China is burning through its natural resources

China is the world’s top mining country, but lack of local reserves of main mineral commodities forces local companies to hunt for mining deals globally.

Since nearly all essential production data has became available to the public, this is a good time to determine the biggest mining countries throughout the world in terms of their domestic mines output.

Due to lack of a common methodology, a simple principle of appreciated mining points credited to countries comprising the top 10 was used in this preliminary estimation.

For example, the leader in copper production was awarded 10 points, whereas a country sitting on tenth place earned one point. If a country placed out of the top 10 producers for a particular commodity, it earned zero mining points.

To simplify calculations, no weights reflecting the importance of each commodity, and other modifying factors, were taken into account. Only those most important for the world economy and most popular among investable mineral commodities, have been considered.

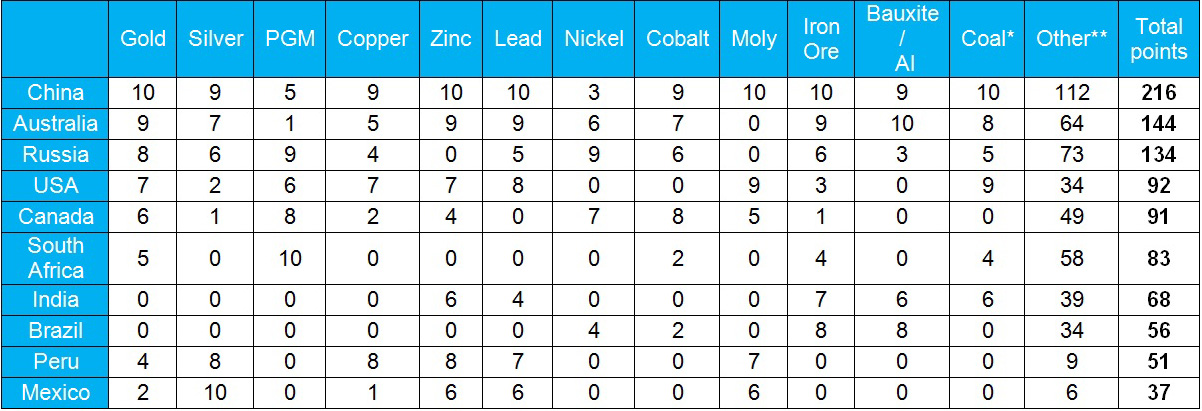

The final outcome of this analysis is shown in the following table:

Countries – leaders in their domestic mine production. Results expressed in mining points

Sources: USGS, BP, market reports, expert opinion.

*Estimation based on 2014 preliminary production figures, except coal and uranium, where 2013 totals used.

** Includes manganese, tin, tungsten, gem diamonds, potash, uranium and other commodities.

China holds first place with 216 mining points, overwhelmingly ahead of Australia, which sits second with 144 points – and 10 points behind third-ranked Russia. The United States and Canada, fourth and fifth in this ranking, are back-to-back with 92 and 91 mining points, respectively.

Of all commodities considered in this research, China is the leader in mining gold, zinc, lead, molybdenum, iron ore, coal, tin, tungsten, rare earths, graphite, vanadium, antimony and phosphate, and holds second place in mine production of copper, silver, cobalt, bauxite/alumina and manganese. The only two main produced commodities of which China is out of the top 10 are gem diamonds and chromium.

This remarkable accomplishment by China’s mining industry raises questions regarding its ability to maintain its leading position longer term, keeping in mind that China’s growing economy remains thirsty for sustainable supplies of raw materials.

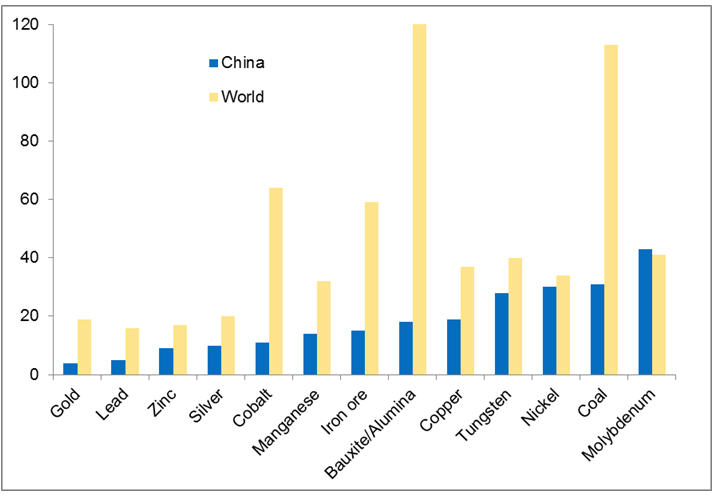

In this case, we have to consider another important indicator, which is the reserves-to-production (R/P) ratio that represents the “burn rate” of proven reserves of mineral commodities in-situ when applying current levels of domestic mine production.

R/P ratio for China in comparison to world average R/P, years

Sources: USGS, BP, country and other reports.

As can be seen, China is in the “red zone” for future supplies of nearly all crucial mineral commodities.

In order to overcome shortages of essential mineral commodities, as well as to secure long-term sustainable supplies for its ambitious economic development strategy, the government of China entitled a number of local state-owned and private companies to actively pursue mining deals throughout the world.

According to the recent Ernst & Young’s report, Chinese buyers topped the list of acquirers by value, with $10.6 billion of deals executed in 2014, including the largest deal of the year, the nearly $7 billion Las Bambas acquisition by MMG.

Undoubtedly, we will see more mining M&A deals led by Chinese corporations, keeping in mind the relentless expansion of China’s economy combined with favorable conditions for assets acquisition due to lower commodity prices.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

3 Comments

Digger Dan

Premier Wynne come clean on the Solid Gold scandal, then resign.

A government swindle and coverup of historical proportion.

Rodrigo Gomez

What happened with Chilean Copper production?

Chance Pemberton

Chinese production of counterfeit coins and bullion must account for much of their basic metals consumption.