Gold price hits 4-month low on vaccine hopes, strong US data

Gold fell to its lowest in four-months on Monday as growing optimism over a covid-19 vaccine and signs of recovery in the US economy drove investors away from the safe-haven metal and towards riskier assets.

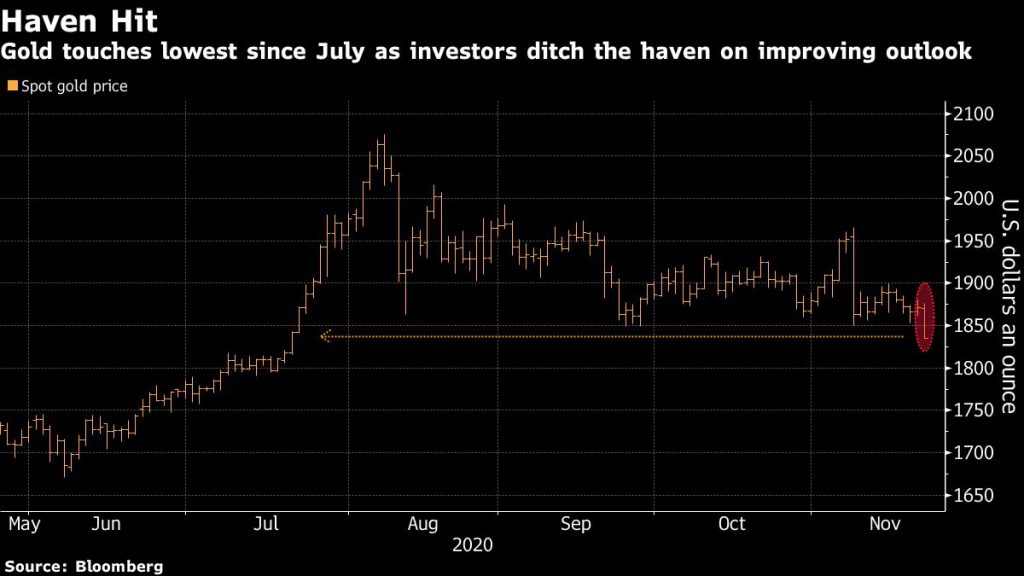

Spot gold declined 1.6% to $1,839.57 per ounce by 1 p.m. in New York, having fallen by as much as 2% earlier in the day. US gold futures were down 1.9% to $1,836.20 per ounce.

Bullion extended last week’s loss after AstraZeneca said its vaccine prevented most people from developing the coronavirus, marking another promising development in the quest to end the pandemic.

Meanwhile, US business activity powered ahead in November at the fastest pace since March 2015, IHS Markit figures showed.

Gold prices have already posted two straight weekly declines, and holdings in exchange-traded funds backed by the metal have slipped recently as hopes for a vaccine buoyed markets and curbed demand for haven assets.

Gold’s break below $1,850 triggered a wave of sell stops, according to Phillip Streible, chief market strategist at Blue Line Futures in Chicago.

“Gold prices broke through technical support, catalyzing a rush to the exits,” Daniel Ghali, a TD Securities strategist, echoed the same sentiment.

“For weeks, capital outflows from ETFs have added pressure to gold markets as a second wave sweeps across the globe, keeping inflation expectations capped, while the vaccine announcements have also seen safe-haven flows reverse,” Ghali added.

“Gold broke below the key $1,850 level after an unbelievably strong US PMI release just dampened the need for stimulus. No one was expecting such strong readings in both services and manufacturing,” Edward Moya, senior market analyst at OANDA, told Reuters.

Gold, traditionally considered a hedge against inflation and currency debasement, has gained over 21% this year, benefiting from the economic damage from the pandemic and the ensuing global stimulus measures.

(With files from Bloomberg and Reuters)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments