Analyst downplays Galane Gold’s June profits, company responds

While Africa-focused Galane Gold (TSX-GG) announced that it bounced back to profitability in the second quarter of 2016, thanks to an increase in production at its Mupane mine in Botswana, an industry analyst warns that the news really means “trouble in paradise.”

In a detailed report published late August on Hallgarten & Company’s website, analyst Christopher Ecclestone calls Galane’s profit for the June quarter “tiny.” He goes on to add: “The profit of a mere $99,000 on revenues of $9.34mn in a fairly strong gold price scenario represents a net margin of around 1%. Nothing to write home about.”

Galane Gold, an unhedged gold producer and explorer, recently acquired Galaxy Gold in South Africa. The firm’s board, which approved the re-opening of the mine in July, has vowed to spend an initial US$2 million to get it up and running so that it can restart production by the end of the year.

Despite the positive news, Hallgarten’s analyst says Galane’s shareholders have reasons to be concerned. He lays out the company’s liabilities to back his claims:

Ecclestone states that Galane’s acquisition of Galaxy Gold in South Africa is nothing less than a bad deal, given that:

- The mine turned out to be a dud for previous owners.

- The company had to issue unsecured debentures “to certain Galaxy loan holders and other parties” as settlement of amounts previously due for Galaxy.

- Galane also inherited shareholder loan agreements from Galaxy in South African Rand.

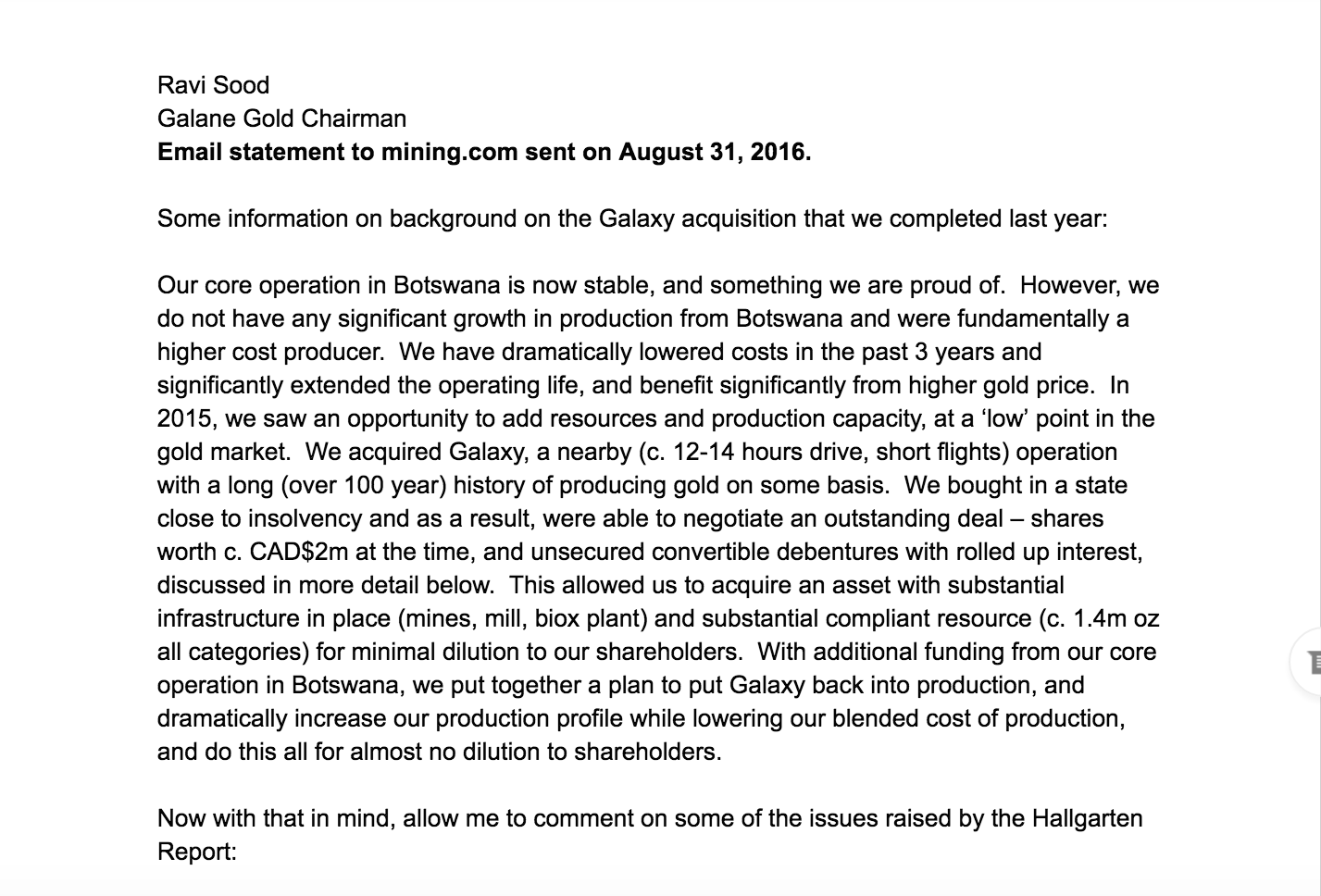

But the company had some things to say about Ecclestone’s document: “The report fails to highlight our cash-flow from operations of $1.978m from Q2 alone. The income and margin number referenced is an accounting number which also includes re-start costs at Galaxy, depreciation and amortization, and other non-cash items. Investors should focus primarily on cash generation and what is done with the cash – not accounting results,” Galane’s Chairman Ravi Sood wrote in an email statement.

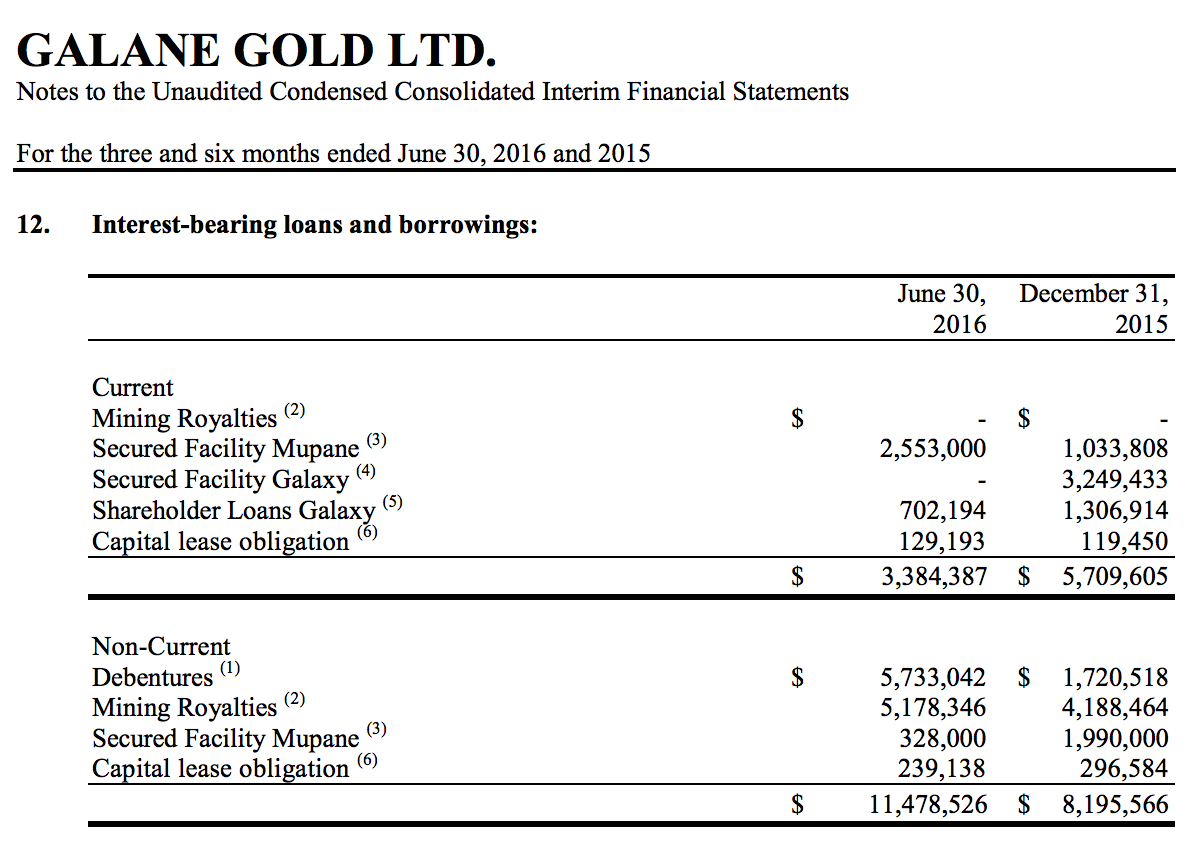

He went on to explain that the largest component of Galane’s debt is the unsecured, subordinated, 4% interest convertible debentures due to the former Galaxy debt-holders, but he said that there is no cash burden associated with these because “the interest rolls up and is payable in November, 2019.” Sood also said that the company’s forecasts show that they can service this debt out of cash-flow by that time.

Ecclestone’s report also indicates that Galane Gold’s deal with Samsung, where the latter put forward cash to ensure supplies of gold for its operations, should be a cause for concern. After their loan facility and gold prepayment agreement was renegotiated in 2015, GG’s Mupane mine must deliver at least 1,607 ounces of gold at a price for the gold “selected by Samsung from any one of the four London Bulletin AM or PM dollar gold fixing prices falling either on the delivery date or on the day immediately following the Delivery Date, less a discount of 1.25%,” reads the company’s Condensed Consolidated Interim Financial Statements for the three and six month periods ended June 30, 2016.

In exchange, Samsung agreed to a repayment of 12 instalments of $20,000 per month effective from October 2015, followed by nine instalments of $277,000 and a final instalment of $328,000 in July 2017. “This arrangement kept the wolf from Galane’s door for an extra year but the paying of the piper will begin soon as the $20,000 per month being repaid shall shortly (in just over a month) balloon to $277,000 per month, consuming most of its cash flow,” Hallgarten & Company’s analyst says.

At the same time, Ecclestone complains about Galane’s lack of explanation as to how it is going to fund these debt repayments and honour creditors who are secured against the Mupane asset.

Sood explained that after a rough two-year period of depressed gold prices prior to the Galaxy acquisition, the company is now entering a phase where they can start generating cash-flow from operations, fund capital requirements at Galaxy and service debt repayments. During those difficult times, the Chairman said, “stakeholders were highly constructive (Samsung and the Government of Botswana) and we structured deals that preserved shareholder value and allowed us to keep them whole, and service those obligations when gold price was higher and we had better operating results. Mission accomplished.”

Ravi Sood assured that Galane’s capital structure is near-on ideal at this stage in the cycle and the state of its operations. “We have expanding production, declining costs, and a rising gold price. Having financial leverage, particularly leverage that does not have any short-term servicing cost of any sort (rolled up interest, bullet payment in 2019), is absolutely ideal for common shareholders. It gives us leverage to the upside on our operations, and gold itself,” he pointed out.

Galane Gold Chairman’s full statement [click on the image for the full statement]:

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments