Column: Trump 2.0 won’t reverse Biden’s critical minerals push

Donald Trump has described the Inflation Reduction Act (IRA) as a "green scam" and vowed to repeal it after he returns to the White House in January.

COMEX copper stocks rose by a net 271 tonnes on Monday. There was some light two-way action at New Orleans and arrivals at both Tucson and Salt Lake City.

So what, you might ask.

Who cares how much copper is sitting in the small handful of U.S. locations registered as good delivery points for what is now the CME’s high-grade copper contract?

COMEX stocks are the third, often forgotten component of the global copper inventory picture.

For years the copper market narrative has been woven around the interaction between inventory registered with the London Metal Exchange (LME) and the Shanghai Futures Exchange (ShFE).

You could even argue that Shanghai bonded warehouse stocks, although statistically obscure, attract more attention than the stuff sitting in what is a purely domestic US delivery system.

But that may be about to change.

Because Monday’s increase in COMEX stocks was but the latest small step higher in a bigger trend that has been running since November last year.

COMEX stocks <HG-STX-COMEX> currently total 180,121 tonnes. That’s the highest they’ve been since 2004, when the U.S. economy was still recovering from the bursting of the dot.com bubble.

Even during the dark days of the global manufacturing meltdown that followed the financial crisis of 2008, they topped out at a little over 105,000 tonnes.

But equivalent to 163,405 tonnes, COMEX stocks now eclipse the 113,600 tonnes of “live” warrants registered with the LME. If they carry on rising like this, they may soon represent the largest single component of the global exchange stocks picture.

How did that happen? And what does it mean for the copper price?

THE TRUMP EFFECT…?

COMEX stocks have nearly tripled in size since the start of November 2016, when they totalled just 71,961 tonnes.

The timing is significant.

It was in November last year that Donald Trump unexpectedly won the U.S. elections. And with Trump came the possibility of a U.S. border tax on commodities such as refined copper.

The arbitrage between LME and COMEX copper prices responded accordingly, flexing out to multi-year levels.

Things have calmed down a bit since then as the prospect of President Trump delivering on this particular campaign pledge has receded.

In March this year the COMEX contract for December 2018 was trading at a 2 percent premium to the equivalent LME contract. That differential has nearly halved in the interim.

But the arbitrage gap, on a forward basis at least, is still there and is still widely believed to be the primary reason behind the rise in U.S. copper stocks.

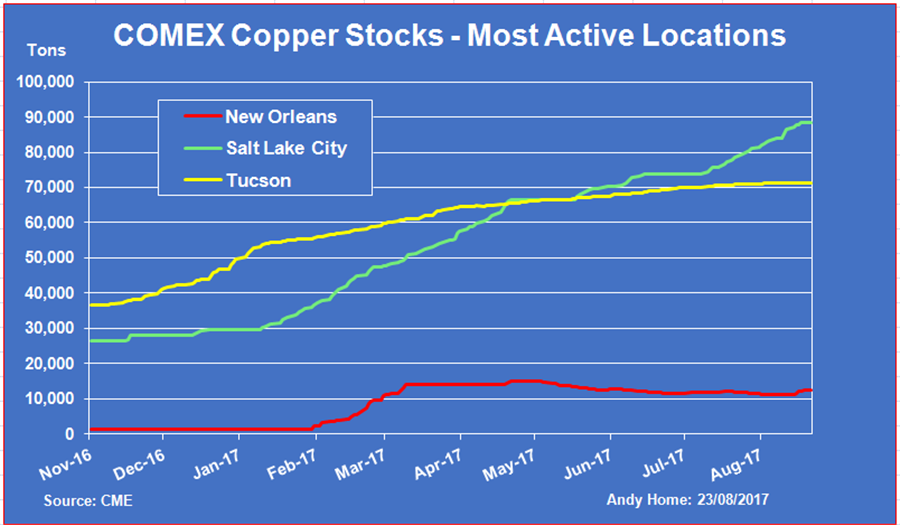

Graphic on COMEX copper stocks and active locations:

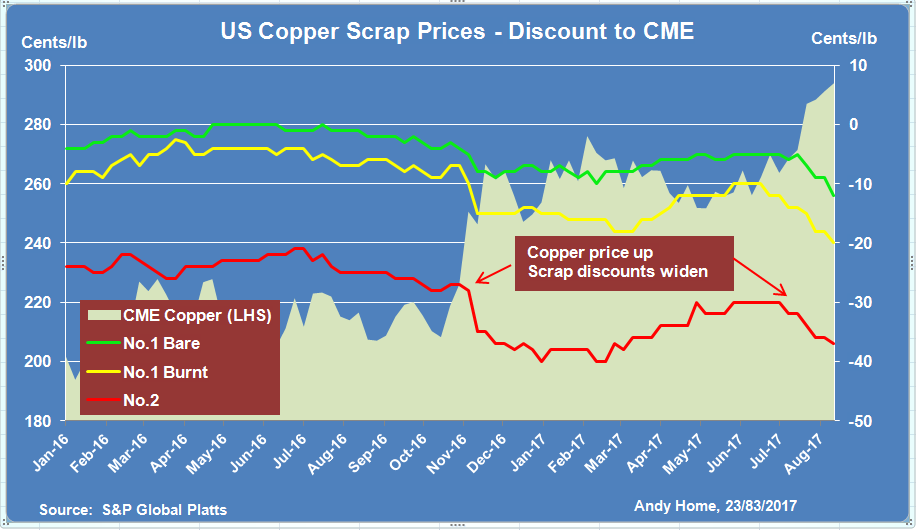

Graphic on US copper scrap pricing:

…OR THE SCRAP EFFECT?

The only problem with that explanation is the location of the stock increases.

COMEX has just seven delivery points, only five of which hold any copper at all and only three of which have been recently active.

And only one of those, New Orleans, is a physical arbitrage point. Not only is it a major international transit port but the city is also host to LME warehouses, albeit sitting in duty-free zones.

If the Trump Effect has stimulated physical flows from international market to U.S. domestic market, New Orleans is where you’d expect to see the impact.

There was a noticeable rise in New Orleans stocks in the first quarter of this year. But the inflow has since fizzled out and the port has, on a net basis, accounted for only 11,091 tonnes of the overall 108,160-tonne increase since November.

Rather, most of the inflows have taken place at Tucson in Arizona, where stocks have risen by 34,820 tonnes, and Salt Lake City in Utah, where they are up by 62,313 tonnes.

Both are not only land-locked but also bereft of any LME warehouses, suggesting that arbitrage, even by displacement, is not the only reason for higher COMEX stocks.

Another displacement effect may be at work in what appears to be a chronically over-supplied regional market, namely copper scrap.

The sharp price rally of late 2016 generated a surge in scrap availability this year, including in the United States.

U.S. discounts for all types of copper scrap blew wider as higher prices incentivised dealers to release material that had been loss-making at lower prices.

The price of higher-grade “bare bright” scrap, for example, flexed out from flat with CME copper in June 2016 to a 10-cent per lb discount in February 2017, according to S&P Global Platts.

Just when the scrap pricing structure appeared to be normalising, this month’s sharp rise in copper prices has caused renewed widening in discounts.

The Platts-assessed discount for “bare bright” had narrowed to just five cents in June. As of last week it was back out at 12 cents, suggesting another potential scrap surge is on its way.

ACCEPTED WISDOM

This seemingly inexorable rise in COMEX stocks is a bear signal in an increasingly bullish global copper market.

The Trump arbitrage effect doesn’t completely explain either the geography or scale of the increases. What is a U.S. physical delivery system must also be saying something about the broader state of the U.S. copper market.

But rising COMEX inventory poses questions not just about the copper price but the way copper is priced, in particular the relationship between CME and LME copper markets.

The accepted market wisdom is that the latter is where the heavy-weight industrial and financial players do their business, leaving the smaller, speculative activity to the CME.

But the recent sharp jumps in both trading and open interest on the U.S. contract, coupled with declining volumes on the LME, have started to chip away at this collective tenet.

Throw rising inventory into that mix and things start to look even more interesting.

One impact of rising stocks on the CME contract has been a widening of the forward contango structure relative to the LME.

It’s not quite reached a point where stocks financiers will pounce but it’s a lot closer than the LME structure. That creates the potential for the sort of “industrial” activity that characterises the London market to cross the Atlantic.

It may seem an unlikely outcome but, for now, keep an eye on those COMEX stocks. They’re getting more relevant to both copper price and copper pricing by the day.

By Andy Home

(Editing by Susan Thomas)