Iron ore price: Seaborne trade is Opec on crack

When the pace of China’s urbanization gathered momentum around a dozen years ago, iron ore was still considered a relic of the industrial age.

The seaborne trade was controlled by the Big 3 producers – Brazil’s Vale and Australian giant Rio Tinto and BHP Billiton. The miners negotiated the annual benchmark price during secretive talks with primarily Japanese steelmakers. Annual contracts were signed and the rest of the industry fell in line.

Much has changed since then.

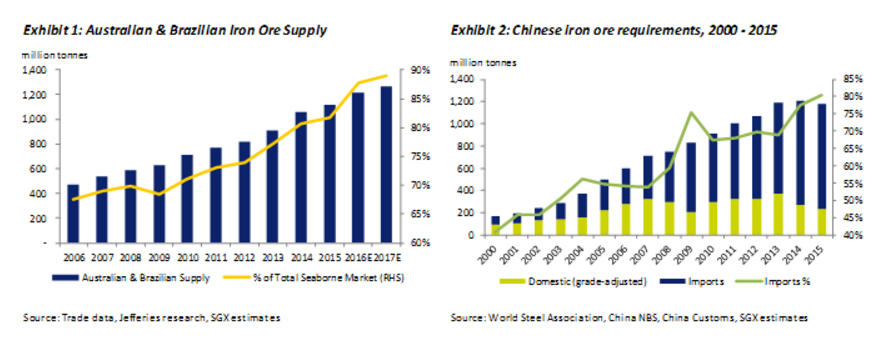

Brazil and Australia have captured more than 80% of the seaborne market. Opec controls around 40% of world oil production and Saudi Arabia represent less than a third of the cartel’s total output

Chinese imports now constitute three-quarters of all cargoes which has ballooned to 1.3 billion tonnes per year making it the second most traded bulk commodity on the planet after crude. Price-setting has moved from annual benchmarks to quarterly contracts to spot pricing and increasingly to derivative markets.

But much has stayed the same.

The Singapore Exchange – the first to launch iron ore price derivatives in April 2009 – in a new research note point to rising supply risks as Brazil and Australia come to completely dominate the seaborne market.

With another Australian miner, Fortescue, joining BHP and Rio at the big table and Vale continuing to aggressively expand in its home base, supply from these countries have been on a relentless upward curve.

Australia upped its exports to China 10.8% last year while Brazilian cargoes increased just over 12%.

Between them these two countries could approach 90% of the seaborne market as soon as next year. For a quick comparison consider that Opec controls around 40% of world oil production and its main member Saudi Arabia represent less than a third of the cartel’s total output.

At the same time Chinese steelmakers have become increasingly reliant on imports as domestic miners struggling with high costs and low grades are pushed out of the market.

Chinese imports hit a record 952.8 million tonnes in 2015 and the country is now reliant on imports for 80% of its needs according to this SGE chart.

Last week the suspension of activities at Vale’s Port of Tubarão – responsible for roughly 8% of global shipments – led to a rally in iron ore prices, which have consequently come down again.

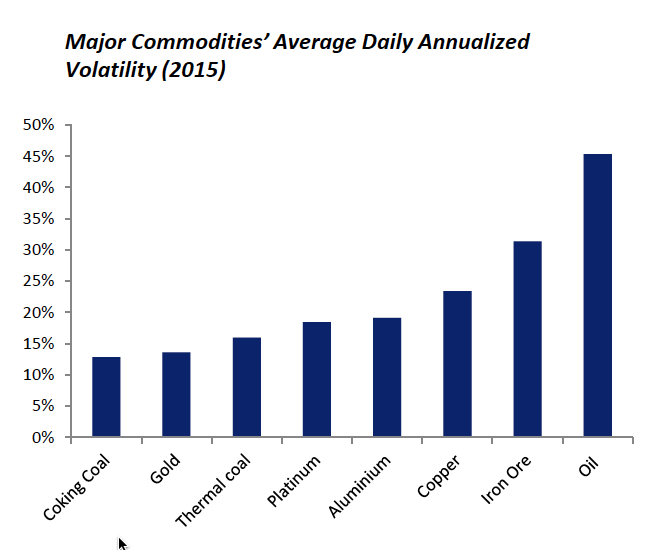

SGE warns strong and relatively undisrupted supply growth from the majors has masked increasing supply-side concentration risk in iron ore:

“As a result, supply disruptions moving forward may hold a greater bearing on supply-demand fundamentals, potentially leading to greater pricing volatility.”

As if it’s not volatile already:

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments