Iron ore price plummets amid Chinese speculative mania

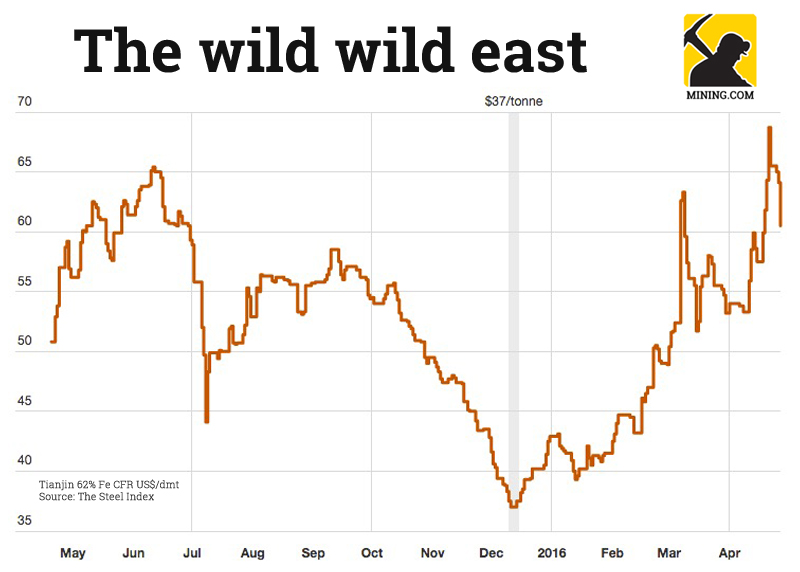

On Wednesday the Northern China benchmark iron ore price fell 5.6% to $60.50 per dry metric tonne (62% Fe CFR Tianjin port). Iron ore is now down more than 12% from 16-month highs hit last week according to data supplied by The Steel Index, but the steelmaking raw material still boasts a 41% rise in 2016 and a 60%-plus recovery from nine-year lows reached mid-December.

Given that it forges half the world’s steel and consumes more than 70% of the 1.3 billion tonne seaborne trade, the iron ore market is reliant, more than any other commodity, on the Chinese economy.

After authorities introduced trading curbs on stocks in 2015, many Chinese investors shifted their attention from the country’s equity markets to commodity derivatives

The surge in iron ore over the past four months has come mainly on the back rapidly rising steel prices in China and commodity investment fever that’s gripping the mainland.

Copper fell victim to Chinese speculators a year ago when a hedge fund called Shanghai Chaos conducted a bear raid on copper futures. Attention has now shifted to iron ore and other metals including aluminum.

The first signs that the fundamentals of the physical iron ore trade was no longer much of a factor driving prices came on March 7. The price surged 19.5% in a single day – in absolute terms the day-on-day rise was roughly half of the price of contracted iron ore during the early 2000’s under the old ‘annual benchmark’ system, which ended in April 2010.

Since then volatility has only increased – nearly 240 million tonnes worth of Shanghai rebar futures contracted changed hands on a single day last week. Reuters points to the fact that it “was equivalent to around a third of China’s steel production last year, not just of construction-destined rebar but of every imaginable type of steel product.”

Circuit breakers on the Dalian Commodities Exchange to curb excessive price movement have been repeatedly triggered the past few weeks. After a very subdued launch in October 2013, volumes have sky-rocketed and last month daily trade in iron ore contracts surpassed one billion tonnes for the first time. That figure compares to the annual global seaborne trade of around 1.3 billion tonnes.

Stock and commodity exchanges are lightly regulated in China and of course not a lot of institutional history. The feeding frenzy have prompted Beijing to intervene in commodity markets in a replay of last year, when ill-fated attempts to stop a free-fall on equity markets trade in the majority of stocks were halted.

Chinese authorities’ record on market intervention is not good and speculative bubbles tend to blow up spectacularly inside the country

A defining feature of the Shanghai and Shenzhen stock markets is the high percentage of retail investors. A whopping 80% of investors buy and sell stocks using their own accounts. On US stock markets that figure is less than 14%. After authorities introduced trading curbs on stocks in 2015, many of these investors shifted their attention from the country’s equity markets to commodity derivatives.

While the plunge on the Shanghai and Shenzen stock exchange had limited effect elsewhere in the world, six out of the world’s ten most active commodity contracts are now traded in Shanghai, Dalian and Zhengzhou.

And as last year’s stock market fiasco showed, Chinese authorities’ record on market intervention is not good and speculative bubbles tend to blow up spectacularly inside the country.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments