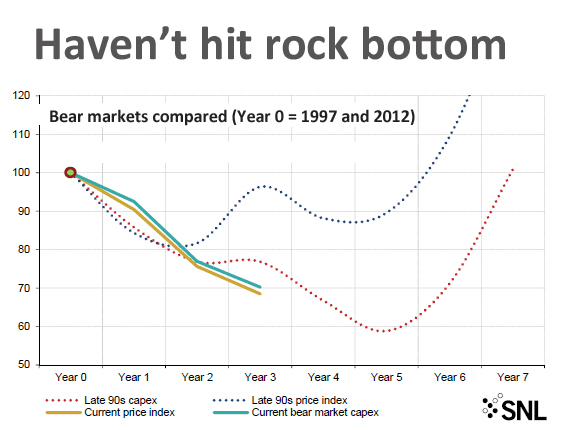

The report compares the current downturn to the previous bear market in mining which ran from 1997 to 2002 and argues that capex cutbacks are far from over.

Instead the industry should brace itself for at least another two years of shrinking budgets and outlays with the first signs of a “subdued” recovery only appearing early in 2018.

But even this prediction could be too bullish.

“Worryingly, metal prices have already fallen 12% further than they did during the bear market in the 1990s. In the last bear market, capex only recovered to its pre-crash (1997) level after seven years (2004),” according to Fellows.

Source: SNL Metals & Mining

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

10 Comments

Gene Byrge

You sir are totally and unequivocally full of beans. Bet all your money on the bears. We’ll wave when we go by.

Frank Delzer, P.E.

And this does not include the impact of inflation aka the US $ losing purchasing power!!!

Gene Byrge

The current contest is whether the market will be controlled by whimsical speculators or demand for the product. I would aver that historically, it ALWAYS ends up supply and demand controlling the cash register. So continue with your charts and predictions, leave the producers alone.

ExPat

There should be massive consolidation in the precious metals mining industry over the next 5 years.

Pedroble

Who are you trying to scare? That chart turns upward.

JD

The global crisis smashed most metals in August 2007. The mining sector has not recovered but this graph seems to start 3 years ago? (It has been 8 years and counting…)

EMILIO ZUNIGA

From scrash large mines take at least 7 years to maturity. Projects 4 years down the road can be pospone with no harm. Projects with EPC contracts go ahead. Pending China recovery ( it swalops half the demand of base metals) in 3 years stocks should level down. The accouting supports 2018 as the year one can expect the down cycle near the end.

Heng

China is cutting investment in housing industry and the house price has been refrained for years. the demand for building metals is down, there is no clear sign of such recovery in the country, maybe the next bull will come after India grows up.

Rayban

China built too much and must catch up . This , the banks are out , they do not trade nearly as much as during the bull . You say they find ways to trade as time goes onward . Sure , but not as many or as big . Without them to stabilize markets and flatten curves metals shall be much more volatile and less likely to please . Squeezes common and trouble aplenty . Repeating , the banks are largely out of commodities trading .

China is but 1 BRIC country , BRIC is F” ‘ d . Brazil is scre”‘d , India is stuck in YEAR 100 bc , Russia is off the Vodka Bottle and China is slow .

1 More itty bitty thing . In investing history never repeats itself . If you think it does I have a Gold Mine with significant Promotion you need to listen about .

jgv1 .

The weak will have to die, only the best cost producers are going to survive.