Korea Zinc plans 10-for-1 stock split

Rival Young Poong and private equity firm MBK Partners have been trying to take over the world's biggest zinc refiner.

* Market braces for rise in output from Asia

* Nickel outperforms other base metals in 2019

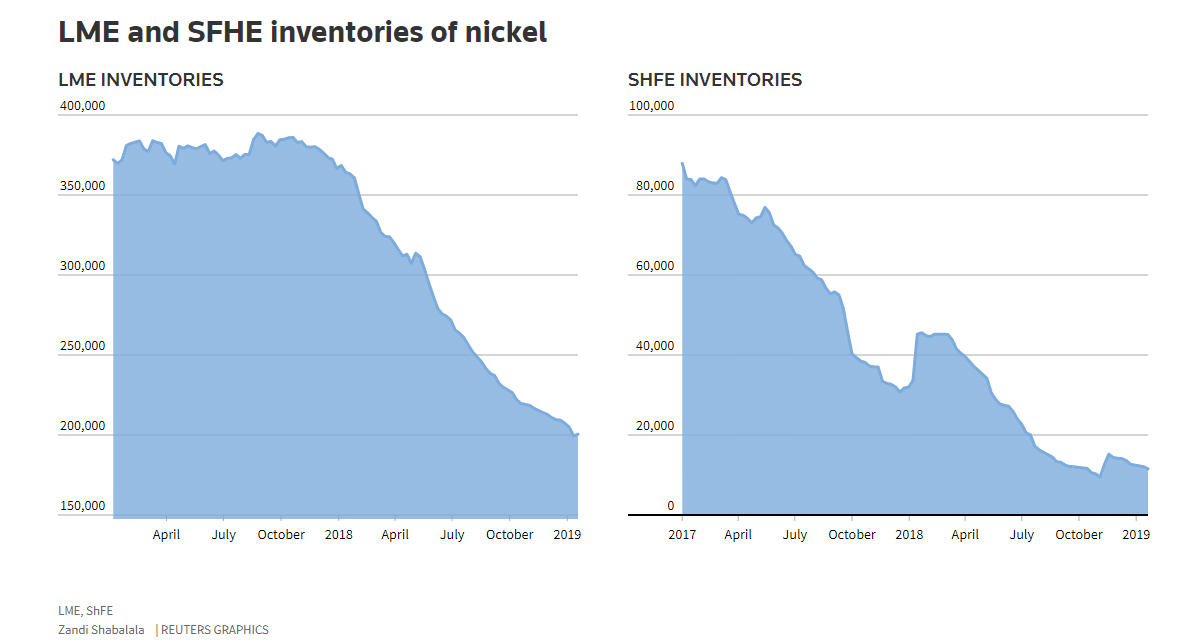

* Inventories slip: https://tmsnrt.rs/2RZbZB0

Soaring nickel output in China and Indonesia to record levels this year is expected to weigh on prices for the metal used to make stainless steel and batteries for electric vehicles even if some projects are delayed.

Nickel on the London Metal Exchange (LME) is up 15 percent so far this year to a three-month high of $12,325 per tonne due to falling stocks and concerns that Brazil’s Vale could cut some of its production.

BMO Capital Markets expects mine output from Indonesia, the world’s largest nickel producer, to rise 34 percent this year

“Current price moves are a knee jerk reaction to the Vale news,” said BMO Capital Markets analyst Kash Kamal.

However, rising output from lower-grade nickel pig iron (NPI) producers and high-pressure acid lead (HPAL) facilities mainly in top producers China and Indonesia are likely to drag prices down.

Analysts at Wood Mackenzie expect smelter expansion in the two Asian countries will result in a 12 percent rise in NPI production to a record 840,000 tonnes this year.

“The announced level of new supply from (HPAL) is so great that near-term deficits and the rationale for progressively higher nickel prices is now at risk,” Wood Mackenzie said.

BMO Capital Markets expects mine output from Indonesia, the world’s largest nickel producer, to rise 34 percent this year to around 777,000 tonnes of contained nickel, rising to 850,000 tonnes in 2020.

Producers such as China’s Tsingshan Group, PT Virtue Dragon Nickel and Shandong Xinhai Technology plan expansions.

However, analysts have cast doubts on the timely completion of a 50,000-tonne HPAL project in Indonesia by Tsingshan and its partners scheduled to begin production this year.

Global nickel demand this year is estimated at around 2.4 million tonnes.

BMO Capital Markets sees a deficit of 129,000 tonnes which is expected to narrow to 96,000 tonnes in 2019.

But Citi analysts see a balanced market this year after a deficit of 40,000 tonnes last year.

Citi analyst Oliver Nugent said changes in the discount for the cash over the three-month contract “do not chime with market consensus of a wider deficit”.

Suggesting ample supply, the discount now at $66 a tonne recently narrowed to $9 a tonne as the market worried about falling stocks in LME registered warehouses.

LME stocks have fallen 45 percent since the beginning of last year to 202,032 tonnes while inventories in ShFE warehouses are at their lowest since October at 11,357 tonnes.

The ongoing trade dispute between the United States and China has also hit prices of nickel as Chinese stainless steel mills are major consumers.

In addition, nickel’s bull rally partly based on electric vehicle excitement is premature, analysts say, with stainless steel still accounting for about two-thirds of demand.

Stainless steel production rose 10 percent in the first nine months of 2018 but showed signs of slowing growth in the third quarter, the International Stainless Steel Forum said.

“Nickel is still very stainless led and it’s a macro story,” Citi’s Nugent said. “Nickel will have its heyday but maybe this isn’t the year.”

(By Zandi Shabalala; Editing by Pratima Desai and David Evans)