Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

The world’s gold miners have spent years avoiding each others’ gazes like nervous teenagers. Now all of a sudden they’re acting like the thrill has gone.

It hasn’t even been two months since Barrick Gold Corp. and Randgold Resources Ltd. announced that their merger was “consummated,” and already Executive Chairman John Thornton appears to be checking out an old flame.

Like most odd couples, they complement each other: Barrick’s mines tend to be higher-grade, but the less debt-ridden Newmont produces more consistent returns

Barrick has in recent months been studying a takeover bid for Newmont Mining Corp., possibly in combination with Newcrest Mining Ltd., people familiar with the matter told Ed Hammond, Danielle Bochove, Aaron Kirchfeld and Ruth David of Bloomberg News Friday.

It’s not clear if the deal is still under consideration, the people said. Newmont announced its own tie-up with Goldcorp Inc. last month, which you’d have expected to change the calculus somewhat. Still, a report in the Globe & Mail newspaper citing industry sources familiar with the situation suggested Barrick and Newcrest might be ready to jilt Goldcorp at the altar, carving up Newmont’s assets between themselves and leaving Barrick to pay a $650 million break fee for violating the target companies’ prenup.

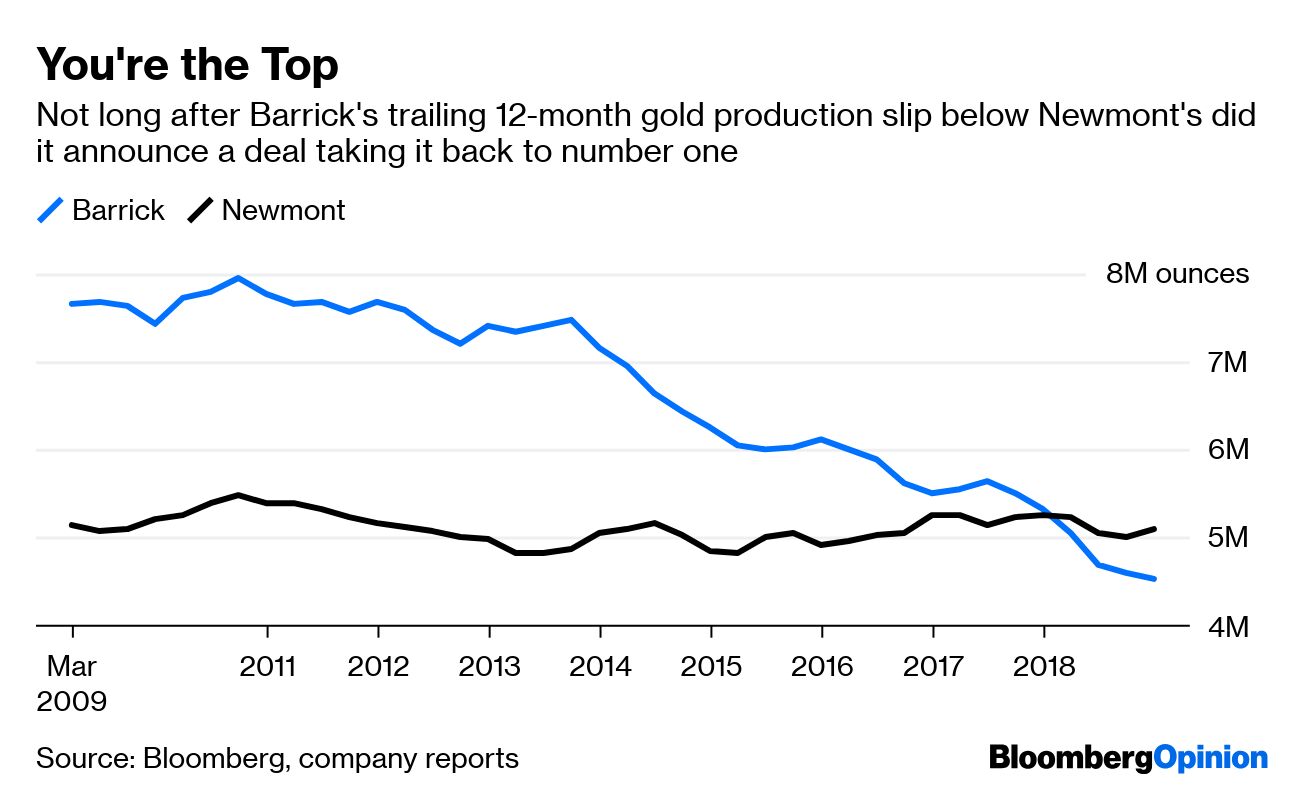

Newmont and Barrick have quite a history together. The two largest gold miners have held merger talks every decade or so for almost thirty years, with the last courtship breaking down as recently as 2014. Like most odd couples, they complement each other: Barrick’s mines tend to be higher-grade, but the less debt-ridden Newmont produces more consistent returns and has normally been preferred by investors.

Barrick has historically been the biggest producer of the pair. It tells you everything you need to know about their relationship that within 12 months of Newmont pulling ahead in output terms, Barrick announced its Randgold deal to get back in pole position.

With an on-again, off-again history that rivals Ross and Rachel, it’s tempting to wish Barrick and Newmont would just get a room and end the speculation.

At the same time, the rush for alliances at the big end of town risks teaching the wrong lessons from the latest round of dealmaking. The great virtue of the new Barrick is that Chief Executive Officer Mark Bristow has a laser-like focus on improving returns and investing in new supply.

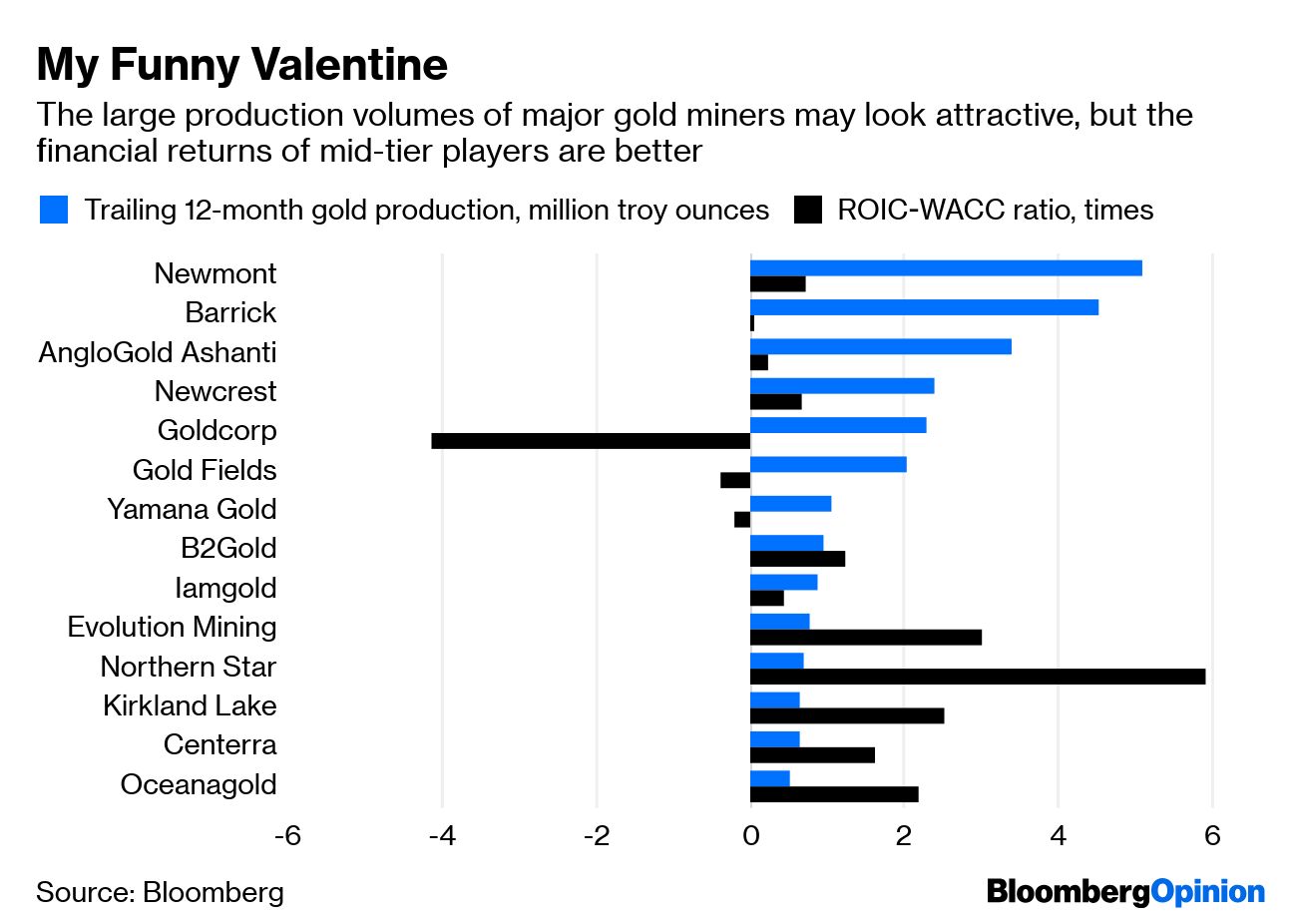

That would suggest concentrating simply on the increased volume available from a deal with Newmont isn’t the best way to go. To be sure, there may be ways to combine Newmont and Barrick’s assets that would result in worthwhile synergies – but just below the radar there’s a host of mid-tier gold miners producing better returns and finding more value than the biggest players.

Canada’s B2Gold Corp., Kirkland Lake Gold Ltd., Centerra Gold Inc. and OceanaGold Corp. plus Australia’s Evolution Mining Ltd. and Northern Star Resources Ltd. all fail to clear the one-million-troy-ounces-a-year bar that seems to be the minimum to pique the top companies’ interest. Unlike their larger rivals, though, they’re all producing returns well ahead of their cost of capital, which ought to count for something.

For the moment, these members of the gold mining community seem so intent on hooking up that neither is noticing how attractive these wallflowers could be. That’s a mistake. A big, splashy prom is all very well, but a lasting relationship is based on the fundamentals.

(By David Fickling)