Earth AI, Legacy Minerals make first greenfield palladium discovery using artificial intelligence

Companies announced the verified discovery of one of the largest palladium mineral systems in Australia.

(The opinions expressed here are those of the author, a columnist for Reuters.)

By Clyde Russell

LAUNCESTON, Australia, June 22 (Reuters) – Iron ore’s demand-driven price surge last year is increasingly looking like an aberration as supply factors once again start to weaken the price outlook.

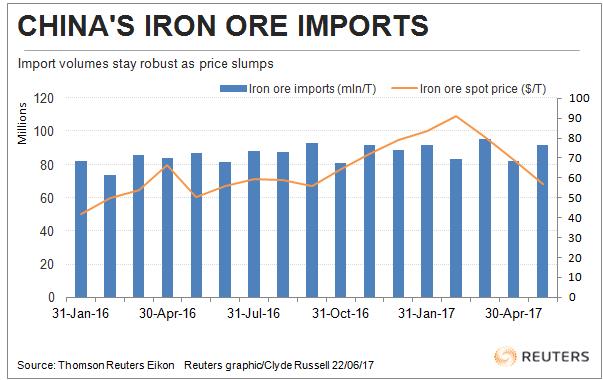

When spot Asian iron ore prices jumped 81 percent in 2016, the surprise rally was chalked up to stronger Chinese imports and signs that a market that had been oversupplied for several years was back in balance.

China, which buys about two-thirds of seaborne iron ore, certainly did boost imports in 2016, buying more than 1 billion tonnes in a year for the first time, with overseas purchases of the steel-making ingredient rising 7.5 percent.

There has been little let up in the pace this year, with imports from January to May jumping 7.9 percent from the same period in 2016 to 444.6 million tonnes, putting them on track for an annual increase of about 65 million tonnes.

Imports look set to remain robust in June as well, with ship and port data compiled by Thomson Reuters Supply Chain and Commodity Forecasts pointing to arrivals of 93 million tonnes.

This number was filtered to show only vessels that have already discharged cargoes or are underway, and may be revised higher as late cargoes get added.

Overall, the picture shows that China’s appetite for imported iron ore remains strong, meaning the price decline so far this year isn’t driven by weakening demand.

The spot price ended at $56.82 a tonne on Wednesday, down 28 percent from the start of the year and 40 percent from a peak of $94.86 on Feb. 21.

Chinese domestic iron ore futures have fared some better, with Dalian Commodity Exchange contracts slipping 8.1 percent so far this year to Wednesday’s close of 426 yuan ($62.37) a tonne, and down 33 percent from their Feb. 21 peak.

STEEL, IRON ORE TREAD DIFFERENT PATHS

In contrast, benchmark Chinese steel futures, the Shanghai rebar contract, have gained 15.1 percent since the end of last year to Wednesday’s close of 3,060 yuan a tonne.

This divergence between Chinese steel and iron ore prices is a marked change from last year, when they rallied in tandem, with rebar gaining 96 percent to spot iron ore’s 81 percent.

China’s steel market appears relatively robust currently, with output in May rising 1.8 percent from a year earlier to 72.26 million tonnes, just below April’s monthly record of 72.78 million tonnes.

In the first five months of 2017, production was 346.8 million tonnes, up 4.4 percent from the same period last year, according to official figures.

Higher steel output is a response to solid margins for steelmakers, which are being supported by ongoing capacity cuts and a still reasonable outlook for construction and manufacturing.

It’s mainly low-quality furnaces that are being targeted for closure by Chinese authorities as part of plans to shut at least 50 million tonnes of capacity this year, which follows on from 65 million tonnes idled last year.

Assuming the demand outlook for steel doesn’t deteriorate too much in the second half of the year, the capacity closures should help keep steel mills profitable and support prices.

But for iron ore the arrival of additional tonnes on the seaborne market from expansion projects by Brazil’s Vale and the new Roy Hill mine in Western Australia will keep the market’s focus on supply.

Citi analysts said in a report received this week that the seaborne market could be oversupplied by 100 million tonnes in 2017, leading them to cut their average price forecast for this year to $61 a tonne from $70 previously.

Once again, it appears that the iron ore market is going to play the game of who can survive lower prices the longest.

While low-cost major miners such as Vale and Anglo-Australian pair Rio Tinto and BHP Billiton are best-placed, smaller Australian players and producers in minor exporters like Ukraine and Canada will struggle to hold on.