The Polyus power play

With nearly nine out of every 10 of the world’s ounces as measured by production or reserves present, size mattered at the recent Denver Gold Forum.

Denver Gold Group, the organizers of the invitation-only event in Colorado Springs, brings together the global gold mining industry and the sector’s largest investors. The DGF has been held every year since 1989 and it’s worth remembering that gold was trading at $400 that year and was destined for a decade-long slump.

2016 Source: Company data, AMC CPR, Metals Focus

Despite the tumult in the industry in the intervening years the top tier of producers has stayed relatively stable. Thanks to a penchant for M&A the ranks of the world’s largest gold miners has only consolidated further in recent years.

Many gold producers are also beginning to talk about gold equivalent ounces to bulk up for the sake of investors. And after many quiet years mid-tier tie-ups are happening again and project acquisitions in exploration hot spots like the Yukon, Burkina Faso and Turkey are becoming more common.

The next few years will likely see the biggest shake-up at the top of the global gold pile in a decade.

In Russia with love

Polyus last month launched hot commissioning of its 10mtpa Natalka processing mill in Russia’s Far East. Once fully ramped up, Natalka is set to turn the country into the world’s number two gold producer behind China.

At full tilt the $2.3 billion Natalka mine will help lift Polyus production by a third to 2.8m ounces per year by 2019 and improve its ranking to around number five from the current 8th.

But the Moscow-based miner is not stopping there.

MINING.com sat down with Polyus chief executive Pavel Grachev at the DGF to find out what’s next for the company.

Polyus is not interested in embarking on an overseas spending spree and is not hung up about geographic diversity

Grachev is a lawyer by training and served three years as CEO of potash giant Uralkali before taking over the reins at Polyus in 2013. Grachev is unapologetic about the firm’s ambitions: “Polyus will be number three globally.”

As Russia’s number one producer Polyus is not interested in embarking on an overseas spending spree and is not hung up about geographic diversity says Grachev.

Grachev believes Polyus’s growth can be achieved organically and in its own backyard.

Olimpiada produced 943koz last year. Image: Polyus

Of course, a “very busy pipeline” and the industry’s second largest reserve base (71moz vs Barrick’s 77moz) makes that a much easier strategy to follow.

And an average mine life of 37 years – which Polyus claims is more than twice those of its peers – means the company’s half-a-dozen brownfield projects in the feasibility stage and seven brownfields either completed or in the final stages will only add to annual ounces, not make up for losses elsewhere.

Polyus was spun out of Russia’s top miner Norilsk Nickel in 2006.

Since then production has grown at annual rate of 6% to just shy of 2m ounces in 2016. That’s despite the fact that halfway through this period the company offloaded all its mines in Kazakhstan, Kyrgyzstan and Romania it acquired through its acquisition of Kazakhgold. During the first nine months of this year Polyus upped production another 13%.

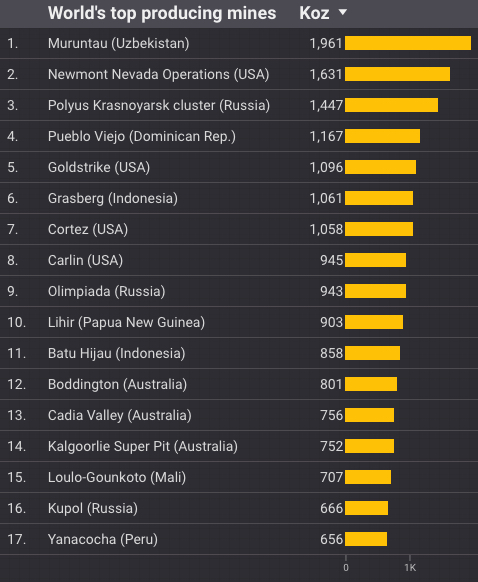

Those growth rates were achieved by expanding its flagship Olimpiada mine which still accounts for a half of output and three mines exploiting the Blagodatnoye, Kuranakh and Verninskoye deposits. And as something of a throwback to the early days of the industry, Polyus alluvial operations still contribute 9% of total ounces.

Dry gully flowing with ounces

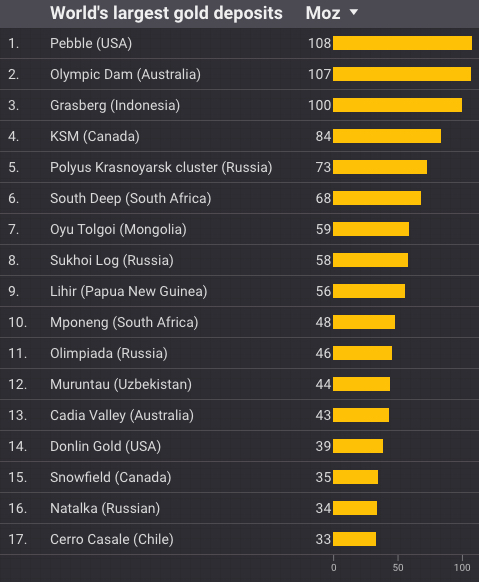

Sukhoi Log’s green fields hide 58m ounces of gold. Image: Gennady Vursiy Polyus

But the real game changer was in February this year when Polyus won a government-backed auction to develop the legendary Sukhoi Log deposit, one of the largest undeveloped gold deposits globally and the biggest gold greenfield project in Russia.

Located in the Irkutsk region of Eastern Siberia, Sukhoi Log (which translates to “dry gully” in English) was discovered in 1961 and extensively explored by Soviet geologists since the 70s. In total over 320,000m of drilling have been carried out, including by a team from Canada’s Placer Dome (now Barrick) in the late 1990s.

That would place Sukhoi Log near Muruntau in Uzbekistan, long the world’s most productive gold mine

A 2008 scoping study for Sukhoi Log estimated 930.3m tonnes of ore reserves, grading 2.1 g/t gold for 62.8m ounces of contained gold under the Russian Resource Estimation Standard or GKZ. Using JORC methodology Polyus calculated 887m tonnes of mineral resources at 2g/t for 58m ounces of contained metal in December 2016. Including Sukhoi Log, Polyus gold resources swell to a peerless 193m ounces.

Grachev says work on a $20-25 million per year feasibility study at Sukhoi Log would take another three to four years. SRK and Hatch have been contracted and the project is only 6km from the Verninskoye mine. Sukhoi Log is a well-known entity with nine engineering studies completed to date.

2016 Source: Company data, AMC CPR, Metals Focus

Camp construction has begun and drills are already turning on a 150,000m program, but Grachev sees no reason to fast-track development. The size of the operation is dependent on work done over the next few years, but there is no doubt that Sukhoi Log will be a massive mine.

According to Polyus’s London share offer prospectus Sukhoi Log would cost between $2 – $2.5 billion to construct and could produce roughly 1.6–1.7m ounces per year. That would place Sukhoi Log near Muruntau in Uzbekistan, long the world’s most productive gold mine.

Sukhoi Log would catapult Polyus into the top three of global producers and within shouting distance of the number one spot all things being equal. Which in gold mining they never are.

Free float

After an 18-month hiatus Polyus has successfully returned to the London Stock Exchange. The London investment community was less than thrilled when Polyus (and other Russian players) left for Moscow after fewer than five years, but Grachev says the company has spent a lot of “time and effort to build trust with the market” since then.

Prior to the London move, majority owner Said Kerimov agreed to sell a 9.4% stake to Chinese conglomerate Fosun International valuing the company at around $9 billion. If the Chinese government gives a green light to the deal, Fosun will buy a 9.4% stake and may exercise an option for another 5% at a (growing) discount to today’s ruling price.

In April last year the company introduced a new corporate governance structure and appointed three independent directors; most recently Maria Gordon, who previously ran a $10 billion emerging market fund for Goldman Sachs, was added to this list.

So why were investors willing to forgive and forget?

Following a successful $800m Eurobond placement, in June Polyus raised $879m in London selling 9% of the company, at roughly the same valuation as the Fosun deal and near the upper end of estimates. Its Global Depositary Receipts are up 20% since listing. Grachev says a top priority is to do more to increase the stock’s free float from the current 16% with a target of between 25%–30%.

So why were investors willing to forgive and forget?

Everyone loves a growth story and Polyus’s peers have been scaling back their ambitions since the boom years. Expected annual dividends of $500m+ don’t hurt either.

The limited impact on the ground for Russian miners of Western sanctions may have also convinced investors to get back in. Grachev says the only way Polyus has been affected are curbs on Russian banks which increased the cost of capital, but it’s not a significant hurdle staying below 5%.

All in

Free flowing ounces. Image: Polyus

But in the end, it all boils down to one thing. Margins. Big fat ones.

Total cash costs for Polyus averaged $389 an ounce in 2016 and on all-in basis it was $572. That, not surprisingly, puts the company in the first decile of the global cost curve.

Don’t make the mistake of pinning the company’s low cost on the rouble says Grachev. In fact, the Russian currency had its best year ever in 2016 and has appreciated further this year.

All but one of Polyus’s mines are fly-in fly-out; all are large-scale open pit operations (and with grades associated more with underground mines), connected to grid power and grouped in clusters making reliance on third party infrastructure minimal.

It’s not just the underlying quality of the assets says Grachev: the company has a comprehensive cost reduction program across all units working on everything from recovery rates to information technology.

Moreover, Sukhoi Log would only improve cost measures for the company. Polyus expects costs of $430–$500 an ounce. Yes, that’s all in.

Grachev would not be drawn to predict the gold price. At those margins, he doesn’t have to.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Restless Boomers

Russia and China believe in ‘The Golden Rule’. Good article!