Barrick reports strong financials in 2020

Despite the challenges posed by the covid-19 pandemic, Barrick Gold (TSX: ABX) (NYSE: GOLD) reported ending 2020 with one of the industry’s strongest balance sheets.

In its 2020 annual report, the Toronto-based miner first highlighted the fact that it increased its quarterly dividend threefold to 9 cents per share since the announcement of its merger with Randgold Resources in 2018. This means that, in the past two years, the Barrick share price has grown by 118% against a 92% increase in the GDX as of December 31, 2020.

In the document, the company points out that one of the key drivers of the positive figures was its ability to capitalize on higher gold prices, with net earnings adding up to $2,324 million.

“In 2020, gold revenues increased by 27% compared to the prior year, primarily due to the impact of recording a full year of production from Nevada Gold Mines, which was formed on July 1, 2019, and is consolidated and included in revenue at 100%,” the report states. “Excluding the impact of Nevada Gold Mines, gold revenues increased by 12% compared to the prior year resulting from a higher realized gold price, partially offset by lower sales volume. The average market gold price for 2020 was $1,770 per ounce versus $1,393 per ounce in the prior year.”

“In 2020, gold revenuest increased by 27% compared to the prior year, primarily due to the impact of recording a full year of production from Nevada Gold Mines”

The rise in the yellow metal and the $1.5-billion sale of non-core assets such as the Eskay Creek gold-silver project in Canada, were also important for Barrick to register an operating cash flow of $5.4 billion and record free cash flow of $3.4 billion.

This level of free cash flow generation also allowed the giant to move into a net cash position, which represents a decrease of more than $13 billion since 2013 when net debt peaked.

Barrick reports that its adjusted EBITDA margin increased further from 50% in 2019 to 59% in 2020.

“While gold cost of sales per ounce was impacted, importantly, our total cash costs and AISCi per ounce metrics were within the guidance we set at the start of the year, notwithstanding that higher royalty expenses driven by a higher gold price were a significant cost headwind,” the company’s CFO, Graham Shuttleworth, said in the report.

According to Shuttleworth, Barrick now has less than $100 million of public debt maturities falling due before 2033, and an undrawn credit facility of $3 billion. This strong cash flow is the reason behind the quarterly dividend increase.

When it comes to copper, the Canadian firm registered a 77% increase in revenues in 2020 compared to the prior year. This rise was due to higher copper sales volume and a higher realized copper price.

Tier-one assets delivered strong production

In terms of production, Barrick reached 4.8 million ounces of gold and 457 million pounds of copper in 2020, numbers that fit its guidance of 4.6 to 5 million ounces of gold and 440 to 500 million pounds of copper.

“Our focus on tier-one and other strategic assets has unlocked material synergies and opportunities,” Mark Bristow, the firm’s president and CEO, said in the report. “The Barrick-led establishment of the Nevada Gold Mines joint venture created the world’s largest gold mining complex under our operatorship and added a sixth tier one mine to our portfolio in the form of the combined Turquoise Ridge and Twin Creeks operation.”

Bristow also emphasized the importance of having reached a deal to settle a long-running tax dispute between Tanzania and mining group Acacia, which Barrick bought in a $1.2-billion transaction in 2019. This settlement – he said – has led to the construction of a potential tier-one complex in the East African country.

“We [also] established Lumwana as a profitable long-life copper mine in Zambia and in Canada, we are well on our way to transforming the previously precarious Hemlo into a robust tier two operation,” the executive said.

When it comes to cost guidance, Barrick reported that 2020’s cost of sales applicable to gold was $1,056 per ounce, slightly higher than its guidance range of $980 to $1,030 per ounce, mainly due to higher royalty expense resulting from the impact of a higher realized gold price and higher depreciation expense following an impairment reversal recorded in the first quarter of 2020.

Gold total cash costs and all-in sustaining costs for 2020 were $699 and $967 per ounce, respectively, both within the guidance ranges of $650 to $700 and $920 to $970 per ounce, respectively.

Barrick’s copper business, on the other hand, registered a cost of sales of $2.02 per pound, below its guidance range of $2.10 to $2.40 per pound, mainly due to lower depreciation.

Copper all-in sustaining costs were $2.23 per pound, at the lower end of the company’s guidance range of $2.20 to $2.50 per pound.

The future

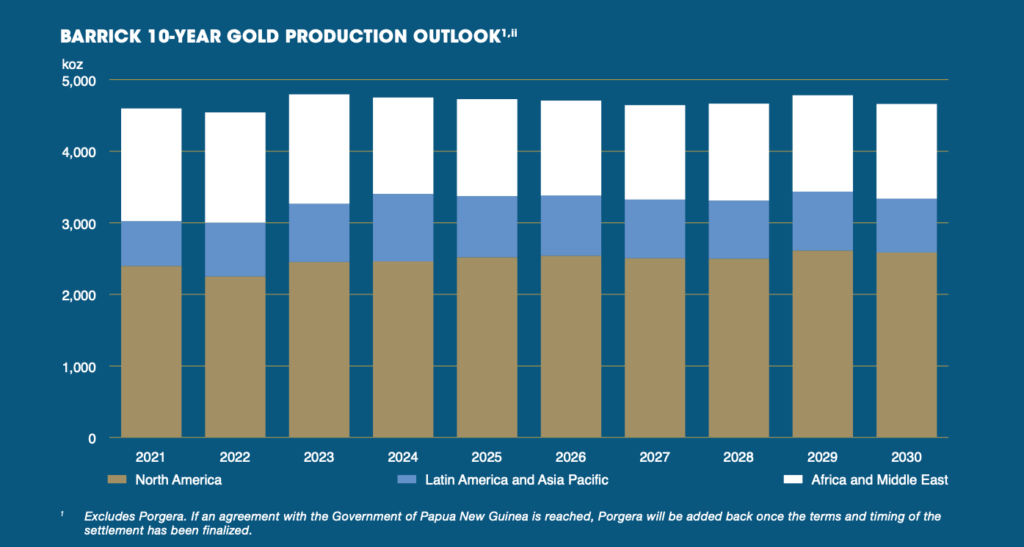

Production guidance for 2021 is expected to be in the range of 4.4 to 4.7 million ounces, excluding production from the Porgera mine, whose operations have been suspended since April 2020, after the Papua New Guinea government didn’t extend Barrick’s mining lease in demand for a bigger stake in the asset.

This guidance, thus, is based on the miner’s properties in North America and the Africa & Middle East regions.

“Five of our six tier-one gold assets are located across these two regions, highlighting the importance of a world-class asset base in delivering consistent performance with the potential for significant brownfields expansion and new discoveries,” the annual review states.

Barrick expects gold production in the second half of 2021 to be slightly higher than in the first half, pushed by the commissioning of the Phase 6 leach pad at the Veladero operation in Argentina, mine sequencing at Nevada Gold Mines and the ramp-up of underground mining and processing operations at Bulyanhulu in Tanzania.

In terms of resources, the company said that as of December 31, 2020, it has proven and probable gold reserves of 68 million ounces at an average grade of 1.66g/t Au. Measured and indicated resources were estimated at 160 million ounces at an average grade of 1.52g/t Au.

Barrick owns and operates six tier-one gold mines, namely, Cortez, Carlin and Turquoise Ridge in Nevada; Loulo-Gounkoto in Mali, Kibali in the Democratic Republic of Congo and Pueblo Viejo in the Dominican Republic.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Silvanus ilonga

All over the world world mining sector is a bone of back by economical because his bring lots of revenue and bring most great jobs opportunity!