Freeport’s Grasberg jujitsu move will pay off

By David Fickling

(Bloomberg Opinion) — There’s a well-thumbed playbook for how deals involving gold mines in the remote jungles of Indonesia are meant to turn out.

The game plan isn’t so different to the plot of the recent Matthew McConaughey film “Gold” – a promise of great wealth turning to ruin with the protagonists ending up brawling in the mud surrounded by fraud, violence and shady political involvement.

For several years, Freeport-McMoRan Inc.’s tussle with Jakarta over the world’s biggest gold deposit and third-biggest copper reserve at Grasberg in the New Guinea highlands has seemed to be headed in a similarly disastrous direction.

Combined with the government’s existing stake and a relatively minor shift in Freeport’s holding, that should be enough to get Jakarta to the 51 percent it wants.

Indonesia’s government has been determined to convert its 9.36 percent stake into majority control, and has used every regulatory trick under the sun to threaten Freeport’s business and bring it to the table at a discount price – from export controls and mining contracts to last-minute environmental reviews.

This wrangle looks to be finally approaching an endgame. Rio Tinto Group is ready to accept a $3.5 billion deal that would transfer its 40 percent interest in the mine to state-owned PT Indonesia Asahan Aluminium, or Inalum, people with knowledge of the discussions told David Stringer and Danielle Bochove of Bloomberg News. Combined with the government’s existing stake and a relatively minor shift in Freeport’s holding, that should be enough to get Jakarta to the 51 percent it wants.

From one perspective, this outcome for Phoenix-based Freeport may not be that much better than for McConaughey’s fictional Reno-based company. It will be losing control of the mine – as well as several years of cash flow – in return for what’s likely to be little more than a peppercorn payment. Looked at in the long term, though, it may be a result that pleases every party.

From one perspective, this outcome for Phoenix-based Freeport may not be that much better than for McConaughey’s fictional Reno-based company. It will be losing control of the mine – as well as several years of cash flow – in return for what’s likely to be little more than a peppercorn payment. Looked at in the long term, though, it may be a result that pleases every party.

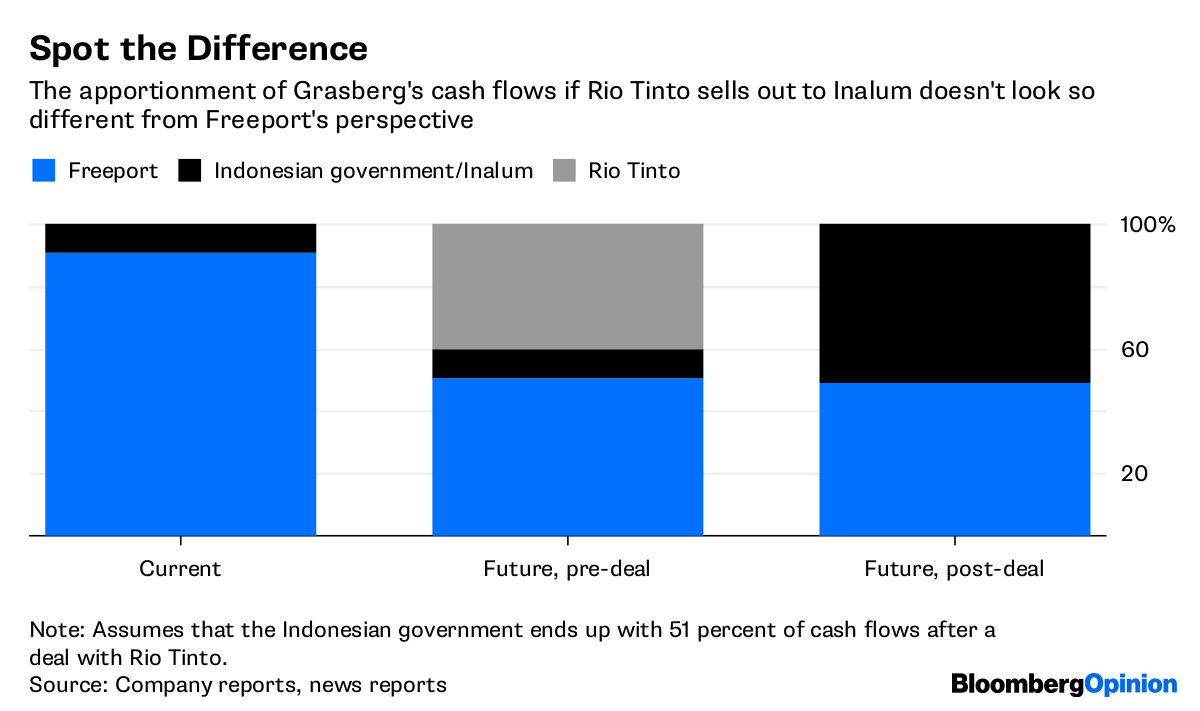

To understand why, look at Grasberg’s shareholder structure. Freeport controls 90.64 percent of the equity, and the Indonesian government the remainder. Rio Tinto’s stake is not in Grasberg itself, but in the project that will expand the underground mines into an operation producing about a billion pounds of copper and a million ounces of gold a year.

In practice, Rio Tinto tends to get almost nothing except for a share of capital expenditure

In practice, Rio Tinto tends to get almost nothing except for a share of capital expenditure – but if output goes over certain levels, it’s entitled to 40 percent of that – and after about 2023 it gets 40 percent regardless of any hurdle levels.

Rio Tinto has made no secret that it’s not wedded to this stake. Chief Executive Officer Jean-Sebastien Jacques has frequently acknowledged that Grasberg is a world-class deposit but not necessarily a world-class business (the former is defined by geology; the latter, by the political and economic risk involved in getting the metal out of the ground).

Having sold out of coal and with hopes to put its run of African scandals behind it, Rio Tinto is busy making itself over (not entirely convincingly) as the ESG play in the mining industry. Converting a politically risky asset targeted by environmental groups and independence fighters into $3.5 billion of cash to shower over Rio’s grateful shareholders seems like a no-brainer.

For Indonesia’s President Joko Widodo, the deal also makes sense. With provincial and presidential elections looming, he’ll have won symbolic control of a prized national asset at a price that looks much closer to the $8 billion equity value Jakarta has been putting out than the higher figures promulgated by Freeport.

What, though, of Freeport? The tiny sum it’s likely to receive for its sliver of equity next to the $3.5 billion going to Rio Tinto feels like a slap in the face, and might undermine the 13 percent run-up in its share price so far this month.

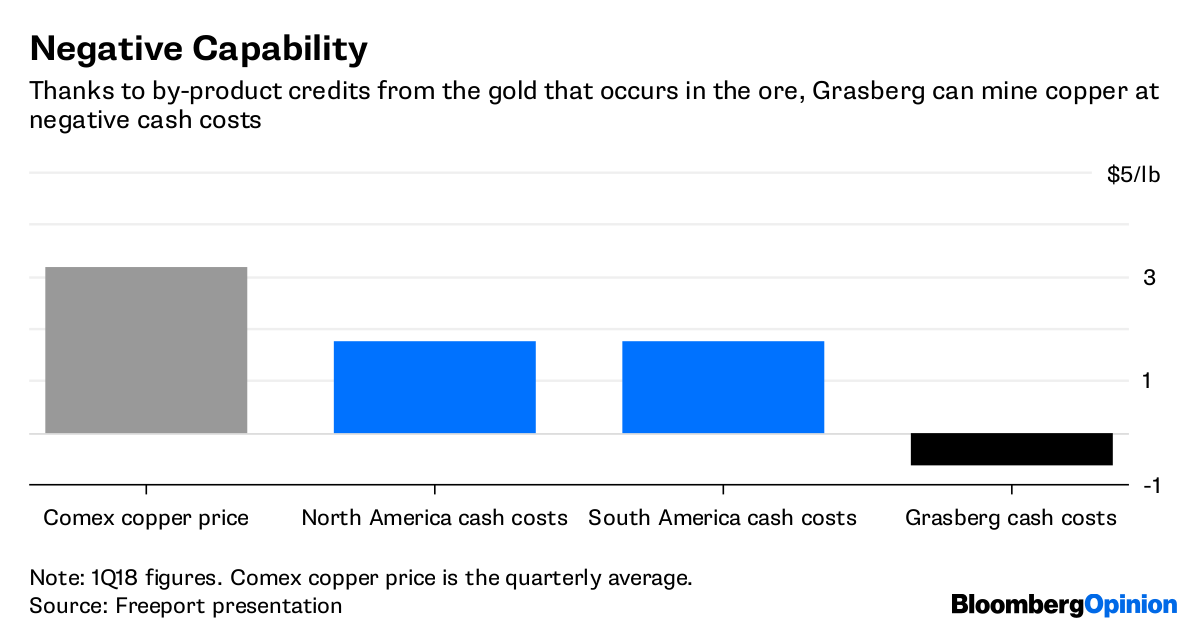

Look further out, though. Grasberg is still one of the world’s most magnificent mineral deposits, producing copper at negative cost as a result of revenues from the gold by-product alongside it.

Mining assets are valued in terms of discounted cash flows, and Grasberg’s current license runs until 2041. In the long term, Freeport retains operational control, and the difference between the 50.64 percent share of cash flows it would have received had it been able to hold its ground and the 49 percent share it will now get looks like a rounding error.

The value of globally unique deposits like this should be measured in decades, not years. By appearing to give way, Freeport has carried out the jujitsu move of finding strength in apparent weakness. A small sacrifice now over equity valuation will pay handsome dividends far into the future.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Tony

How much to buy stock.

Mike Failla

Okay but still a ways to go. Looking towards the future this may work out better. Time will tell but it is always wise to look and anticipate governmental/political chicanery.