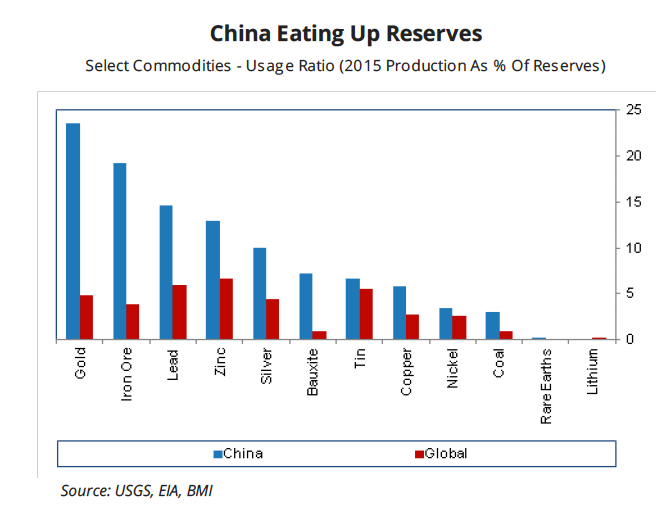

China’s exhausting its gold reserves at 5 times the global rate

China is the leader in extracting gold, zinc, lead, molybdenum, coal, tin, tungsten, rare earths, graphite, vanadium, antimony and phosphate, and holds second place in mine production of copper, silver, cobalt, bauxite and manganese.

At the same time the country is the number one consumer of metals and minerals – in iron ore its imports constitute nearly 80% of use and in copper it’s approaching 50% and for nickel it’s already above that.

The gap between China’s domestic mineral capacity and demand is what is driving the country’s push to acquire overseas mines

China’s reserves-to-production ratio represents the “burn rate” of domestic reserves and it’s not surprising that the country’s elevated consumption levels and increasing dependency on imports are raising alarm bells in Beijing.

A new report by BMI Research says this gap between China’s domestic mineral capacity and demand is what is driving the country’s push to acquire overseas mines:

Notably, China’s production-to-reserves ratios for gold and iron ore are 23.5% and 19.2% respectively. In comparison, global usage rates for gold and iron ore are at just 4.9% and 3.8% respectively.

China surpassed South Africa as top gold producer almost a decade ago and last year produced 490 tonnes of the metal, nearly 200 tonnes more than number two Australia. China in 2013 become the world’s top gold market at 1,132 tonnes and although consumption has shrank since then it’s holding around the 1,000 tonne level.

Domestic Chinese iron ore miners in 2010 supplied 36% of the raw material to the country’s blast furnaces which forge nearly halve the world’s steel. Beijing’s stated goal is to keep domestic mines’ share to around a quarter of the total, but despite tax breaks and other incentives low grades and high costs have seen steelmakers opt for imports.

Source: BMI Research

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

6 Comments

Richard Schodde

An interesting & topical story … but it is totally WRONG … as it is based on poor data. BMI has used production and reserve numbers straight from USGS’s latest Mineral Commodity Summary Report – which, in general, are pretty good, but the problem is that they have great difficulties getting accurate and up-to-date data on countries like China.

The Chinese Government through its Ministry of Land and Resources (MOLAR) publishes annual statistics on their domestic mining industry. These reports can be downloaded from http://www.mlr.gov.cn/zwgk/tjxx/ . Unfortunately, they are all written in Chinese. Table 2.1 in their 2015 Communique report states that, as at the end of 2014 the proven reserves for gold in China totaled 9816 tonnes. This is 5x higher than the USGS figure of 1900 tonnes in 2015. It is interesting and significant to note that the USGS’s reserve figure has remained unchanged since 2009 … which suggests that their current number may now be well out of date.

By way of comparison, MOLAR reports an in-ground gold reserve of 1015.3 tonnes in 2009. So, if you do the math, between 2009 and 2014, according to Chinese Government statistics, China’s proven gold reserve grew by 8801 tonnes. Over the same period the local industry produced around 2300 tonnes. In other words, the Chinese were finding gold ((8801+2300)/2300 =) 4.8x FASTER than they were mining it – which completely contradicts the headline in your article “China’s exhausting its gold reserves …”.

The same flawed data also applies to most of the other selected commodities plotted in the bar chart in article. As a rule of thumb, the USGS reserve numbers are 4-8 x smaller than that reported by MOLAR.

Sorry to rain on your parade – but China is not going to run out of metal any time soon.

MINING.com Editors

Thanks for the comments Richard. Aren’t we back to the old debate about reserves vs resources? Without knowing the methodology used by MOLAR (vs NI 43-101/JORC,Samrec) some of those proven reserves perhaps should be moved into resources. While there is no reason to doubt their stats, as H. commented below the Chinese have found enough deposits, but much of it may not be mineable. This is a moving target of course and with gold clearing $1,300 again today resources become reserves again. Thanks again for opening up this fascinating debate – Frik

Richard Schodde

I agree, the article (and my response) does re-open the debate over EXACTLY what do we mean by “Reserves” & “Resources”. The quoted figures from MOLAR are referred to as “Proven Reserves” … am not sure how well they map onto Western definitions of “Reserves”. Don’t forget though that the USGS’s definition of “Reserves” is fairly broad – and is roughly equivalent to what JORC would define as a “Measured & Indicated Resource”.

A related issue that often confuses and excites the lay-reader is the subtle fact that not all of the Resources will get mined, and the bit that does get mined, not all of the contained metal will be recovered. As really rough rule of thumb perhaps only half of the reported gold resource will end up as gold bars.

And to echo your final point, the published amount of Reserves and Resources will both move up and down with changes in the cut-off grade and the commodity price. Its a moving feast !!

H.

As a Chinese mining engineer worked in a western gold mining company for many year, I can say with confidence that neither the article nor the comments are accurate. China has very unique mineral exploration teams, especially in the gold sector. significant amount of gold deposits have been found in recent years, however, a lot of them are not minable (too deep or under the sea) or not economical with the current gold price.

Altaf

More than the article and the comments, I like the way the discussion is going. The author participating in discussion is a good sign. People reading article along with comments discussion will get more info.

Similar to the largest mining companies discussion.

Thanks Friks 🙂

Sam Bowles

I think Chinese actions regarding currency and gold reserves are directed at one goal: Complete chaos in the mineral and currency markets. There past actions in the rare earth market show how easy it is for them to control it. Also the Chinese have been capitalists for a couple of thousand years. And there are two economies in China: The official, certified by the government one; and the underground hidden market. As far as I can tell, the general consensus about the Chinese official economy: is, who knows what the real figures are.