Canada, Australia may have to help America achieve the electrification dream

Canada and Australia could be the top destinations where US president Joe Biden would look for battery metals for his recently announced EV plan, an analysis by Adamas Intelligence suggests.

In late May and following a 100-day review of critical supply chains, Biden said that he plans to look abroad for most supplies of EV metals and focus on domestic processing into battery parts.

Some American miners interpreted the announcement as a blow and commented that the White House should allow more domestic mines, particularly because Chile and Australia – the world’s two largest producers of lithium – ship most of their product to Asia for processing into battery cathodes and other parts and it would be unrealistic to expect those countries to divert existing supply chains to the United States.

Mining analysts, however, pointed out that the US mining industry is unlikely to meet all future demand for battery metals and, in fact, it probably won’t be able to supply more than 30% of the lithium it needs to build EVs domestically by 2030. Adamas Intelligence’s review agrees with this view.

The reason for this is that the US’ climate goals under Biden call for half of all new automobile sales to be electric by 2030 and every car on the road to be electric by 2040.

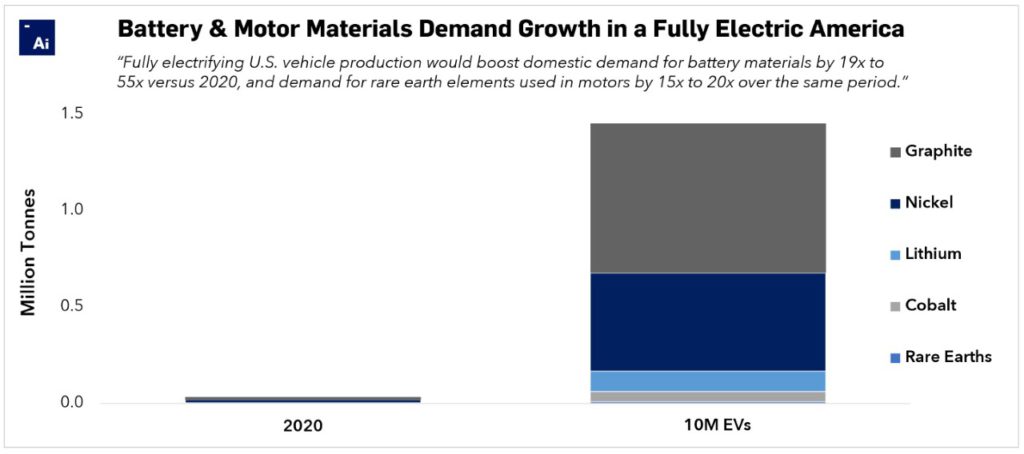

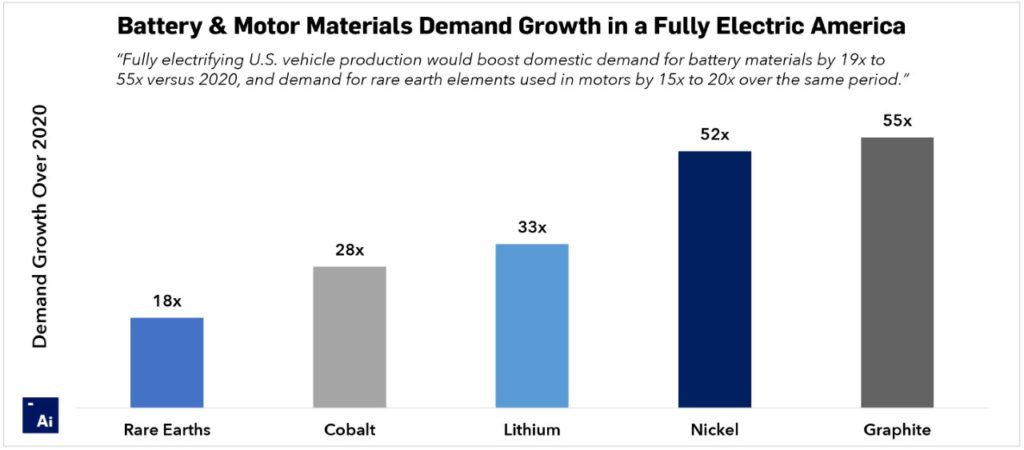

What this means in terms of manufacturing is that about 10 million plug-in electric passenger cars and light trucks would have to be produced every year by 2030, which would foster the country’s battery capacity and motor power demand of 775-gigawatt hours, and 1,500 GW, respectively, each year along with demand for far more raw materials than the US itself could produce.

For Adamas, this is where Canada comes in.

The country is host to around 3% of known nickel reserves globally and produces approximately 15% to 20% of the world’s Class 1 battery-grade nickel each year, while also being the sixth-largest cobalt producer in the world. Both metals are used in energy-dense batteries for high-performance and long-range electric vehicles and Canada extracts them with a degree of transparency and provenance that is becoming more and more important to the end-users.

In other jurisdictions, cobalt and nickel mining may be tainted by issues related to human and labour rights abuses.

“In a fully electric America, it would need more than three times the nickel supply that Canada currently produces and 15 times its current cobalt supply annually,” the analysis reads.

Despite US miners believing it is unlikely that Australia — the world’s top lithium producer, responsible for 50% of the global lithium output every year — would redirect its exports from Asia to America, Adamas predicts that the island country is likely to still benefit from US electrification. Yet, the US demand may be so big that it is likely that Canadian, South American, European and domestic producers will have to fill in the gaps.

Another realm where Adamas Intelligence sees both domestic and ally-country producers benefitting is that of rare earths.

The US is responsible for 10% of global didymium oxide mine supply annually, an input material for high strength magnets used in EV motors. Yet, in the country’s fully electric future, this will not be enough, so Australia, Canada, Europe and others may have to step up and even explore the market of converting rare-earth mine outputs into the high strength magnets because, at present, there is a lack of production capacity outside of China.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments