Osisko’s hybrid model could be the future of gold streaming

Sean Roosen, Chairman and CEO of Osisko Gold Royalties

Precious metal streaming and royalty companies are the envy of the industry.

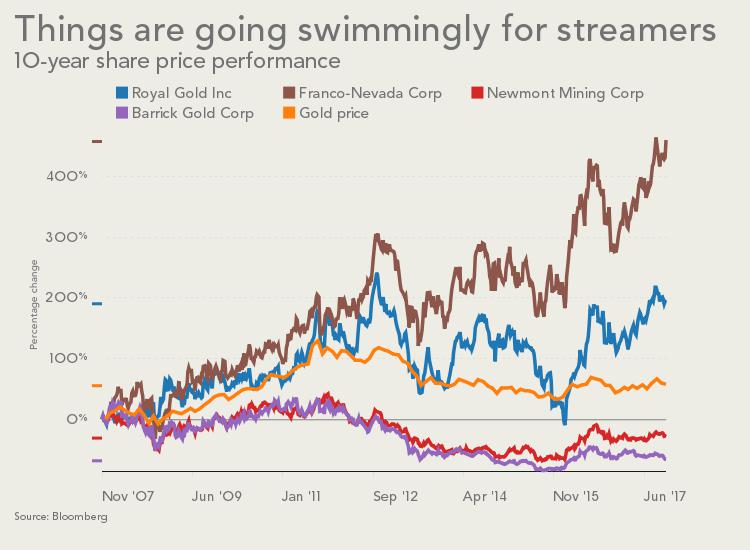

The relative share price performance over a 10-year period of the largest gold streaming and royalty companies vs the top gold miners is eye-popping (and for those who picked the wrong crowd a decade ago probably eye-watering).

As if to prove that streaming is still where gold mining’s action is the sector saw a $1 billion deal close only three months ago

Investors love streamers for their (more) predictable cash flows, minimal GSA overheads, revenues per employee more associated with companies making iPhone apps and low risk profiles. Miners are attracted to streaming deals because it’s not dilutive like equity transactions and easy on balance sheets.

Clearly the kinds of returns shown on the graph will attract competitors and the field has become much more crowded – from micro and small caps like Metalla and Maverix to companies like Sandstorm bent on a billion dollar evaluation. Even the likes of Glencore is toying with the idea of spinning off a streaming company.

Centerra’s cash purchase of Aurico Metals at a healthy premium just this week shows a sprinkling of royalties may be the sugar on top juniors need to attract big players.

Franco Nevada’s 2007 debut still ranks as North America’s largest mining IPO ever. Royalty companies have also been involved in some of the biggest mining transaction of the past decade.

Franco Nevada set the bar high back in 2012 with its $1 billion deal with Inmet (now First Quantum) in Panama and Silver Wheaton (now Wheaton Precious Metals) followed up its $1.9 billion deal with Vale in 2013 with an $800m agreement with the Brazilian giant three years later.

For precious metals streamers the sweet spot is gold or silver byproduct from a base metal mine with a life counted in decades, but deals like that are few and far between.

That’s especially true with better times returning to mining and the majors’ deleveraging of the past few years mostly done. Bellwether Franco Nevada seemed to indicate that the era of mega deals with debt-laden majors for their byproducts may be over. The company is now singing the praises of oil & gas and has to look upstream for opportunity.

But as if to prove that streaming and royalties are still where the real gold mining action is the sector saw another $1 billion deal close only three months ago.

Osisko Gold Royalties was formed in 2014 with the sale of its Canadian Malartic mine – the country’s largest gold mine. In August the Montreal-based company closed a $1.125 billion deal for 74 streams, royalties and off-takes from private equity firm Orion Mine Finance. The transaction catapulted Osisko Gold Royalties into streaming’s top tier.

The companies that we incubated are worth three times what we were worth three years ago

MINING.com sat down with Sean Roosen, Chairman and CEO of Osisko Gold Royalties to find out what’s next for the company and for the precious metals streaming business as a whole.

“2015 and the first half of 2016 was great for us to put down some bets – the streaming model is pretty good in a downward or flat cycle. An uptick market tends to be more equity driven,” says Roosen.

A 5% stream from Malartic (30koz per year for nothing) remains its anchor asset and it also picked up a diamond stream from the new Renard mine in Canada. The Orion deal ups production to 100,000 gold equivalent ounces next year.

Zero cost revenues should hit $100m this year and grow to $200m within five years says Roosen. From five assets three years ago the company today owns 130. It’s market value has gone from just less than $500m in 2014 to over $2 billion.

Osisko is unique in the sector with about a quarter of its investments going into a accelerator business it set up mid-2015.

“We’ve had good acceptance of our accelerator model. We match up management teams and assets under the Osisko umbrella, creating new companies like Osisko Mining, Barkerville Gold and Falco Resources.

“These companies did not exist in any significant value form three years ago and now collectively they are worth $1.5 billion – the companies that we incubated are worth three times what we were worth three years ago.”

Roosen remains bullish that these sort of growth rates can be maintained given its hybrid model.

“It’s a sustainable growth plan in terms of us being able to get in and provide both technical and financial wherewithal to put assets to work.

“Currently across our companies right now, there are 41 rigs turning and Osisko Royalties shareholders – without any more dollars in – will benefit from almost a million meters of drilling next year. “

Far from pulling back, Roosen says the company has hit the “accelerator pedal right now because we’ve got more drilling and more chances for exploration success on our platform than we’ve ever had.”

“Our core belief is all wealth is created through the drill bit.”

“Our core belief is all wealth is created through the drill bit. If you’re not drilling and you’re not discovering then it’s pretty hard to see anything new happening. We have the Osisko internal program which is called “SUDS” which stands for Shut Up and Drill, Stupid.”

Canadian Malartic gold mine, a partnership between Yamana Gold and Agnico Eagle is Canada’s largest.

Osisko believes plenty of opportunity still exists in the space. “In terms of our size deals from zero to $200m or $200m – $500m still present tremendous opportunity for us. Growing 5X over the next three years? Granted, not that likely.”

Roosen says that Osisko’s “reality is that we have pretty good organic growth in our existing platform so we don’t have to take a lot of risks, there’s no onus on us to take risks because we’re going to double our cash flow in five years without having to add another dollar into investments. For us to make an investment, it has to be a good deal.”

Roosen says the sector is returning to a more traditional streaming and royalty market targeting development and exploration assets.

“Most balance sheets got cleaned up last year. I don’t anticipate big debt-conversion deals on operating assets now.

“Typically, you’re going want to enter as close to the production cycle as you can. And get the cash-flow sooner rather than later.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Jeremie Grondin

BGM.V a stock to watch in the near future