Earth AI, Legacy Minerals make first greenfield palladium discovery using artificial intelligence

The companies announced the verified discovery of one of the largest palladium mineral systems in Australia.

There are several encouraging signs for the mining outlook in Australia.

Prices

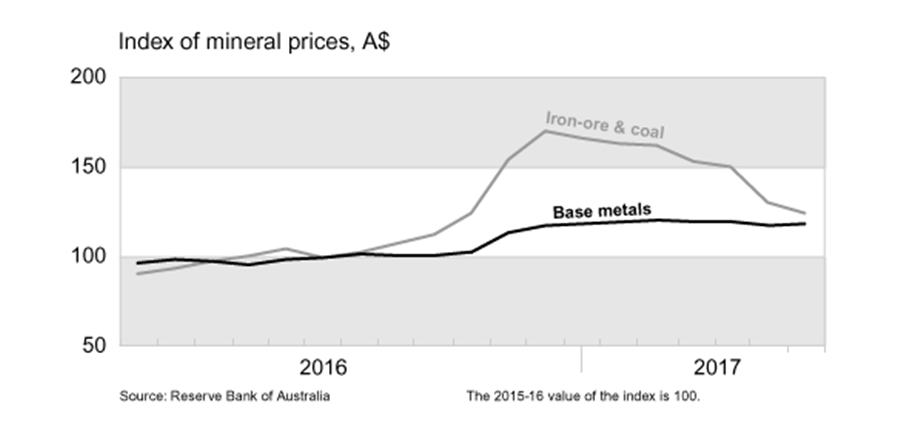

First, mineral prices are showing signs of life.

Prices of base metals (copper, nickel, zinc, aluminium, lead) have steadily increased over the past nine months. In addition, prices of iron-ore and coal are well ahead of their levels a year ago. (They have come down from the peak of late 2016/early 2017, when prices of both increased strongly, defying widespread forecasts.)

Production

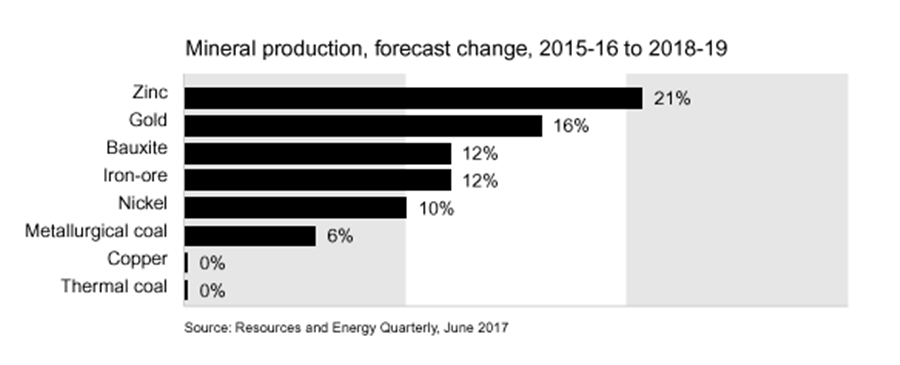

Second, whatever happens to prices, mineral production in Australia is likely to increase over the next few years. This follows the enormous investment made in new mining projects in the decade after 2005; many of these projects are now producing mines. The forecasts shown below come from the Australian government’s industry department, through its publication, Resources and Energy Quarterly.

Projects

Third, planning for tomorrow’s new mines appears to be stepping up.

For example, iron-ore companies are planning major new developments in the Pilbara region of Western Australia. These include Koodaideri ($2 billion+) in the case of Rio Tinto and South Flank in the case of BHP Billiton ($2 billion+).

Gold-mining companies, notably in Western Australia are generally in an expansive mood, with current prices resulting in attractive margins for many existing operations.

Since last year, production has commenced at three lithium mines in Western Australia: Mount Cattlin, Mount Marion and Wodgina. In addition, construction is underway at the Pilgangoora lithium project, with first production expected by March next year.

Lithium is not the only mineral being stimulated by the strong demand for lithium-ion batteries (notably for electric vehicles and large-scale electricity storage). BHP Billiton announced this month that it is to develop the world’s largest nickel-sulphate plant near Perth, nickel being an important component of lithium-ion batteries.

BHP Billiton also announced this month that it will spend $600 million this year at its Olympic Dam copper-gold-uranium-silver mine in South Australia, notably on underground infrastructure and an upgrade of the smelter there.

South Australia will also benefit from OZ Minerals’ underground Carrapateena copper-gold project; with an estimated cost of $1 billion, first production is expected in late 2019.

Coal has been buffeted in recent years, with prices slumping for several years up to late 2016 and most coal-expansion plans being shelved.

However, this situation is changing.

The Indian company, Adani Group, appears set to start early works this year on its large Carmichael mine in Queensland, following years spent meeting government approvals and overcoming environmental objections to the project. The $15-20 billion project will include a 390-kilometre rail line to new port facilities at Abbot Point (between Mackay and Townsville).

The thermal coal produced (eventual annual capacity will be 60 million tonnes) will be mainly sold to India for electricity production.

Glencore Australia and Yancoal Australia are both intent on expanding coal production in Australia, while several smaller new players (e.g. Pembroke Resources, MACH Energy) are planning new mines in this sector.

Mining-service companies are starting to feel the benefits of this improving picture, both in regard to orders and enquiries.