Fading US rate hike expectations point to $1,300+ gold price

On Thursday, gold showed some resilience after signs of ever-looser monetary policy in Europe led to to a rally in the US dollar.

On the Comex market in New York, gold futures with December delivery dates were largely unchanged compared to yesterday’s close at $1,166.90 in cautious trade ahead of next week’s crucial Federal Reserve interest rate decision. Gold remains up some 5% from where it was trading before the US Federal Reserve at its September meeting decided not to lift rates from near-zero, where it has been since the global financial crisis.

None of the economic data out of the US released this week gave much support to the hawks or the doves on the Federal Open Market Committee to raise rates for the first time in nine years, but the expected rate at the end of next year have been steadily adjusted downward beginning in the second quarter.

Interest rates have a strong negative correlation to gold and the relationship has only gotten tighter since the 2008/09 crisis. The underlying reason for the relationship is that as yields rise, the opportunity costs of holding gold increases (and its relative attractiveness as an investment) because the metal is not income producing.

Higher rates also boost the value of the dollar which usually move in the opposite direction of the gold price. On Thursday the greenback jumped 1.4% (a huge move on a market which usually fluctuates only be a few basis points on a daily basis) to its best level against major currencies in over three weeks after the European Central Bank hinted at possible expansion of its program of quantitative easing.

Should the Fed raise rates, or even just strengthen the case for a rise in December or next year, and the ECB start printing even more money it would give a fresh boost to the dollar which is already up 11.4% compared to this time last year.

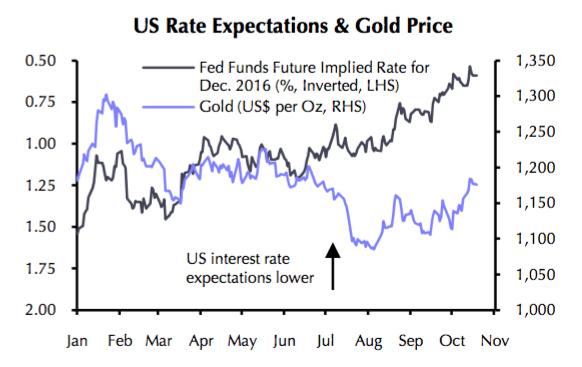

This chart from Capital Economics shows just how far the gold price and interest rate expectations have diverged. The gold price has not caught up to interest rate expectations that have gone from 1.5% at the start of the year to closer to 0.5% today.

The conventional wisdom is that the gold price is bound to fall sharply as well when US interest rates are hiked. However, gold has already underperformed relative to what might have been expected given the Fed’s hesitancy thus far. We suspect this partly reflects the lack of demand for inflation hedges as the past weakness of oil prices keeps headline inflation low. Correspondingly, if we are right that oil prices are set for a gradual recovery, gold should benefit too.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Swiss Freiherr

Gold (6000 years bc – still a world currency). The greenback is a piece of cotton (1971 — 2017/2018??) ‘Money for nothing’ Dire straits 🙂

Jan Jee

Rate hike or not, Gold will go up, so will pretty much all the (natural) resources. My dilemma is whether things like NUGT and AGQ are safe short/mid term. My portfolio is pretty well diversified and physical is the ‘only way to go’ but what will happen to the dollar? Currencies are on a race to the bottom and I don’t like to have anything denominated in dollars or euro’s or pounds.. just cold hard sound money like silver and gold but the risk/reward in NUGT and AGQ might be an interesting speculative play short term.