Copper price: four Chinese bear charts

September copper lifted its head over the last week and is now only just trading above the $4.00 per pound ($8,800 per tonne) level in Chicago.

The price of the bellwether metal is still down more than 20% from its intra-day peak struck mid-May following a short squeeze, primarily played out in US markets. Year to date gains are all but wiped out.

Copper’s fall since the squeeze was squoze compares to bandwagoners eager to jump on the next big thing calling for $15,000 early next year and $40,000 a tonne in the “not too distant future”.

Those who caught copper fever added demand from artificial intelligence data centers and military spending to the often trotted out energy transition.

Fair enough, but before the mining industry finally enters copper nirvana, the next few years are likely going to be brutal.

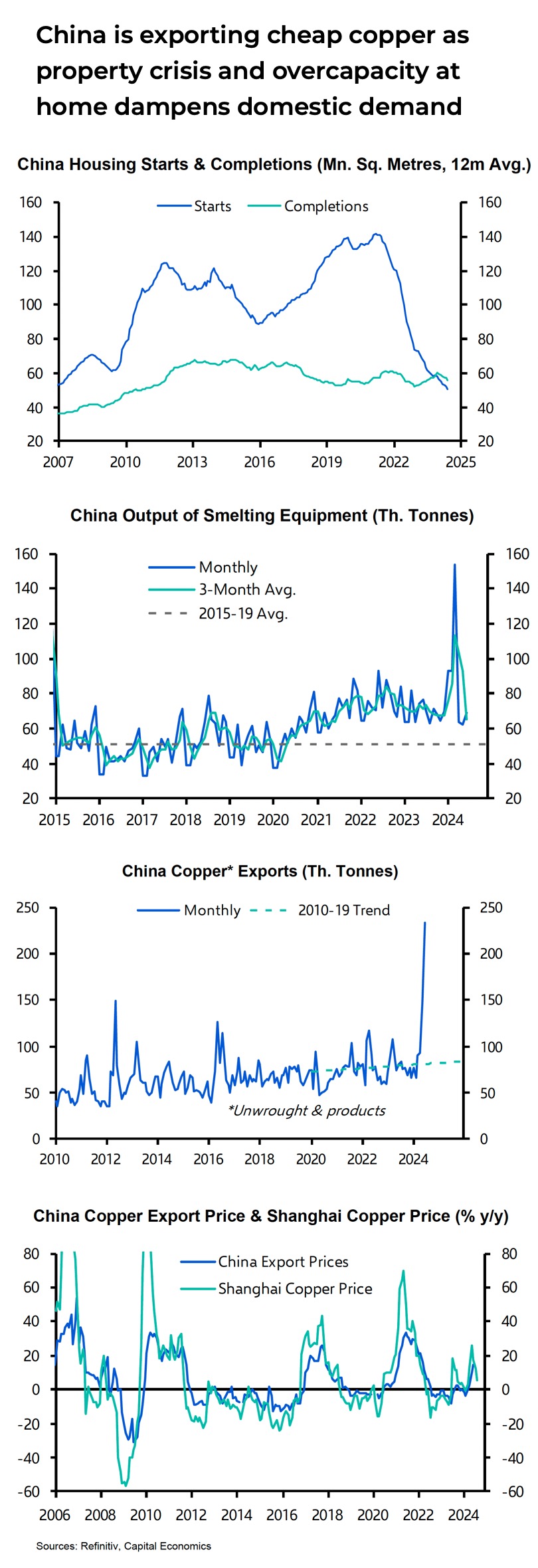

A new note from Capital Economics reminds industry watchers that copper’s fortunes hang on China.

More specifically, the country’s construction sector and its smelters (talk of output cuts was the spark that first lit up the market).

The London-based researcher says rather than a slowdown in the US, the “slow-moving crisis” in the property market in China and ongoing overcapacity will drive copper prices lower.

Output from China’s smelters responsible for more than half global output will remain high and ample exchange inventories will see the country’s copper export prices drop, dragging down prices on global exchanges.

While base metals should get a lift towards the end of the year as China steps up government borrowing and infrastructure spending over the last few months of 2024, by the end of next year copper will be back below today’s levels.

So not $15,000 then.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments