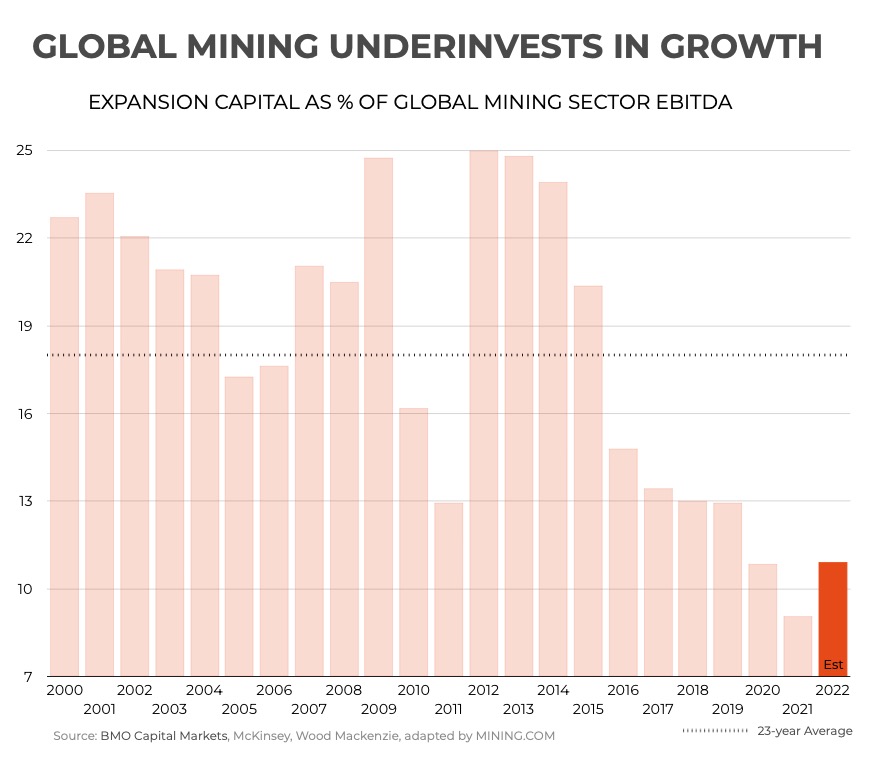

CHART: Demand is soaring, but global mining is not expanding

A new report by BMO Capital Markets has a trenchant chart showing just to what extent mining companies – flush with cash – are opting to return money to shareholders rather than build new mines.

Global mining’s enthusiasm for brown and greenfield projects has fizzled over the last decade despite near universal agreement that in the coming decades demand for metals and minerals will boom due to the green energy transition.

BMO says while companies “have started to talk more openly about investment,” so far they are “doing little about it”.

Over the past 20 years, expansion capital spending across the industry has typically run above 20% of EBITDA, which is to be expected in an industry with depleting assets and falling grades (click here for a copper ore grade graph).

The authors of the report point out that the past couple of years have seen this metric slip to around 10%, “with shareholder returns favoured even as free cash rose.”

“Given the timeline to bring a mine to market, this lack of investment is storing up issues for later in the decade, where balances look incrementally tighter.”

Buying not building

“Moreover, given it has never been harder to build a new mine owing to capex escalation concerns, shareholder resistance and environmental/ESG challenges, we see companies looking towards buying rather than building any growth,” says BMO.

Given this, the investment bank sees the need for medium-to long-term pricing to trade at a premium to the cost curve “given the need to substitute or thrift demand in a number of metals, particularly those exposed to the fuel to materials transition.”

Also in the report, where BMO has upped its price forecast for most of the commodities it covers (notably molybdenum +59%, gold +13%, and copper and zinc both +10%), is a section on changes to China’s raw materials model.

If mining companies in the West are planning to buy their way out of years of underinvestment in new assets, they will have stiff competition, not just at home:

“Ensuring availability of raw material supply is not a new policy for China, but it has clearly been moved up the agenda since last year’s NPC.

“We view this as effectively a carte blanche to Chinese SOEs to invest in mines overseas again, both mining companies and, potentially, battery and automakers such as CATL and BYD.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments