CHART: Silver price drops one millstone

The price of silver was trending lower on Wednesday, pushing the metal to below its 2019 opening levels of around $15.30 an ounce.

Silver has been underperforming gold for much longer than even ardent bears had expected – the ratio of the prices of the precious metals recently hit the highest since 1991.

Zinc, lead and copper mines produce more than 60% of the world’s silver as a byproduct and with prices of these base metals also struggling there is little incentive to increase output

The lacklustre trading in silver exists despite a range of positive drivers – the first annual increase in global demand since 2015 to above one billion ounces, a slump in mine production (particularly primary silver producers where output is down 7%), relatively healthy demand from investors in silver-backed ETFs and a rebound in US coin demand.

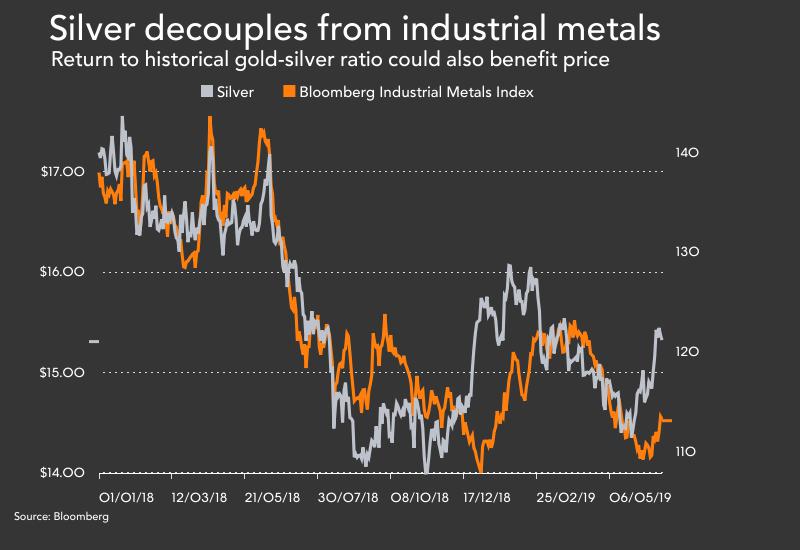

One explanation for the weak silver market is the fact that the bulk of demand is from the industrial sector and the price tracks the performance of base metals closely.

In industry, the outlook is clouded by expectations of slower global economic growth that is affecting major and previously fast growing sources of demand for silver including photovoltaics and automotive applications.

Zinc, lead and copper mines produce more than 60% of the world’s silver as a byproduct and with prices of these base metals also struggling there is little incentive to increase output.

In addition, the world’s third largest silver mine – Escobal in Guatemala owned by Canada’s Pan American Silver – shuttered since 2017 is not likely to reopen before next year.

But a positive trend for silver now seems to be finally developing with the price decoupling from a basket of industrial metals.

This combined with a return of the gold-silver ratio to more historical levels could at last give silver bulls something to look forward to.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments