Most copper producers in Chile barely breaking even — mining group

Chile’s Escondida, the world’s largest copper-producing mine. (Image courtesy of BHP Billiton)

More than 18,600 km from Beijing, in copper-rich northern Chile, beleaguered miners are barely coping with the impact of China’s economic slowdown.

The situation is worse than many think, according to the country’s mining industry group Consejo Regional Minero de Coquimbo (Corminco), which represents some of Chile’s top miners in the copper sector, including Antofagasta (LON:ANTO), Glencore (LON:GLEN) and Teck Resources (TSE:TCK.A, TCK.B) (NYSE:TCK).

Its president, Juan Carlos Sáez, told El Día newspaper (in Spanish) that a “majority” of the group’s members are already unable to make a profit.

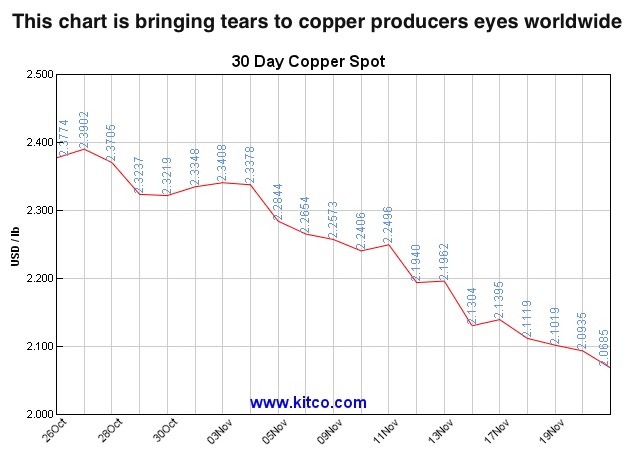

“We hope this is already the lowest level,” said Sáez referring to current copper prices. “Because it’s below the limit of exploitation for the majority of miners in the country.”

China’s voracious hunger for Latin America’s raw materials fuelled the region’s most prosperous decade since the 1970s. It filled government coffers and helped halve the region’s poverty rate.

That era is over, especially for Chile, the world’s top copper producer. Not surprisingly, the country relies heavily on the red metal, which makes up about half of its exports. To make things worse, roughly 40% of those shipments are destined to China, where demand has cooled dramatically, sending prices down to six-year lows.

That has cut into the profits of mining companies to the point that main producers, such as Chile-owned Codelco, have announced massive lay-offs to weather the copper price slump. Early this month, the world’s No.1 copper miner said it would axe close to 3,900 positions, including contractors, which would bring the number of layoffs by the company to over 4,000 only since September.

Codelco is not the only copper player taking drastic measures. In August, Freeport-McMoRan (NYSE:FCX), the world’s largest publicly traded copper miner, said it would slash its mining employees and contractors by 10%. It also said it would suspend operations at a mine named Miami in Arizona and decrease output at both its Tyrone mine in New Mexico and its majority-owned El Abra mine in Chile.

Chart courtesy of Kitco Metals.

Juan Carlos Sáez, President of the northern Chile-focused mining group Corminco. (Image courtesy of Corminco)

Chile’s government announced in September it would grant “emergency loans” to copper producers affected by current market conditions.

The loans will be given to medium-sized companies across the country — those with output of less than 50,000 tonnes of copper per year. In total, the rescue package is supposed to apply to about 20 companies, granting them the equivalent of about 10 cents per pound of copper produced, Platts reported.

But with only five weeks until the end of the year, when the subsidies are scheduled to stop, and metal prices down the slippery slope, the situation is as gloomy as it is uncertain.

“Without those subsidies, our members risk having to halt all operations,” said Sáez, adding that, for the copper sector, the only way to keep afloat is by having access to loans. “The government needs to keep supporting its mining industry, and that includes extending the loans program through 2016,” he told the newspaper.

On Monday, copper dropped to a new six-year low of $4,443.5 a tonne on the London Metal Exchange. December delivery, the most actively traded contract, closed down 1.9% at $2.0215 a pound on the Comex division of the New York Mercantile Exchange, the lowest level since May 2009.

And while prices recovered slightly on Tuesday, the metal has lost more than 28% its value this year and is down almost 57% since their 2011 highs.

More News

Endeavour Mining reports fatality at Burkina Faso mine

Mining and processing activities at the Mana mine site remain uninterrupted, the company said.

March 09, 2026 | 10:25 am

Argentina says Taca-Taca copper project represents $5.25B investment

March 09, 2026 | 09:42 am

LME to consider replacing warehouse rent caps with fixed daily load-out rates

March 09, 2026 | 09:36 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

nick kelly

So if DR. Copper knows what he’s talking about, the next crash is well under way