Barrick says Ontario Superior Court dismisses 2022 Tanzanian security case

A group of 21 Tanzanian nationals had alleged that Barrick was complicit in extrajudicial killings by police guarding its North Mara mine.

In conjuring this title, I realized it has been a mere five weeks since I wrote about the acceleration of Ely Gold Royalties into junior royalty space (Mercenary Musing, June 17, 2019).

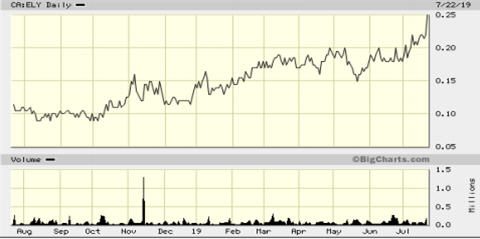

In the interim, the stock has continued a steady climb upwards from C$0.18 and hit an intraday high of C$0.255 today.

So I started thinking … and wondering … and asking.

ELY underwent a market re-rating from October to late February with a double in market capitalization as it transitioned from a Nevada prospect generator to a hybrid company with gold royalty interests.

In late April and early May, it was at a 2.5-year high at C$0.205 and then pulled back a bit to C$0.18 a month ago.

By then, the various royalty and property deals it announced had closed or were on the verge of doing such.

Meanwhile, the price of gold soared from its yearly low of $1,272 in late May to $1,445 late last week before falling back to the $1,425 level. That’s a 12% move in less than two months.

Another catalyst for ELY’s recent rise is closing of the sale of a small royalty interest in Quebec and a strategic private placement with Toronto speculator Eric Sprott.

The one-year chart is below. In my opinion, it is quite constructive with higher highs and higher lows since October.

Market capitalization is now at C$25 million dollars; that’s more than triple what it was when I initiated coverage in late February 2018.

The company’s transformation over the past 1.5 years has been both successful and impressive:

The company is now drawing comparisons to junior royalty peers that have market caps six to seven times higher.

Based on precedent, Ely management makes the case that it is entering a sweet spot for junior royalty companies whereby market capitalizations leap-frog over the course of a couple of years. Examples they point to include Sandstorm Gold, Metalla Royalty, and Abitibi Royalties.

If this suggestion proves correct, subscribers who got in early and took well-earned profits might want to redeploy some capital into ELY before the next move up.

Likewise if you are new to the story or did not act on my initial idea last year, this could prove to be a good entry point in the low 20 cent range.

Regardless, more royalty deals and property options are likely in the works and therefore, we are aiming for another re-rating of Ely Gold Royalties that could produce a double within the next 12 months.

I am looking to add more of my own capital into this company but I do not intend to chase the stock. Although it gapped up today, my target price remains in the low 20s. Note that my views are skewed by speculative dollars in Ely Gold Royalties and the fee it pays to sponsor my website.

All in all, a near-term re-rating seems a reasonable possibility; check out the new corporate presentation and see what you think.

On another note, ELY will exhibit at the Sprott Resource Investment Conference in Vancouver, July 30 to August 2, and I will be making two public speaking appearances. As per usual, there will be many interview opportunities and chats with high net worth speculators about resource companies that have recently caught my attention.

(By Mickey Fulp)

Comments