Exports can’t save US coal

Between late 2010 and the end of 2014, the top ten publicly-traded coal companies in the US saw their combined share price value drop by more than half, as hundreds of plants closed and thousands of employees were laid off.

The US coal industry – struggling to compete with cheap natural gas at home – turned to exports to take up some of the slack in the domestic market. From less than 5 million tons of steam coal exports in the first quarter of 2009, shipment rose to 17.4 million tons by the second quarter of 2012.

But cargoes have been declining since then with first quarter exports this year less than half the peak three years ago. Over the same period coking coal exports are down nearly a third. The US now commands less than 1% of the 900 million tons seaborne thermal coal trade.

Aside from a small number of high-productivity longwall mines, operations in the US are predominantly in the 4th quartile of the seaborne thermal coal cost curve according to a new report by CRU Group which covers more than 300 mines and projects globally.

Reasons for this lack of competitiveness are plenty says the mining and commodities research company:

“US mines were already comparatively high-cost due to factors such as high distances to export facilities (e.g. the Powder River Basin mines), difficult geology and high legacy workforce costs (e.g. Appalachian mines), but the appreciation of the US Dollar is what is hurting coal producers there most. ”

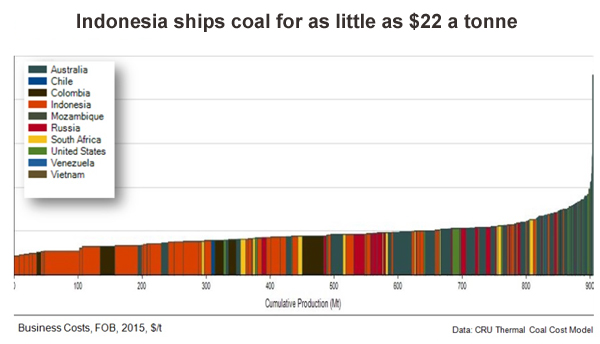

CRU says free on board costs for global producers range from a low of $21.9 per tonne to a high of $116.2 per tonne for ongoing operations.

Indonesia is the undisputed leader in the seaborne thermal market. The Asian nation dominates the 1st quartile due to the availability of abundant and cheap labour, low-cost river barging, capital-light operations and the ability to sell run-of-mine coal, without the added expense of washing says CRU.

CRU’s analysis of the margin curve, based on our estimate of the average annual prices, finds that “around 30% of seaborne production sold on a delivered basis into its natural market is expected to be loss-making in 2015.” Many of these unprofitable mines are in the US and Australia.

Source: CRU Group

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

5 Comments

Mike Failla

As for the U.S. we have a president and his “cabinet” who believe they can fix the climate (which isn’t broken or likely to be anytime soon) by decapitating coal in the united states and that will fix everything. As I recall he publicly stated he would kill the coal industry.

Mike Failla

Yeah I read it and added my 2 cents. What is your point fred? You think that political shenanigans had nothing to do with it as well?

Mike Failla

Read it. Understood it and added my 2 cents as to what else was part of the reason coal was on a downturn. transportation and transport.. Not wanting to start a war here fred but I don’t have a particular agenda but I do observe what is going on and politics is a large part of it, whether you agree or not. I will not be posting a link as all the speechs are on public record. I don’t need to defend myself. If you don’t care for politics (don’t blame you) great but don’t take it out on me okay?

fred garvin

That’s ok, you don’t have to defend yourself. I’m just messin with ya because I’m bored. I follow politics quite closely, and I knew you’d have a hard time with that quote because it doesn’t exist. I’m also a geologist that comes from coal country. Obama makes a fun target for getting folks riled up about the demise of coal, but you’d be closer to the truth if you were blaming Chesapeake Energy and their ilk. Politics’ role in the price of coal is miniscule. Obama actually continued the practice of mountain top removal mining, against his campaign promises and much to the dismay of his supporters. Check it out when you have time. It was related to his efforts to keep WV from flipping back to the Republicans. If anything, that’s where this was most political; his support rather than lack thereof for coal.

Mike Failla

Don’t mind a bit of mess. I am in total sympathy with miners. I was one for many years and still work with them.(Though now in the education and training end of things). I feel their pain in this economy though! What i was referring to was the comment “sure you can have your coal and power but it will cost you more”. That was one of them anyway. yeah Obama makes a good target thats for sure. Some of these policies are just killing the mining industry. 10 years on average for permitting? Now we are seeing layoffs in the copper sector also.It is an economy thing but do federal policies, taxes etc affect miners? I think they do. Freeport McMoran and Asarco are laying off miners. been through it many times and it always hurts but you know we rise up and keeping on doing what we do best. anyway no harm no foul! Time for coffee!