China’s rate cuts to slow copper demand even further — report

Image courtesy of Codelco.

China’s recent moves to cut interest rates could “significantly reduce” its demand for copper, affecting global producers, a paper published by Peking University HSBC Business School warns.

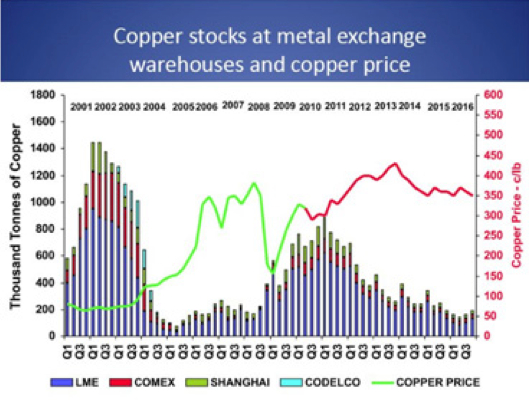

According to the article, there is strong evidence to conclude that copper stocks have been piled up at warehouses mainly “to facilitate a carry trade under capital controls.”

By “carry trade” they mean that speculators have been borrowing dollars to buy Chinese assets, and they often do so with leverage and through convoluted means, some involving use of copper or iron ore as collateral.

The bet is that the Yuan will strengthen, generating a near certain profit on the exchange rate. But this has gone badly wrong as the central bank intervenes to force down the exchange rate.

“Due to the importance of the Shanghai copper holdings for the global copper market, any unwinding or change in interest rate differentials will have significant impact on global commodity market pricing and trading,” warn the authors, Zhang Xiao, a fixed-income analyst with BNP Paribas, and Christopher Balding, associate professor at the Graduate business school.

Citing to data from the Shanghai Futures Exchange, which monitors Chinese stocks, they show that the amount of copper stored in the country jumped from 4% of global stock in 2009 to 38% last year.

According to the paper, for every 1 basis point increase in the onshore-offshore interest rate differential, copper carry trade positions increase by $1.5 million. The problem, it adds, is that during that very same period there were not changes in industrial production to justify such a large variation in inventory.

A puppet with many strings

Graphic courtesy of AQM Copper.

Copper’s fortunes depend not only on demand from China, though the nation is the world’s largest consumer, accounting for 42% of global trade. The red metal is also highly needed on the build-out of the electricity grid, as well as wiring used in cars and consumer goods.

Producers also hope that copper will have a future in electric cars, wind turbines and high-efficiency power transformers.

And unlike other commodities such as iron ore, the world’s largest copper miners have been cutting their production forecasts this year due to disruptions from strikes and engineering issues.

Another plus for copper could come from shrinking supplies of high quality concentrate in the first half of this year, due to disruptions in top producer Chile.

Based on these facts, analysts predict that any further problem will support copper prices, even if Chinese demand weakens.

The metal was trading slightly lower on Friday. Benchmark copper on the London Metal Exchange traded at $5,793 a tonne at 1210 GMT from $5,795 at Thursday’s close.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments