Gold dominates mining M&A again in 2024: S&P Global

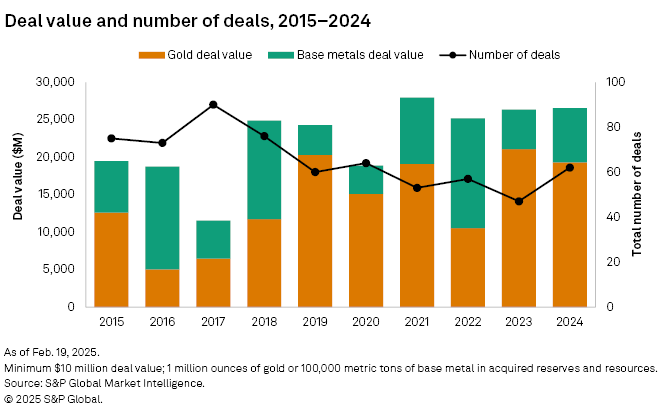

Gold was once again the dominant theme of mergers and acquisitions (M&A) deals within the precious and base metals mining space in 2024, accounting for 70% of the year’s transaction count and total value, says S&P Global.

According to data tracked by S&P, the number of M&A transactions with gold as the primary resource metal more than doubled those in base metals at 43 (versus 19). The total transaction value was also nearly three times higher for gold at $19.31 billion, compared to $7.23 billion for base metals.

While the total M&A deal value of $26.54 billion was roughly the same as 2023 ($26.36 billion), the number of deals in gold increased by 32% from 47 to 62, including 13 more deals in gold. This highlights the increased appeal of gold in 2024 amid escalating geopolitical risks, which sent the metal’s price to multiple records, ending the year with a 27% gain.

The gold deals predominantly involved production-stage mining properties in Australia and Canada — two of the most geographically significant sources of gold. S&P says the two countries maintained their reputation as stable jurisdictions to investors and producers eager to capitalize on gold’s rise.

In 2023, there were already signs of the mining sector pivoting its focus towards gold, which had over two-thirds (30) of the total deals that year. The 2024 figure would mark the second straight year of gold dominance in mining and metals M&A.

*For inclusion in S&P’s database, the M&A transaction must have a value of at least $10 million and 1 million ounces of gold or 100,000 tonnes of base metal (copper, zinc, nickel) in acquired reserves and resources.

No big deals

S&P notes that the 2023 figures were skewed by Newmont’s $16.49 billion acquisition of Newcrest, meaning the 2024 M&A data would have painted an even brighter picture for gold deals. Without the Newcrest sale, gold’s total deal value would have been the highest since 2020, the firm says.

In 2024, there were no such megadeals (defined as those valued over $10 billion), which resulted in the lowest average deal value in five years at $428.1 million, down 24% from 2023. However, S&P points out that transactions involving gold remained consistently high through all four quarters, with at least one high-priced deal announced.

The three largest deals last year were company-level transactions, with a divided focus between gold and copper. The first was the acquisition of De Grey Mining by Northern Star Resources in December 2024 for $3.26 billion, closely followed by the Lundin Mining and BHP Group’s joint acquisition of Canada’s Filo in a $3.03 billion copper-focused deal. AngloGold Ashanti’s purchase of Centamin, priced at $2.48 billion, was the third-largest deal of 2024.

Base metals

Copper M&A activity was mostly muted in the first half of 2024 with only two deals, but the pace picked up in the second half once the metal’s price rose, S&P analysts observed, pointing to the surge in copper prices following an unprecedented squeeze on the COMEX in May.

Of the 16 announced copper deals, more than two-thirds were company acquisitions, with most targets evenly split between Canada and Chile. The largest deal was the Filo acquisition. However, other than that, activity in Canada was largely subdued after its government imposed stricter M&A regulations in July.

Majors were the most prominent buyer for copper assets. Without the billion-dollar deals, 2024’s total transaction value of $5.7 billion would have decreased 6% year over year. Much of the money spent by majors went to assets in the pre-production stage — a surprising turn given the pronounced focus on producing mines the year before. Although copper exploration budgets increased annually in 2024, miners still hesitated to rely heavily on exploration, S&P says.

After a dormant year in 2023, zinc-focused M&A activity returned in a big way with Boliden’s acquisition of two mines from Lundin. At $1.52 billion, the transaction was the largest primary zinc deal in more than five years, which was atypical for the commodity.

On the other hand, the number of nickel-focused deals declined from three to just one in 2024, along with a steep 97% drop in deal value. The lone deal was Horizon Minerals’ acquisition of Poseidon Nickel for $20.3 million.

More M&As

Based on the deals announced in the first quarter of 2025, it is likely that gold will continue to gain traction throughout the year, and that overall M&A activity will be stronger, S&P predicts.

As the critical minerals race grapples with concerns surrounding the Ukraine-Russia war and with trade tensions triggered by US tariff announcements coming to a head, metal prices are expected to fluctuate, especially for gold and copper, the firm says.

This is already seen in Equinox Gold’s February announcement of its acquisition of Calibre Mining for $1.87 billion, it adds.

So far, both metals have rallied during the first two months of the Trump administration. Gold, in particular, scored multiple record highs and recently surpassed the $3,050-an-ounce mark. Copper, mostly on anticipation of tariffs and stimulus in China, is also nearing its all-time peak.

As geopolitical turbulence continues to sway the markets, S&P’s analysts forecast an uptick in slightly more opportunistic acquisitions and supply chain consolidation efforts from players big and small.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

gaston theberge

I realy follow the gold market and i am following 50 different company