Global copper output to grow over the next decade – report

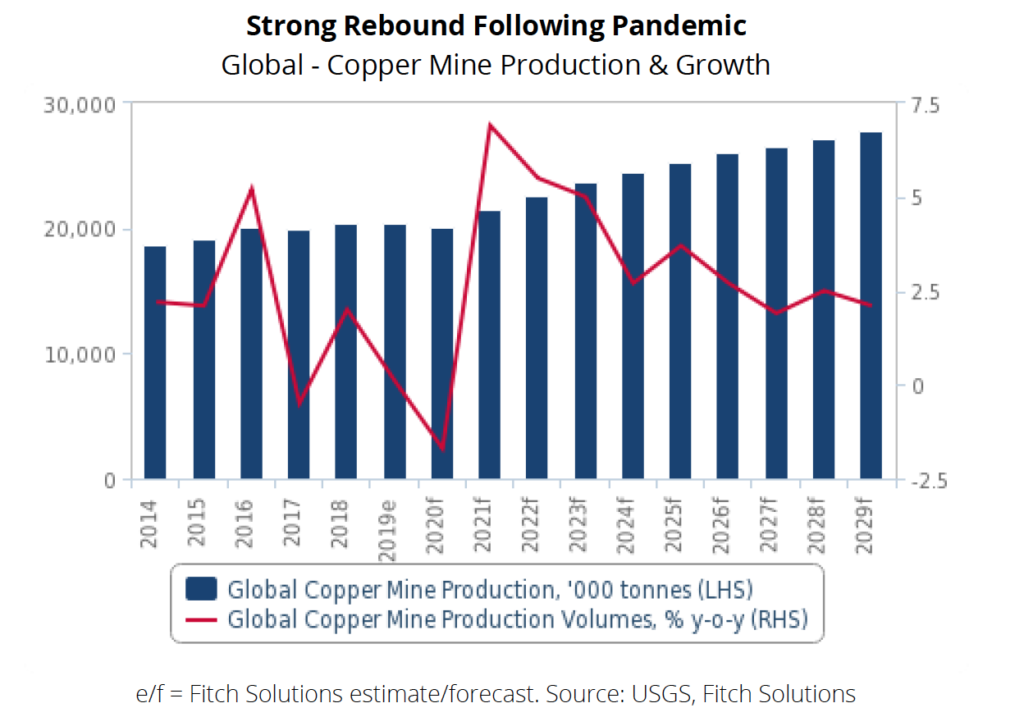

A new report by Fitch Solutions forecasts global copper mine production to increase by an average annual rate of 3.7% over 2021-2029, with total output rising from 21.5mnt to 27.8mnt over the same period.

Year-on-year, the market analyst sees production of the red metal expanding 6.9% as a result of multiple new projects coming online and low-base effects due to covid-19 lockdowns reducing output in 2020.

Leading this growth is Chile, where BHP’s (ASX, LON, NYSE: BHP) Spence Growth Option project is expected to deliver first production between December 2020 and March 2021. The operation is projected to increase payable copper production by 185kt per annum once ramped up.

Fitch’s forecast also takes into consideration the return of most workers to the Escondida mine, although BHP has already said that output will be lower than usual through the 2022 fiscal year as a result of the reduced workforce levels.

“However, the return of workers will boost copper output back into normal range, which the firm is holding at roughly 1,200kt per annum on average,” the report reads. “Furthermore, depending on when the Spence Growth Option project mentioned earlier ultimately begins production and can ramp up to its full run rate, we expect it will also contribute positively to 2022 growth.”

The analyst points out that the copper forecast is also counting on Lundin Mining (TSX: LUG) being able to reach an amicable solution with its Chilean unions by year-end and, thus, not impacting production for 2021.

Lundin projects copper mine production at Candelaria to range between 185kt and 195kt in 2021, which is up from the 142kt produced in 2019 and is slated to be higher than what is produced in 2020.

According to Fitch, growth following 2021 will benefit from the delayed project ramp-ups such as Teck Resources’ Quebrada Blanca Phase 2 project, which is expected to begin production over the second half of 2022.

Project development had been delayed by five-to-six months due to the covid-19 pandemic but has since restarted, and the company now estimates copper production over the first five years will average 286kt per annum.

All of these developments led Fitch to revise up its 2022 and 2023 forecasts to 4% and 3.2% respectively from 2.9% and 1.9% previously.

When it comes to Peru, the world’s no. 2 copper producer, Fitch expects its outlook for copper mine production to bounce back strongly in 2021, growing by 20% y-o-y, as a result of strong low-base effects and new projects coming online.

Chinese investment will play an increasingly important role in Peru’s copper sector

The Andean country currently has 48 mining projects at different stages of development and another 54 exploration projects.

“Peru is tied for second for the world’s largest copper reserves at 87mnt as of 2019, 10% of known reserves,” the report reads. “We believe Chinese investment will play an increasingly important role in Peru’s copper sector. Miners are seeking to diversify their supply chain to compensate for Chinese domestic consumption being greater than their supply.”

Based on official information, Peru is expected to see $10.2 billion invested in five mining projects over the next decade by Chinese firms.

China and the DRC

Within China, copper production is expected to increase at an average rate of 1.5% per annum over 2021-2029, compared with an average growth rate of 4.6% over the past 10-year period.

The market analyst says that this slowdown in production growth will be driven by closures of low-grade copper mines and delayed planned capacity expansions.

Despite this outlook, domestic copper production is expected to be positive as new projects come online and the Asian country develops foreign assets to improve its resource security.

Kamoa-Kakula is set to be one of the largest contributors to growth within the DRC’s copper sector

“Chinese copper miners will remain committed to investing in copper deposits abroad to secure access to high-grade, low-cost material,” Fitch states. “For instance, in October 2019, Zijin Mining announced that it would spend $146 million to increase its interest in Ivanhoe Mining. The purchase will make Zijin the second-largest shareholder in the company developing the Kamoa-Kakula copper mine in the Democratic Republic of the Congo.”

Kamoa-Kakula, on the other hand, is set to be one of the largest contributors to growth within the DRC’s copper sector, whose production is expected to grow 12% y-o-y in 2021, following a 3.5% contraction in 2020.

The prediction is based on the fact that, in August, Ivanhoe Mines (TSX: IVN) reported that the development of the Kakula copper mine had been progressing ahead of schedule, with the firm expecting to achieve first copper concentrate in Q321.

This and other projects, together with steady output from China Moly’s Tenke Fungurume mine and Glencore’s (LON: GLEN) Katanga mine, are the foundations of Fitch’s forecast, which takes into account Glencore’s decision to idle the Mutanda copper-cobalt mine from 2020 to 2022.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments