Coking coal price finally breaks fall

On Friday, Chinese traders returned to financial markets after the lunar new year break welcomed by a surprise interest rate announcement from the People’s Bank. It’s the latest sign that Beijing’s stimulus efforts are coming to a close and that stoking economic growth is no longer the number one priority.

Friday’s Caixin manufacturing PMI reading was also a disappointment showing Chinese manufacturing activity are losing some momentum at the start of 2017. The reading came in at 51.0 in January, down from the near four-year high of 51.9 that it hit in December and below expectations.

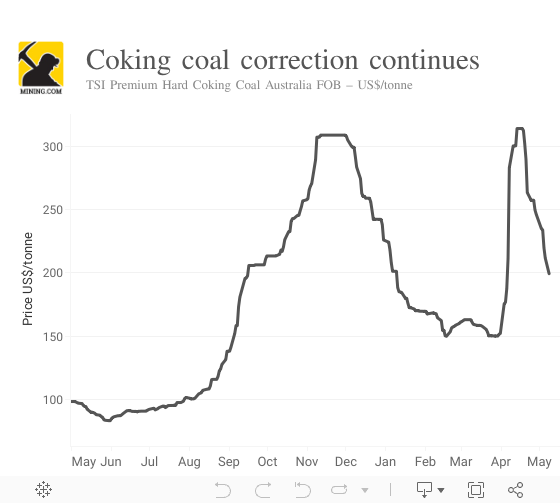

Nevertheless after 12 weeks of non-stop declines traders on Friday finally pushed the price of coking higher, albeit only by a few cents. The steelmaking raw material broke its fall at $167.80 on Friday, still $140 below its multi-year high of $308.80 per tonne (Australia free-on-board premium hard coking coal tracked by the Steel Index) hit in November.

Indian consortium plans to restart Benga mine in Mozambique bought from Rio Tinto for a fraction of Melbourne company’s original purchase price

There was a more than $100 differential between the spot price average and the fourth quarter contract benchmark, but that situation has now completely reversed. Benchmark contract prices for the Q1 2017 were settled between Australian miners and Japanese steelmakers at $285 a tonne.

While the rally and subsequent pullback has created uncertainty in the market, supply is beginning to respond to higher prices.

Earlier this week International Coal ventures (ICVL), a consortium of five state-run coal mining operations, announced plans to restart operations at the Benga mine in Mozambique according to a report in the Financial Express.

ICVL acquired control of Benga mine and two green-field coal assets (Tete East and Zambezi) in 2014 from Rio Tinto. The assets have an estimated coal resource of 2.6 billion tonnes and in its current form Benga can produce 5.3 million tonnes per year. Mining was suspended in May when met coal was trading below $100 a tonne.

Rio Tinto acquired the Benga mine and other coal projects in the Southern African country’s Tete province in 2011, after buying Australia’s Riversdale Mining for $3.7 billion. But in 2013 the Anglo-Australian giant took an asset impairment charge of $3 billion on the coking coal venture citing challenges in building the necessary infrastructure to bring the project on stream. A year later Melbourne-based Rio sold the assets to an Indian company for just $50 million.

Mozambique’s central Tete province is believed to hold one of the world’s largest untapped coal reserves that has been compared with Australia’s coal-rich Bowen Basin.

The US is also expected to increase its coking coal production in 2017 and that around 9 million tonne of US met coal will be added to the export market. Companies such as Warrior Met Coal, Rosebud Mining and Ramaco already plan to start operations in the new year.

Australian coking coal mines owned by miners South32 and Anglo American are expected to once again produce at full capacity in 2017 following force majeure stoppages in late 2016, while Conuma Coal Resources is restarting production at its Wolverine mine in BC, Canada exporting around 1.5 million tonnes of coking coal a year starting in April.

Despite the pullback metallurgical coal had more than doubled from multi-year lows reached in February last year. Coking coal averaged $143 a tonne in 2016 (about the same as it did in 2013). Consensus forecast is for the price to average about the same in 2017.

In 2011 floods in key export region in Queensland saw the coking coal price briefly trade at an all-time high $335 a tonne.

More News

Column: Iran war exposes fragility of Western aluminum market

March 09, 2026 | 04:22 pm

Venezuela acting government sends mining reform bill to legislature

March 09, 2026 | 04:08 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments