EV momentum ‘unstoppable’ – report

The momentum behind cleaner, software-enabled forms of mobility is unstoppable, a new report by McKinsey & Company states.

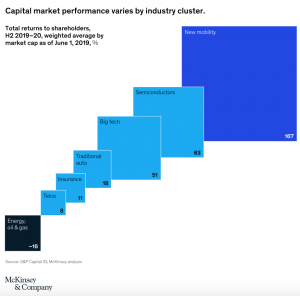

According to the consulting firm, one of the key indicators of this momentum is the mobility industry’s outperformance over top industries, such as semiconductors and big tech, in capital markets.

In McKinsey’s view, besides its ongoing work on autonomous electric vehicles, the industry’s performance is also explained by the fact that it is exploring new avenues, such as shared mobility – which could double in size by 2030 – and advanced connectivity solutions for EVs, like personalized contextual advertising based on driving routes.

The way automotive software is evolving is also pushing the industry’s positioning in the stock markets.

“We estimate that the automotive software market will have grown by approximately 250% by the end of the decade. This will put software at the very center of new automobile designs,” the report states.

McKinsey says Chinese buyers are driving the interest of automakers in innovative software that incorporates facial recognition, avatars with location-enabled recommendations, voice commands, in-car payment options and apps, among other features.

The green push

Although it seems evident, EV makers’ objective of reaching zero emissions has also been key in pushing up their shares, particularly because of their recent focus on cutting both tailpipe emissions, which account for two-thirds of the total, and emissions from production, the remaining third.

“Consumers factoring sustainability into buying decisions helped drive EV sales up 43% in 2020,” McKinsey’s report states.

Many of these consumers, the review points out, want to support the goal of limiting global warming to 1.5°C by 2035, which will require 95% of all cars and trucks on the road to be zero-emission vehicles by then.

OEMs are expected to turn their attention to supply chains

With these targets in sight, OEMs are expected to turn their attention to supply chains, encouraging material providers and in-plant processes to become carbon-free.

“There are a number of promising efforts, like the development of ‘green’ steel, and the location of battery plants close to OEMs to lower carbon transport costs,” McKinsey’s report reads. “Some such plants are even powered with carbon-free, water-generated electricity.”

While this type of infrastructure becomes the norm, the analyst says low-carbon fuels, hybrid vehicles and more efficient gas-powered cars are likely to play an important role in the transition to a zero-emission global vehicle fleet.

“Holding emissions under the 45 gigaton target will require a cross-industry effort among companies, industries, and government. For instance, the energy and transport sectors can work together to drive smart-charging technologies that would in turn accelerate the shift to EVs. Coalitions can be formed to develop clean supply chains for the creation of low-carbon battery solutions that reflect the full potential of a circular economy,” the analysis suggests.

For the experts at McKinsey, the need for regulators and policymakers to intercede may become evident in the near future and they may need to adopt an ecosystem perspective with cross-border goals and meaningful timelines for all elements involved in the transition, from the number of charge points needed to the trajectory of carbon reduction.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments