Battery demand to maintain elevated cobalt prices – report

This year, Fitch Solutions expects a rebound in auto production, coupled with the accelerating EV uptake to keep cobalt prices on an uptrend. These sectors will serve as the primary battery end-market for cobalt chemicals such as cobalt hydroxide, the industry analyst says in its latest report.

Battery metals have risen to the forefront of attention in 2021, as major economies continue to embark on green recoveries from the covid-19 pandemic. Cobalt, in both its metallurgical and chemical forms plays an important role in this increasing transition to greener energy infrastructure and transportation methods, Fitch notes.

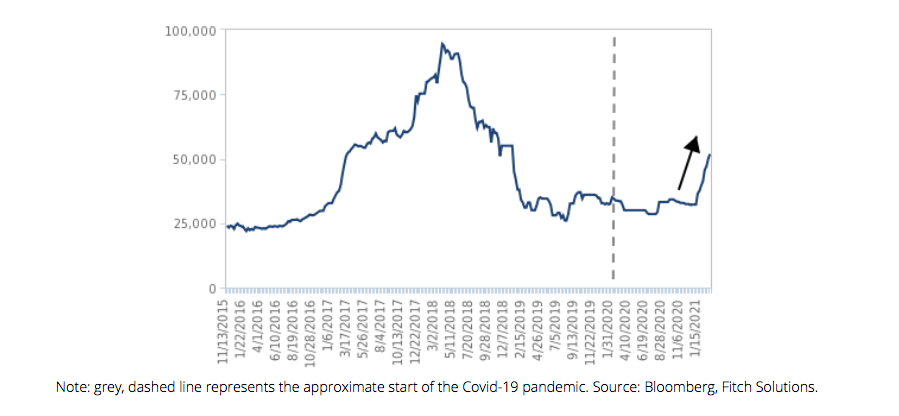

Prices for cobalt remained resilient throughout the uncertainty of 2020, and have trended significantly higher in 2021, with LME cobalt spot prices breaching $50,000/tonne in February 2021 up from $32,209/tonne in December 2020.

LME cobalt three-month

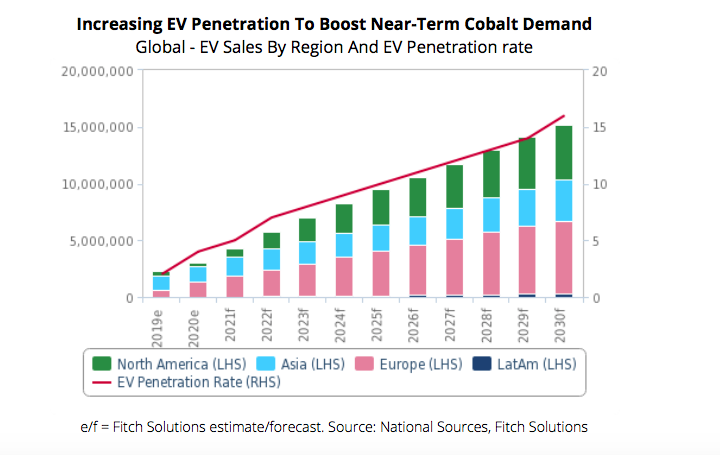

Cobalt demand is driven primarily by batteries, with superalloys in a distant second, Fitch points out. Increased battery demand for autos manufacturing will be accompanied by strengthened demand for cobalt to produce lithium-ion batteries for renewable energy storage and 5G-compatible technology.

Battery storage for renewable energy will be supported by capacity expansions in both solar and wind power, with Fitch’s power analysts forecasting respective global capacities of 807GW and 793GW in 2021. This represents an increase of 43.4% in wind power and 60.4% in solar power capacity since 2018.

Although it will be a smaller end market for now, Fitch says, the pick up in 5G subscriptions will support cobalt demand to manufacture larger lithium-ion batteries. Fitch’s TMT analysts are more bullish on 5G adoption in Asia, led by China’s renewed 5G push. In 2021, the TMT team forecasts China’s 5G subscriptions to experience 123.1% y-o-y growth. Phones running 5G applications require increased power, creating the need for larger batteries to accommodate power amplifiers.

On the supply-side, continued growth in the DRC’s cobalt mining sector will struggle to keep pace with increasing consumption in the coming quarters, Fitch notes. The DRC will continue to dominate mined cobalt production, accounting for approximately 68.0% of mined cobalt in 2020 even amid the covid-19 pandemic.

In 2021, Fitch forecasts cobalt production in the DRC to witness healthy growth of 12.0% y-o-y, aided by ramp-ups and a resumption of work on Chemaf’s Mutoshi processing plant. Supply will also benefit from the increasing formalisation of the artisanal cobalt mining sector, but the continued closure of Glencore’s idled Mutanda mine through 2021 will limit gains, Fitch says.

In the medium term, Fitch expects a lack of transparency surrounding confidential long-term supply contracts will make it difficult to accurately gage supply in the global cobalt market, thus hindering the ability to set prices.

Increasing technological advances pioneering cobalt-free batteries will pose a large threat to cobalt demand and thus prices in the long-term, Fitch says, adding that it expects cobalt to remain a staple in lithium-ion batteries for the next few years, and then increasing charging infrastructure and low-cost efficiency will cause lower-range, cobalt-free alternatives to become the battery of choice.

Read the full report here.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments