Solaris exits Canada for Switzerland with new CEO, board and spin-out plans

The company changed its board of directors and plans to spin out non-core assets La Verde, Capricho, and Paco Orco into a new company.

A new year but the same old problems for aluminium.

“When you look at the economics of producing aluminium, these prices cannot be sustainable.”

That was the stark message from Roy Harvey, president and chief executive of U.S. aluminium producer Alcoa, speaking on the company’s Q4 2018 results call.

With the London Metal Exchange (LME) aluminium price languishing near two-year lows at a current $1,870 per tonne, Alcoa estimates some 30 to 40 percent of the world’s smelters are losing money.

Alcoa’s own aluminium smelting operations recorded a net operating loss of $53 million in the fourth quarter of 2018. It is in the process of closing two Spanish plants, another rejig of its smelter portfolio aimed at being “competitive through all cycles”.

The current pricing reality jars with Alcoa’s assessment that the global aluminium market will record a second year of supply shortfall to the tune of 1.7-2.1 million tonnes in 2019.

If the world is running an accumulating deficit of the stuff, how come smelter margins are being pulverised?

The answer comes in two parts.

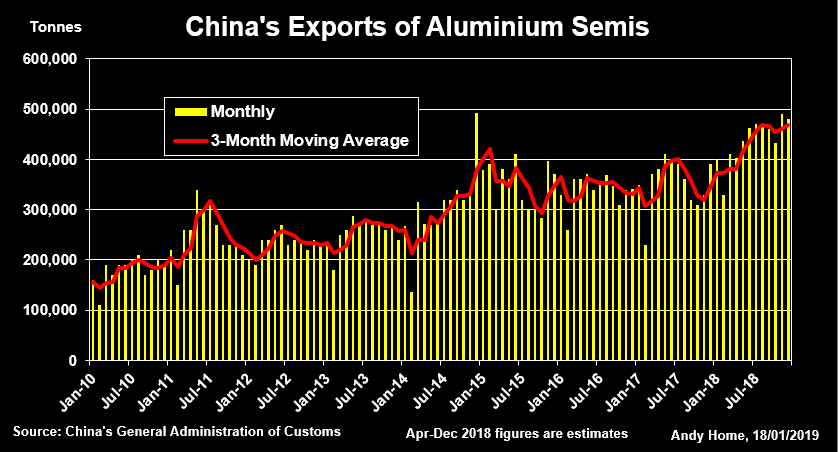

Graphic on China’s exports of aluminium “semis”:

Firstly, Chinese exports of aluminium in semi-fabricated product (“semis”) form surged to fresh heights last year.

Total exports of unwrought aluminium, including primary metal, alloy and semis, were 5.8 million tonnes last year, up 21 percent on 2017.

That’s a lot of metal, equivalent to around 20 percent of demand in the rest of the world, according to Alcoa’s Harvey.

Most of the exports, something around 5.25 million tonnes, were in “semis” form.

This massive outbound flow injects complexity into any calculation of market balance in the primary metal segment of the supply chain.

Strong Chinese semis production means strong Chinese primary metal consumption, but strong Chinese exports of semis means a hard-to-quantify displacement of metal demand elsewhere.

Such statistical niceties aside, however, the real significance of China’s accelerating exports is what they say about what’s happening in China.

China’s production of primary aluminium was up by one percent in the first 11 months of 2018, a sharp slowdown from 2017, when output grew by 10 percent.

Quite evidently, higher exports are not down to surging output, but rather poor demand.

Quite evidently, higher exports are not down to surging output, but rather poor demand.

Analysts at BMO Capital Markets estimate that Chinese aluminium demand growth last year was anaemic by historical standards at just 1.1 percent.

The deceleration was in stark contrast to strong consumption of both steel and copper, up nine and four percent respectively. (“Steel the positive surprise in China’s Metals Demand”, Jan. 16, 2019).

BMO pinpoints three bear drivers that have combined to depress aluminium usage in China – low levels of State Grid power transmission investment, a fall in construction completions and a weak automotive sector.

Given that China has long been the engine of global aluminium usage growth, last year’s tepid performance dragged global usage growth down to 2.6 percent, the slowest since the Financial Crisis, according to BMO. (“Aluminium: Can a record deficit really feel this bad?”, Jan. 8, 2019).

Even allowing for this below-trend usage rate, BMO still calculates the global market was in “record market deficit” last year with inventory draws of around 1.5 million tonnes to plug the supply gap.

And inventories are the second reason why the supply deficit isn’t doing much to lift prices.

There is still a lot of aluminium around, some of it dating back to the demand collapse of the Global Financial Crisis.

Total inventory is falling and at 50 days’ global consumption is back at 2008 levels, according to BMO.

“This is, however, still high in historical terms,” BMO wrote, adding, “there is no inventory shortage for aluminium.”

“There is no inventory shortage for aluminium”

Moreover, any bullish signal from falling stocks is lost in the statistical murk of off-market storage.

Visible stocks such as those registered with the London Metal Exchange have fallen steadily over the last few years but the driver has not been fundamentals but rather cost of exchange relative to off-market warehousing.

LME stocks look set to fluctuate around the one-million-tonne level with movements both in and out determined primarily by gyrations in short-dated time spreads.

The longer-term bull story of falling stocks is playing out in the shadows. And it will continue to do so.

The only clue as to what is happening comes in the form of physical premiums.

Unfortunately for producers such as Alcoa, these are as bombed out as the LME price.

Japanese buyers have just negotiated first-quarter shipment premiums of $85 per tonne over the LME, the lowest settlement in two years.

Broader macro-economic concerns have of course weighed on the aluminium price, just as they have on all the LME-traded metals, but aluminium’s particular problem right now is the weakness in demand in the world’s largest user.

Any offsetting potentially bullish narrative of falling inventories is simply not visible to the market.

The best that can be said is that prices are unlikely to stay at these levels for too long.

“The price as it is right now certainly doesn’t sustain continued production”, according to Alcoa’s Harvey.

“The price as it is right now certainly doesn’t sustain continued production”

That applies particularly in China itself where price-related curtailments have started to build.

Chinese demand, meanwhile, should pick up this year, according to BMO.

In the construction sector completions are set to grow as strong starts feed through the development process.

Having not approved any aluminium-intensive high-voltage transmission projects since 2014, Chinese policy-makers sanctioned 12 new ones at the end of last year.

The automotive sector, meanwhile, is unlikely to be as weak as it was last year, particularly as broader Chinese stimulus trickles through to consumers.

The combination of improved usage and constrained production growth in China, where Beijing has capped future smelter capacity growth through a permitting system, should translate into lower exports of semis.

How long this takes is difficult to say, given the multiple complexities of Chinese economic stimulus and simultaneous reform of the aluminium sector.

Equally unknowable is when total stocks will be drawn down to a point that requires higher pricing.

Things will get better. Eventually.

For now it’s back to cost-curve support.

“Given we are already hard into the cost structure of the industry the risk-reward skew is to higher prices than seen currently,” is BMO’s conclusion.

Alcoa would agree.

Prices will in all likelihood move higher. How much higher, however, is an altogether different question.

(By Andy Home; Editing by David Evans)