Idaho’s Silver Valley Poised for Expansion

Idaho’s Silver Valley, better known to miners as the Coeur d’Alene Mining District, has an exciting 110 year history of lead, zinc, silver and copper production, much of which has taken place through shafts several thousand feet deep. Over the years, lead and zinc have carried the load at times, but it is silver that causes the most excitement and brings new money and miners to the valley today.

Since 1884, the Silver Valley has produced 1.2 billion troy ounces of silver, 8.3 million tons of lead, 3.3 million tons of zinc, 207 thousand tons of copper and 529,000 troy ounces of gold (worth US$37 billion at today’s prices). Most of these metals were produced from steeply dipping narrow veins, some of which extend from surface outcroppings to a mile or more deep.

The veins are mostly associated with, but not within, a major structural feature called the Osburn fault, which extends the length of the valley. Each deposit has its unique characteristics, but the ore minerals generally comprise some combination of tetrahedrite, galena, sphalerite and chalcopyrite, along with siderite and quartz gangue minerals. The wallrocks are mostly quartzite and argillite of the Precambrian Revett and St. Regis formations. Narrow vein mining at these depths is difficult, costly and dangerous.

As depths increase, the costs for moving workers, supplies and air to the stopes increases, as does the cost of hoisting ore to the surface. Rock and water temperatures sometimes exceed 110 degrees F, and rockbursts are an everpresent threat. A challenging and intriguing part of all this is that exploration is difficult and costly as well. Most of the exploration takes place from existing workings at great depth, mostly by tunneling and drilling into untested ground.

For this reason, large volumes of the earth’s crust within the district remain untested. As Paul Dirksen, Timberline Resources Chairman, describes it, “There are many good opportunities left in the Coeur d’Alenes, but few for the little guy. Targets are mostly deep and require extremely large expenditures of risk capital to access and explore.”

In 2010, prices for metals mined in the district approached historic highs; consequently, the district’s producing mines operate at capacity today and conduct exploration programs to provide for expansion. New money flows into the district to reopen existing mines and explore for additional resources. Following are descriptions of the major projects active in 2011.

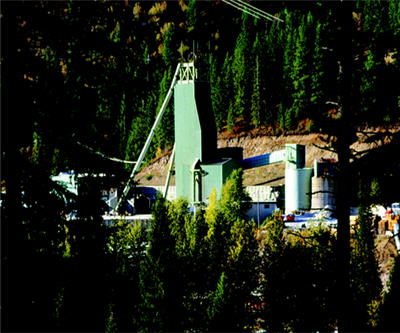

Lucky Friday Mine

Hecla Mining Company’s Lucky Friday mine, near the east end of the district, has been a model and an inspiration for Silver Valley explorers and developers since it began producing silver, lead and zinc 60 years ago.

The original Lucky Friday vein was mined until 2001, when production shifted to the Lucky Friday Expansion Area, accessed by tunnels driven about a mile to the northeast. The Expansion Area turns out to be a system of veins considered to be the downward extension of the old Gold Hunter veins which were mined to a depth of 1,800 feet a century ago.

The principle mining method at the Lucky Friday is mechanized cut-and-fill. Ore is hauled by truck to the Number 2 shaft where it is hoisted to the surface for milling. Concentrates are shipped to the Teck smelter in Trail, B.C., Canada. An active exploration program focuses on underground drilling to intercept the Expansion Area vein system above, below and to the east of the presently-defined reserves. Hecla reports multiple encouraging vein intercepts in these areas as high as 85 oz/t silver and 32.7% combined lead and zinc over a width of 3.1 feet.

Hecla is sufficiently confident in these resources to propose an internal Number 4 shaft to access them. The proposed shaft will descend from the 4900 level to the 7800 level, and possibly to the 8800 level. The shaft is expected to cost $150 to $200 million and could increase the mine’s annual silver production by 50 percent and extend the mine life beyond 2030. Hecla is also expanding its search to the Noonday vein, 1.5 miles to the northwest. Ores — up-dip from stopes last mined by the Star Mine in the 1980s — would be trucked on the surface from an adit at the Star 700 level to the Lucky Friday mill.

The Snowstorm Project

Immediately east of the Lucky Friday mine, Timberline Resources Corporation recently completed a drilling program to explore silver and copper mineralization in a halo zone surrounding the old Snowstorm mine workings. The halo zone was previously explored by Hecla, which estimated that it contains 5 to 10 million tons of material grading 1% copper and 1 oz/t silver.

The Snowstorm deposit is significant in that its mineralization, unlike that of most of the other deposits in the district, occurs as disseminations of copper and silver in Revett Formation quartzite, similar to the Troy, Rock Creek, and Montanore deposits, 55 miles to the north. Timberline drilled 10 holes along a 3.5-mile mineralized horizon in the Revett and found good grade mineralization in every hole, but thicknesses were disappointing.Timberline is presently focusing on other projects, but Chairman Paul Dircksen says, “We still like the Snowstorm. There are a number of good targets yet to be explored.”

Galena Mine

The Galena Mine is the central anchor for a string of three developed projects, the Caladay Mine, the Galena Mine and the Coeur Mine, all connected by underground tunnels stretching three miles beneath the mountains above the towns of Wallace and Osborne. All three projects are owned by U.S. Silver Corporation, which acquired them in 2006 for US $15 million.

At present, the Galena Mine is the only producer among the three, but the fortuitous interconnection of the properties provides U.S. Silver with considerable operational advantage. The Caladay facilities provide ventilation, possible hoisting capacity and an escape route for the Galena. The inactive Coeur mill processed Galena ores in the past and could do so again.Since 1953 the Galena has produced 160 million ounces of silver, 116 million pounds of copper and 22 million pounds of lead from 7 million tons of ore.

Last year, the Galena mine produced 2,427,156 ounces of silver, 6,446,856 pounds of lead and 1,075,307 pounds of copper. Cash cost per ounce of silver was $11.72.U.S. Silver maintains an active exploration program at depth. Recent work has identified three new veins and a downdip extension of the 306 vein, all between the 4000 and 5200 levels of the Galena mine. At the time of this writing, drifting on the 306 vein at the 5200 level had exposed 68 feet of strike length with an average grade of 21.55 oz/t silver and 0.83% copper, over an average width of 4.1 feet.

Three new veins have been intercepted by drilling only, with intercept grades ranging as high as 50.79 oz/t silver and 0.47% copper. One intercept on the 55 vein at the 5200 level assayed 223 oz/t silver over 0.5 feet. The main 306 vein and all the newly discovered veins remain open at depth.

Sunshine Mine

The venerable Sunshine Mine has been used and misused over the decades and, in turn, has broken the pick of many who treated her badly. Once one of the world’s largest silver mines, the Sunshine produced over 360 million ounces of silver in its 100-year history until 2001 when its owner filed for Chapter 11 bankruptcy.

Prior to closure, the mine was producing about 3 million ounces of silver per year at an average grade of 20 oz/t. Silver was selling for $4.39 per ounce at the time of closure. In 2003, the property was leased to Sterling Mining Company, which commenced an exploration program, along with rehabilitation of underground workings and facilities, most particularly the Jewell Shaft Hoist, the Silver Summit Mine Hoist and the mile-long drift connecting the Sunshine workings to the Silver Summit (Idaho’s Silver Valley section). Sterling initiated production in December 2007, but closed the mine again a few months later and filed for bankruptcy. Thus began a series of attempts by several companies to gain control of the mine.

Dallas- based Silver Opportunity Partners, backed by an eccentric billionaire named Thomas Kaplan, acquired the property for $24 million. The company’s emphasis is expected to be exploration to build the resource base, rather than immediate production.Over 30 veins have been mined at the Sunshine, most notably the Sunshine and Chester veins. An independent study by Behre Dolbear & Co. determined the remaining Sunshine resources to be 6,664,217 ounces of silver measured, and 24,490,138 ounces indicated, with an additional 231,528,312 ounces inferred in veins with average grades as high as 110 oz/t.

A number of exploration targets exist within or adjacent to old workings.A permitted tailings dam exists on the property, but tailing disposal and discharge of mine wastewater to the South Fork of the Coeur d’Alene River are critical environmental issues for the mine.

Crescent Mine

Across the Big Creek Valley from the Sunshine Mine, United Mining Group is advancing an aggressive plan to rehabilitate the historic Crescent Mine. Bunker Hill operated this mine from about 1917 to 1981. Extensive workings were developed and 25,139,655 ounces of silver were produced.

This historic production came both from below and above the Hooper Tunnel, which served as the main access. The now-flooded workings below the Hooper tunnel are not included in United Mining’s near-term plans. Present efforts focus on finding and mining ores above the Hooper Tunnel in the Alhambra and South Veins, which can be extracted without hoisting or dewatering the old workings.United Mining, which is earning its interest from SNS Silver, inherited the results of an extensive exploratory drilling program conducted by SNS.

To date, United has completed rehabilitation of the Hooper Tunnel, and is well along at driving a new access decline called the Countess Portal, 1,400 feet above the Hooper Tunnel. First production is scheduled for early 2012. There is no mill on the site, so United has negotiated an agreement with New Jersey Mining Company to utilize its flotation mill to process ores from the Crescent. United will pay the cost of expanding the mill capacity from 100 to at least 350 tons per day, and it will pay a management fee of $2.50 per ton in addition to the cost of operation. Indicated resources for the Crescent are presently listed as 324,000 tons at 18.7 oz/t silver; inferred resources are 211,000 tons at 19.5 oz/t.

Bunker Hill Mine

No discussion of the Silver Valley would be complete without mention of the Bunker Hill mine, the oldest and largest producer in the history of the valley. Its actual discovery in 1887, the first discovery of a major deposit in the district, is clouded with legend. Ultimately, several deposits were consolidated into one large mining operation, along with a mill, smelter and lead and zinc refineries. The complex operated until 1981 when environmental issues forced its closure. The mine, now surrounded by a superfund site, is presently owned by the New Bunker Hill Mining Co. All levels below the 11 level are flooded. Several estimates of remaining resources have been prepared that range up to 7,336,900 tons at 2.85% lead, 1.58 oz/t silver and 4.95% zinc.

Links and Refereneces

Click here for full list of links:http://go.mining.com/jan11-a1

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments