Global battery demand to quadruple by 2030 — report

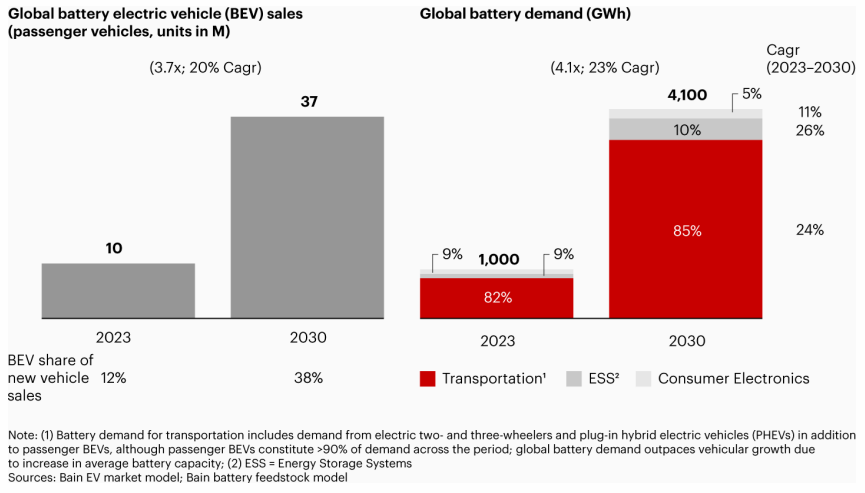

Global battery demand is expected to quadruple to 4,100 gigawatt-hours (GWh) between 2023 and 2030, according to a new report by Bain & Company.

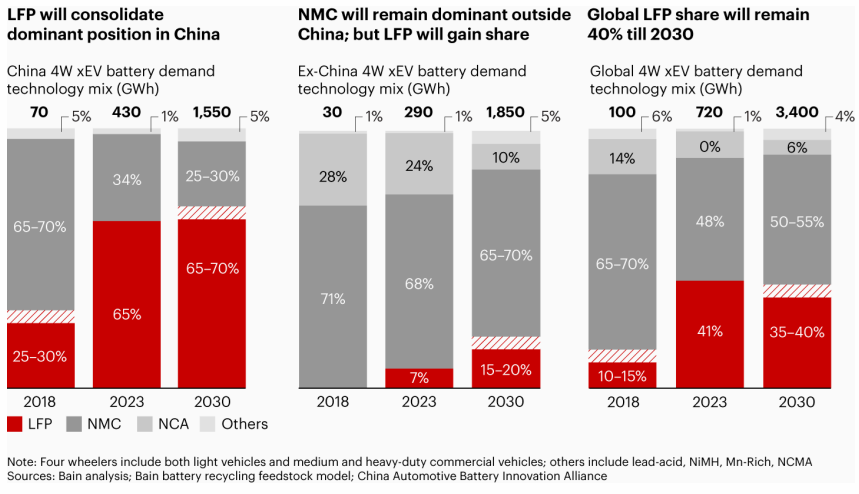

According to the report, lithium-ion batteries will remain dominant for the foreseeable future.

The report highlights that nickel manganese cobalt (NMC) and lithium-iron phosphate (LFP) will be the dominant cathode chemistries. LFP and NMC chemistries together currently make up more than 90% of lithium-ion battery sales for EVs.

“Emerging technologies such as solid-state and high-density sodium-ion are still in the prototype and pilot manufacturing stages, and their market share is expected to stay in the single-digit range until 2030,” the firm said.

“Batteries are the single biggest cost driver for OEMs and they influence product performance. However, ongoing flux across battery chemistries, especially within lithium-ion batteries, is affecting OEM product roadmaps,” said Mahadevan Seetharaman, partner at Bain & Company’s advanced manufacturing services practice.

“OEMs across the world face the critical choice of which battery type to use and whether to develop batteries in-house or through collaboration with other companies.”

According to the global consultancy, LFP will become more dominant in China due to robust demand for mass-market EVs and established supply chains, in addition to the emergence of LFP variants with improved energy density, such as M3P and lithium manganese iron phosphate (LFMP).

In the USA and EU, LFP will gain share but will still be lower than that in China for multiple reasons, according to the report.

“First, domestic LFP production is nearly nonexistent, and existing iron and phosphorous supply chains are significantly less mature in these regions compared to those in China. Consequently, the cost advantage of LFP versus NMC will be undercut by the costs of importing LFP from China,” the report states.

“In addition, many companies are looking into no cobalt or low-cobalt NMC variants, which would further reduce the cost advantage of LFP.”

Finally, import tariffs and broader geopolitical challenges may make LFP less suited for Western OEMs looking to build more resilient supply chains.

Bain says solid-state and sodium-ion will be the only commercialized emerging technologies by 2030. The consultancy firm expects commercial availability of sodium-ion-based EVs by the first half of 2025.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments