Battery metals deployment rises as EV sales continue to climb

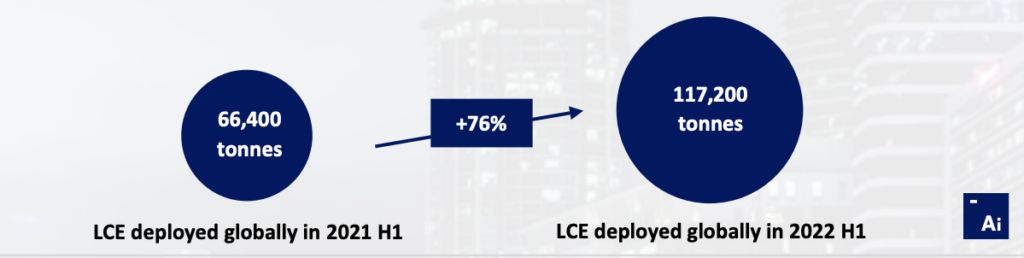

During the first half of 2022, 117,200 tonnes of lithium carbonate equivalent (LCE) were deployed onto roads globally in the batteries of all newly sold passenger EVs combined, an increase of 76% year-over-year.

According to Adamas Intelligence’s biannual State of Charge report, rising sale numbers in battery materials supply chains are the consequence of global passenger EV registrations rising by 42% in 2022 H1 compared to the same period the year prior, amounting to 6.23 million units, up from 4.40 million units in 2021 H1.

The increase was driven by surging sales growth in Asia Pacific, which were up 75% year-over-year, coupled with modest growth in the Americas, which reached 19% year-over-year, and Europe at 10% year-over-year.

Adamas’ report also records a 27% increase in the global sales-weighted average pack capacity, coupled with the pervasive use of LFP and medium- and high-nickel cell chemistries, like NCM 5-, 6- and 8-Series.

The dossier singles out Tesla as responsible for 19% of global LCE deployment in 2022 H1, down from 22% in 2021 H1, with the Tesla Model Y alone responsible for 11% of global LCE deployment.

Battery electric vehicles or BEVs were responsible for 89% of all LCE deployed globally in 2022 H1 versus 87% in 2021 H1, whereas plug-in hybrid electric vehicles or PHEVs and hybrid electric vehicles or HEVs were responsible for a combined 11% in 2022 H1 versus a higher 13% during the same period the year prior.

Nickel deployment

When it comes to nickel, Adamas reports that in 2022 H1, 88,200 tonnes of the metal were deployed onto roads globally in the batteries of all newly sold passenger EVs combined, an increase of 50% over the same period the year prior.

“This increase is attributed mainly to a jump in global EV sales, coupled with the pervasive use of medium- and high-nickel cathode chemistries, plus an increase in global sales-weighted average pack capacity,” the document reads.

“That said, however, with Tesla’s global adoption of LFP cells for entry-level versions, its share of total global nickel deployment fell from 25% in 2021 H1 to 20% in 2022 H1. Notably, the Tesla Model Y alone was responsible for 13% of global nickel deployment onto roads in 2022 H1.”

Adamas’ data show that BEVs were responsible for 82% of all nickel deployed onto roads globally in passenger EV batteries in 2022 H1, a figure that implies a 78% increase compared to 2021 H1, while PHEVs and HEVs were responsible for a combined 18% in 2022 H1, coming from 22% in 2021 H1.

“In 2022 H1, NCM 8-Series cells were responsible for 26% of total global nickel deployment in passenger EV batteries while NCM 5-Series and nickel-rich NCA Gen 3 cells were responsible for 23% and 15%, respectively. Moreover, in 2022 H1, NCM 6-Series cells were responsible for 14% of total global nickel deployment and NCM 7-Series cells were responsible for 10%,” the report states. “Finally, the average amount of nickel deployed onto roads globally per EV sold in 2022 H1 increased by 6% year-over-year, from 13.4 kg in 2021 H1 to 14.1 kg.”

Cobalt deployment

Adamas Intelligence notes that in the first half of the year, 18,500 tonnes of cobalt were deployed onto roads globally in batteries of all newly sold passenger EVs combined, a 44% increase over the amount deployed in the same period the year prior.

As with nickel, this increase is attributed mainly to a surge in global EV sales coupled with the widespread use of medium-nickel cell chemistries, such as NCM 5- and 6-Series, plus an increase in global sales-weighted average pack capacity, from 24.8 kWh to 31.4 kWh.

The market analyst points out that the top seven cell suppliers by cobalt deployed onto roads, namely CATL, LG Energy Solution, Samsung SDI, Panasonic, SK On, CALB and BYD, were collectively responsible for 88% of the market’s consumption.

In terms of vehicle type, EVs were found to be responsible for 81% of all cobalt deployed globally in passenger EV batteries up from 78% in 2021 H1, whereas PHEVs and HEVs were responsible for a combined 19% down from 22% in 2021 H1, as BEV sales growth outpaced that of P/HEVs over the same period.

“As with nickel, the average amount of cobalt deployed onto roads globally per EV sold in 2022 H1 increased by just 2% year-over-year, from 2.9 kg in 2021 H1 to 3.0 kg in 2022 H1, suppressed by ongoing adoption of cobalt devoid LFP cells for entry-level BEV and PHEV models, particularly in China,” the report reads.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments