Platinum and palladium markets to go into deficit in 2016: GFMS

There is good news on the horizon for investors of platinum group metals (PGMs), though a reader has to scrutinize the fine print in the latest report from GFMS to find it.

The GFMS team at Thompson Reuters released their annual GFMS Platinum Group Survey 2016 (registration required) last week. In it, GFMS forecasts the platinum market will return to a small deficit in 2016 and the deficit in palladium will deepen, with the chief determinant of lowered supply for platinum being a reduction in mined metal.

“There will be little addition from new projects in the development pipeline while the headwinds of mines’ reduced capital spending is expected to start to weigh,” say the report’s authors.

But while the supply-demand fundamentals look positive for platinum and palladium, GFMS says it is broader macroeconomic criteria that will be the primary price drivers of PGMs this year.

“The GFMS forecast sees broad support from extremely gradual U.S. monetary tightening, paving the way for higher prices in 2016, particularly for palladium.”

Dissecting how the markets for palladium, platinum and rhodium changed between 2014 and 2015, GFMS says the prices of all three metals fell “on the back of a year unimpeded by industrial action in South Africa and amid a bad year for commodity returns generally.” Readers will recall the 5-month strikes at platinum mines in South Africa in 2014. The end of those strikes pushed combined production of platinum, palladium and rhodium by 37%, the highest since 2011.

“The GFMS forecast sees broad support from extremely gradual U.S. monetary tightening, paving the way for higher prices in 2016, particularly for palladium.”

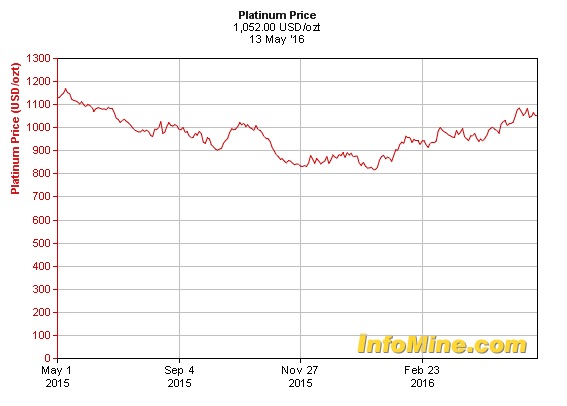

The price reductions were also exacerbated by: liquidations of ETF positions, with platinum investors reducing their positions by 0.26 million ounces; the Volkswagen scandal, which pushed expected demand for diesel vehicles lower- platinum is a primary ingredient in auto catalysts; and the lower South African rand, which depreciated 26 percent between 2014 and 2015.

2015 platinum: marginal surplus

A rebound in mine production pushed the platinum market back into a marginal surplus. According to GFMS, global output recovered 27% to 6.16 million ounces, while in South Africa, production was up 40%. The weak rand and and a 23% reduction in costs also augmented the production figures. The net balance for palladium, adjusting for movements of palladium in ETFs, shows a slightly smaller surplus of 265,000 ounces in 2015 compared to 375,000 ounces in 2014.

Scrap jewelry supply was robust, climbing 4% in 2015 to 0.54 million ounces, the highest level since 2011, driven mostly by a 21% surge in Chinese scrap supply. In contrast, in North America and Japan low platinum prices saw recycling volumes slip to near-decade lows.

Autocatalyst scrap declined by 14% in 2015, giving up gains of the last two years to reach 0.93 million ounces says GFMS, particulary North American and Europe, “as lower steel and PGM prices impeded the flow of scrap down the supply chain.”

On the demand side, platinum consumption in autocatalysts rose by 2% last year to 3.0 million ounces, with the offroad sector being the primary demand driver at a 24% increase. However platinum used for making jewelry dropped by 4% to 2.46 million ounces, mostly due to lower consumer spending capabilities in China. Industrial segments were also weaker, with the chemicals sector down 17%, the petroleum industry retreating 18%, and platinum demanded by electronics also dropping.

2015 palladium: deficit shrinks

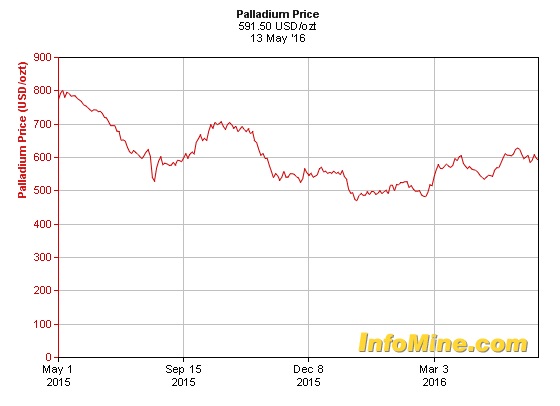

A 9% increase in mine production shrunk the palladium deficit considerably in 2015. The end of strikes in South Africa pushed production in that country up 32% to the world’s highest-level producer, while Canadian palladium output dropped 10% and Russia’s remained steady. The net balance shrank from a 1.571 million ounce deficit in 2014 to just 290,000 ounces last year.

The biggest contributor to supply was autocatalyst scrap which, while off by 11%, was still 1.6 million ounces, the second highest level recorded. Palladium jewelry scrap was also up, by 7% to 0.27 million ounces, a new high. The growth was exclusively driven by China, with low metal prices crushing recycling volumes in other markets, according to GFMS.

Demand-wise, palladium used in autocatalysts was up 4% to 6.89 million ounces. In contrast, demand for industrial applications was weaker all-round, falling to a 10-year low of 2.17 million ounces. Jewelry demand slipped for the seventh consecutive year, to 0.35 million ounces. “China was the chief culprit,” says GFMS, with demand there plummeting 70% after several fabricators left the industry.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments