Metals production emissions must halve by 2040 – report

Emissions from metals production will need to halve over the next 20 years in order to achieve the Paris Agreement decarbonization goals, a new report by Wood Mackenzie finds.

To reach such a target, the market analyst proposes a rise to the price of carbon dioxide per tonne to $110 everywhere by 2030.

“These taxes aim to spark massive technological change across emissive industries like metals production,” the report reads. “Carbon taxes levied under a 2-degree pathway also provide a good guide as to the budget needed for decarbonisation.”

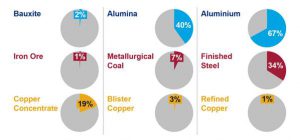

As a cautionary tale, the document presents the case of the steel sector, which has to eliminate 1.7 billion of direct and indirect emissions over the next 20 years. If the industry doesn’t comply, it would have to pay $191 billion per year in taxes, which is equivalent to 24% of annual global steel revenues of $800 billion in a good year.

The path to compliance, though, starts with progressive electrification, according to WoodMac.

“Mine designs need to adapt, and more renewable electricity is required. Whether from the grid or self-supplied, power supply arrangements will grow in prominence as miners become increasingly reliant on this single energy source,” James Whiteside, the firm’s global head of multi-commodity research, writes.

The electrification of thermal processes powered by renewables is also key to decarbonizing downstream sectors.

“Carbon is intrinsic to the dominant production routes for aluminium and steel. But sustainable and scalable alternatives are emerging. Aluminium smelters’ carbon anodes now have inert alternatives. Coking coal can be replaced with hydrogen for iron ore reduction.

Biomass and carbon capture can play a role in the right location,” Whiteside says. “Increased deployment brings down the cost of emerging technologies over time. Signatories to the Paris Agreement hoped their carbon policies would get the ball rolling, yet CCS and green hydrogen have been slow to truly kick-off. The learning curve in wind and solar costs will only be echoed in these technologies when their installation scales up.”

In the expert’s view, increasing investor pressures is also expected to accelerate change. “Miners are well equipped to access alternative sources of capital like green and ESG bonds through their role in low carbon technology. Development banks have ring-fenced funds to support energy efficiency and reduce emissions,” the analysis reads.

For WoodMac’s specialist, equity investors, currently most concerned with the impact of carbon pricing, are likely to be forced by their own stakeholders to examine the ambiguous aspects of sustainability reports. This means that junior miners seeking finance to develop their first operations will increasingly find detailed environmental planning a differentiator in capital raising.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments