Fresh iron ore price plunge

Relentless selling continues with iron ore price falling more than 2% on Monday. Next stop $45 a tonne says new report.

The spot price of iron ore fell further into uncharted territory on Monday with the steelmaking raw material declining to the lowest since the inception of the spot pricing system amid a widening supply glut and fears about demand from top consumer China.

The 62% Fe import price including freight and insurance at the Chinese port of Tianjin lost $1.20 or 2.2% to $52.90 a tonne on Monday. After giving up 47% in 2014, the price of iron ore is now down another 25% this year.

Monday’s peg was the lowest price since November 2008 when The SteelIndex, a unit of Platts, first started tracking the spot price. In 2008, the benchmark contract price was $60.80 a tonne, which was hiked from the annually-set price in 2007 of $36.63.

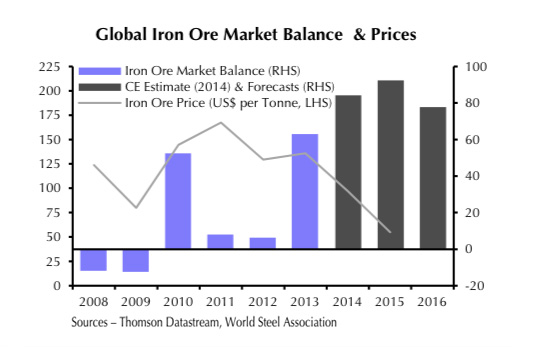

Steel consumption in China which imports more than 70% of the world’s iron ore fell last year for the first time since 1995 and the slowdown has coincided with a flood of new supply.

Led by the Big 4 – Vale, Rio Tinto, BHP Billiton and Fortescue Metals Group – iron ore miners invested north of $100 billion in new projects and expansions since the start of the decade which pushed the market into surplus late 2013.

Oversupply is not going away soon either. The majors which enjoy cash costs on only around $20 a tonne have been pushing out marginal producers in their home bases and elsewhere, but a new report by Capital Economics suggests the rebalancing is not likely to go smoothly.

According to Caroline Bain Senior Commodities Economist at Capital Economics in London “the ensuing large surpluses will put further downward pressure on prices” prompting the independent research house to slash its iron ore price forecasts for end-2015 and end-2016 to $45 and $50 per tonne (from $60 and $70 previously).

CRU, a commodities research company, estimates that more than 50 million tonnes of existing supply will need to be removed from the market this year alone before a turning point for the industry can be called.

Expectations have been that China’s domestic mines which number roughly 1,500 and produce some 350 million – 400 million tonnes a year on a 62% Fe-basis would be the main victims given sub-20% Fe grades and low tech operations.

While a huge number of Chinese iron ore miners have shut up shop, the country’s supply is proving too be stickier than anticipated. That’s due to long term agreements and captive mines and the close relationship between local governments, steel mills and miners which means commercial imperatives often take a back seat to other considerations like jobs retention.

Source: Capital Economics

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

5 Comments

Mark Harder

Sorta dumb question, but what is meant by a price per ton(ne) of iron “ore”? There are all sorts of iron ores, with different iron concentrations. How are these effects normalized? Is it really a price per ton of iron metal content? What?

david c Wold

It sounds very depressing considering how much money has been invested in new/smaller mines world wide, many financed by ‘venture capital’. Smaller mine do not only have the disadvantage of higher per mt start up cost, but their shipping cost is about ‘double’ of what the large 4’s . Result is that large new communities in W.Africa , Indonesia, Mexico, South and Central America – (who recently got jobs in the new mines, transport and export) would go without income . Mining is for many countries their largest source of export revenue and work. On the other hand with such cheap raw material we again see China dumping cheap steel on the USA and Europe ‘killing’ any home grown steel industry.

valakos

i see a price of $45 being the trigger for a wider “change” in Australian economy

jorge castro

Me parece que el actual nivel de precio es insostenible para los productores, esto es una crisis de incalculables repecurciones

jorge castro

the cost ex-work for chilian smaller mining around USD24/TON then more land transport, costport an freigh and insurance the finally value CFR TIANJIN +usd 50/ton