CHARTS: The coming critical minerals trade war is BRICS short of a load

"While a large number of countries around the world continue to talk about securing raw material supply, China is actually doing something about it."

Base metals have had a shaky start to 2019, with a cautious first-quarter advance giving way to an April drop on uncertainty about the global economy and the impact Chinese stimulus will have on consumption.

Clouding the outlook are mixed signals on world growth. China’s first official gauge of the manufacturing sector fell in April, indicating that more may be needed to bed down the economic stabilization seen earlier this year. The euro area’s manufacturing slump showed tentative improvement, while data showed U.S. unemployment fell to a fresh 49-year low. Hanging over the market, though, is the question of when the U.S. and China will resolve their prolonged trade spat.

Growth prospects, as well as supply outlooks for the most-traded base metals, will be among topics discussed as traders, executives and financiers gather in Hong Kong for the annual LME Week Asia event. Here’s a summary of key discussion points:

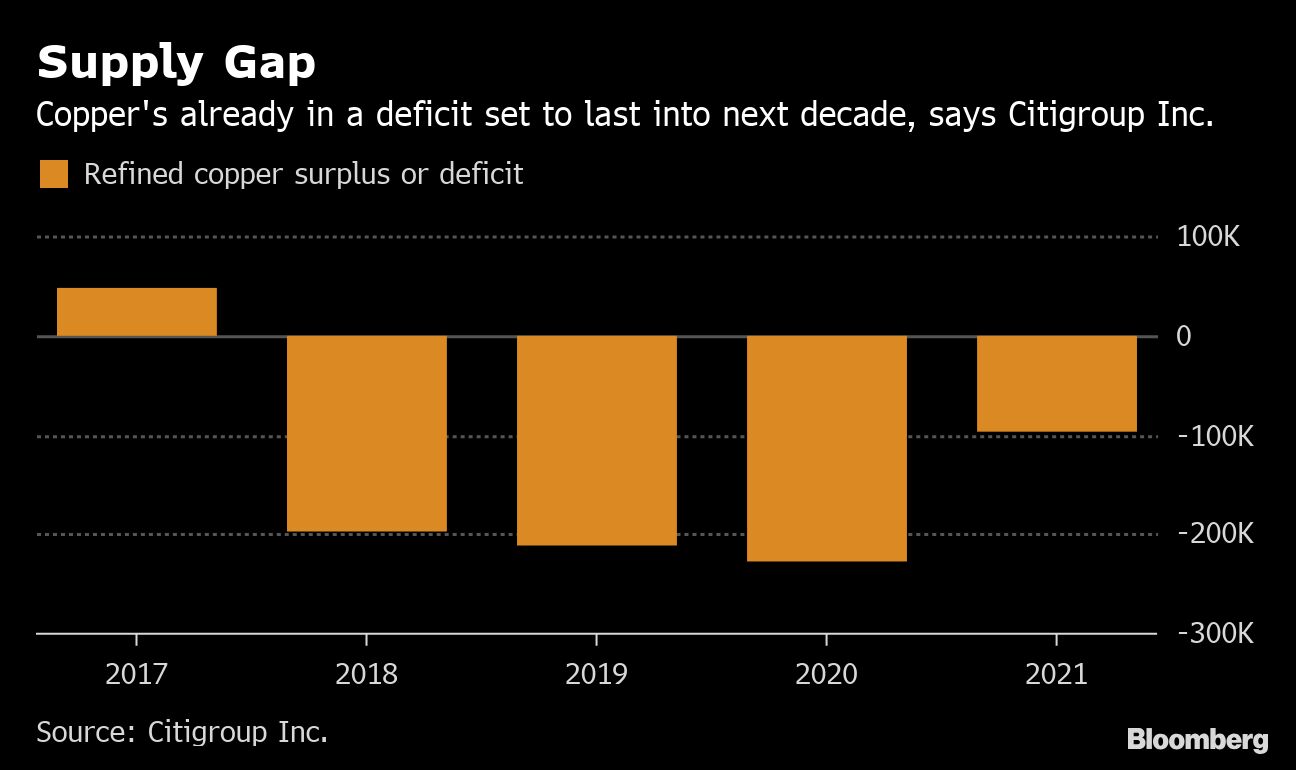

Copper’s long-term appeal is a staple topic at LME gatherings (see here, here, and here). But the metal has failed to break out of a modest range since its slump in mid-2018, even as global mine supply tightens. Prices are often tied to the global macro mood, which has been soured by U.S.-China trade tensions and muted manufacturing activity.

In China, government stimulus has proved underwhelming so far, according to one of the nation’s top traders. Import premiums are waning and a high-profile trader’s financial woes are also weighing on sentiment. Barclays Plc predicts prices may end the year below $6,000 a ton, saying the macro backdrop still matters more than any supply issues. Still, copper bulls may take heart after Codelco said the downtrend in prices won’t last as consumption growth outstrips supply.

The key question in the market is whether China’s zinc smelters can process increasing global mine supply. Output constraints in the top producer — due to various disruptions and environmental strictures — have crimped their ability to do so. With treatment charges still at elevated levels, there’s growing expectations of a supply response from smelters that will pressure global prices. But not everyone is convinced.

“The economics of zinc are already telling smelters to produce as much as they can, and I don’t think that’s happening,” Colin Hamilton, managing director for commodities at BMO Capital Markets Ltd. said in a phone interview. “The question is, are we going to see them ramp up? If not, the zinc market has a problem because refined inventory is still very low”.

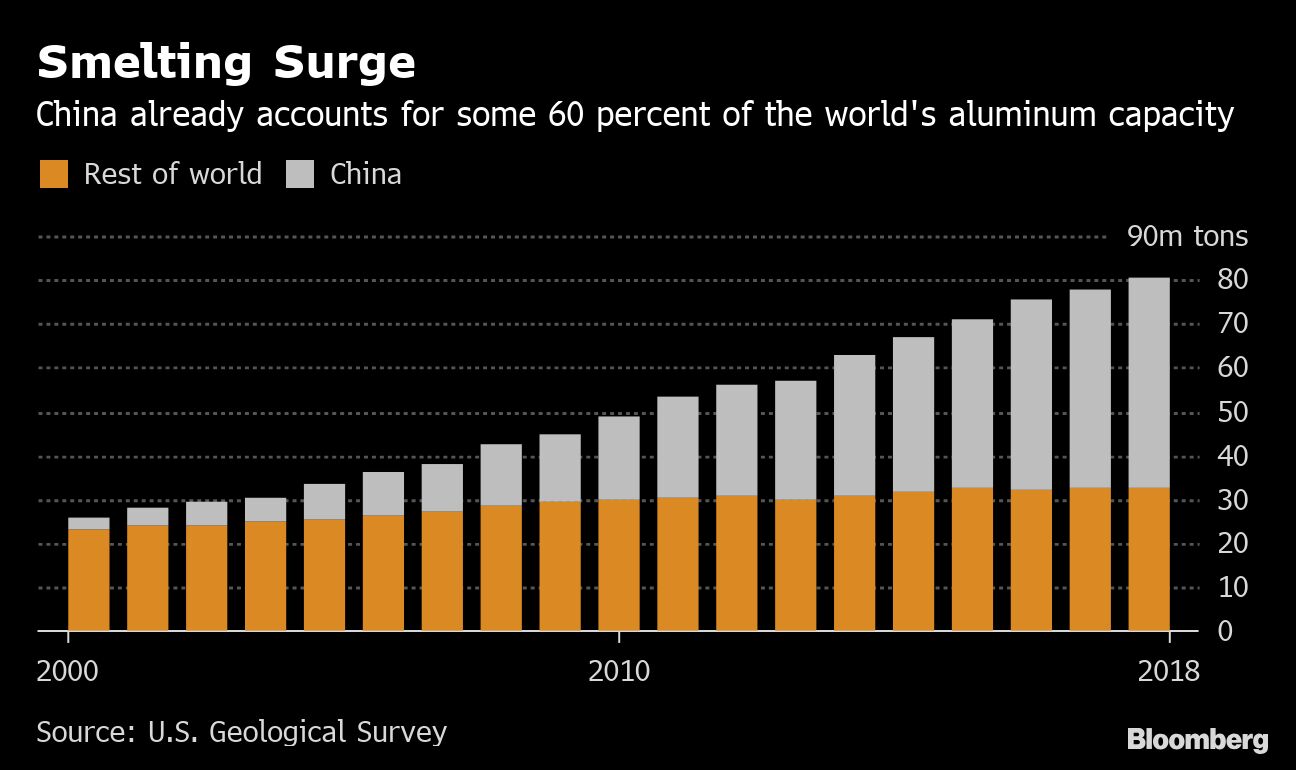

Last year was turbulent, with the market dominated by the prospect of U.S. sanctions on United Co. Rusal. With that episode resolved, attention has turned to more familiar concerns, especially Chinese capacity. Prices in London are broadly in line with where they started the year, constrained by weakness in demand and uncertainties around new Chinese plants.

Aluminum optimists point to dwindling stockpiles in China, greater restraint in permitting new capacity, as well as rising consumption. But some producers aren’t feeling so upbeat. China’s recent better-performing prices — crucial to setting the global tone — are “ unsustainable” given substantial capacity still waiting in the wings, Rusal warned in April.

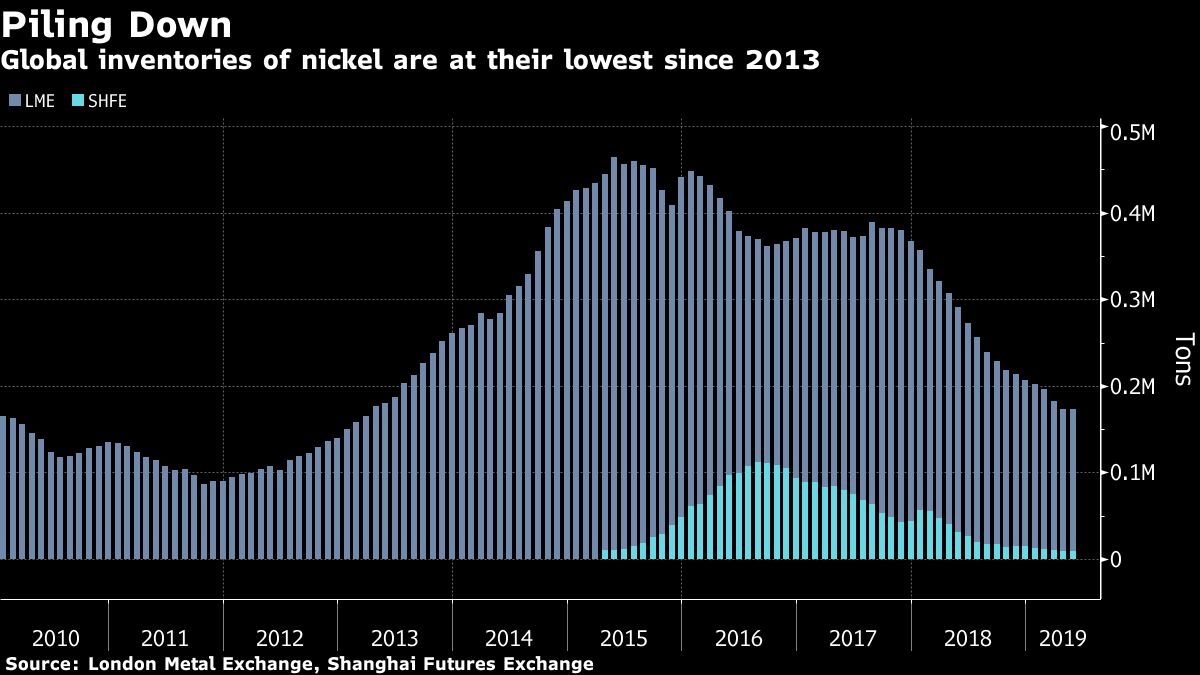

Nickel is this year’s best-performing base metal, and dwindling global stockpiles point to a tighter market. But there’s plenty of room for short-term caution. China’s output of nickel pig iron is running at its highest levels since 2014, while Indonesia is also boosting supply. There’s signs of weakness in the crucial stainless steel sector, with stockpiles building in China as prices soften.

Much still hinges on the fate of major Chinese investments in low-cost battery nickel production in Indonesia. Timely progress toward operating low-cost battery nickel plants in the country could reboot some of the concerns that triggered a drop in prices last year. Citigroup Inc. is forecasting higher nickel prices this year, it said in April as part of its expectations for a more risk-on global environment in the second half, “rather than nickel’s micro factors.”