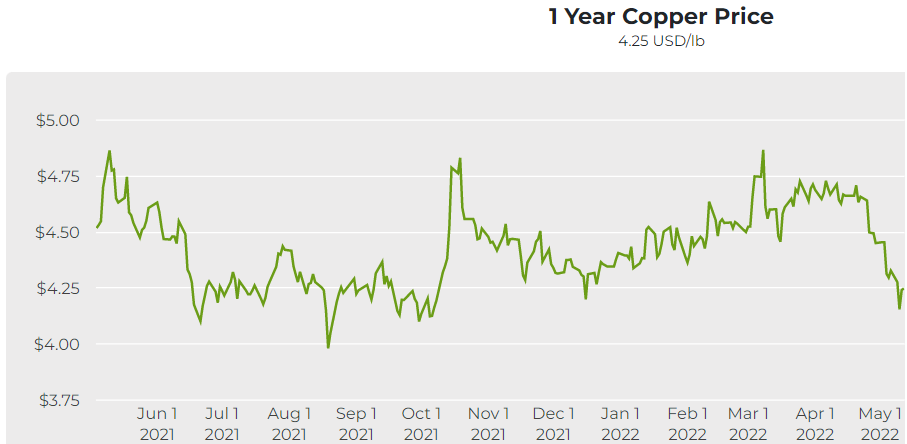

Copper price hits 8-month low on slowdown fears

Copper prices tumbled on Thursday to their lowest in 8 months as traders worried that a slowing global economy would require less metal.

With inflation surging and interest rates rising, growth fears also pushed down oil prices and stock markets hit a one-and-a-half-year low.

The dollar, meanwhile, reached a new 20-year high against a basket of major rivals, making dollar-priced metals costlier for buyers with other currencies.

The yuan fell to its weakest against the dollar since September 2020, making metals costlier in China.

Copper for delivery in July fell 2.6% from Wednesday’s settlement price, touching $4.10 per pound ($9,020 per tonne) midday Thursday on the Comex market in New York, the lowest since September.

Click here for an interactive chart of copper prices

“Demand hopes have given way to demand concerns,” said Commerzbank analyst Daniel Briesemann.

Covid lockdowns in China, the war in Ukraine, and aggressive interest rate rises were all hurting the outlook for the economy and metals demand, he said, but added that the sell-off was likely overdone in the short term.

Sunac China became the latest Chinese property developer to default on a bond payment, adding to a wave of defaults in the sector.

A senior Chinese official said the country is eyeing new incremental policies to prop up growth and will take steps when necessary.

“Hedge funds are turning increasingly bearish on the copper market amid mounting evidence that global manufacturing activity is starting to stall,” wrote Reuters columnist Andy Home.

“Bears now outnumber bulls on the CME copper contract for the first time since May 2020, when the copper price was just starting to recover from the first wave of covid-19 lockdowns.”

(With files from Reuters)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments