Forecasts for uranium price all point up

Have your yellowcake and eat it

Uranium was the glaring exception amid a broad-based rally in metals and minerals in 2016. The price of U3O8 fell 41% in 2016 with the industry tracker UxC’s broker average price hitting 12-year lows below $18 per pound in November.

After top supplier Kazakhstan announced in the second week of January that it’s cutting output by 5.2 million pounds, equal to 3% of global production, the price rallied, hitting $26.75 a pound by mid-February.

But Japanese utility TEPCO’s declaration of force majeure on a key uranium delivery contract from Cameco Corp. (CCO-T), the world’s top listed uranium producer, dampened enthusiasm.

And news in April that the US dept of Energy is making cuts to the amount of uranium that it disperses into the market (as much as 1.1m pounds per year less) did little to buoy sentiment, not to mention bad news surrounding nuclear power including the first new reactor to be built in the UK in a generation and risks to the US industry.

Last week Russian state nuclear corporation Rosatom suspended its Mkuju River uranium project in Tanzania for at least three years due to depressed uranium market.

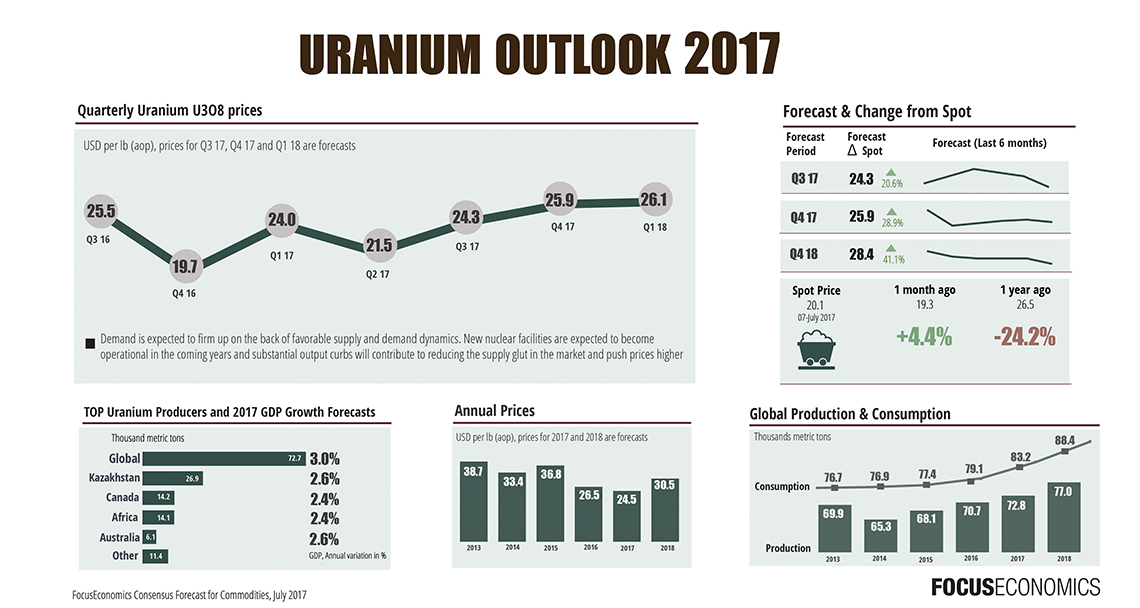

Spot uranium rose to $20.75 this week but remains technically in a bear market, trading down more than 20% from its February peak. Despite the current negativity analysts surveyed by FocusEconomics in July predict a steady increase in the price from today’s levels rising by 40% by the end of next year and over $40 a pound in 2020:

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

patentbs

The Tanzanian project suspension was due to other considerations as much as price. That was a self inflicted wound to the nation.