Gold price ahead of the Thanksgiving weekend

During this period, gold is usually just before forming a short-term top and starting the biggest decline within the final quarter of the year.

Kootenay Silver Inc. (TSXV: KTN) began phase II leach testing of oxide and sulphide silver mineralization on bulk samples from the La Cigarra silver deposit using SILVOX process.

AuRico Metals Inc. (TSX: AMI) receives environmental assessment approval for Kemess underground project.

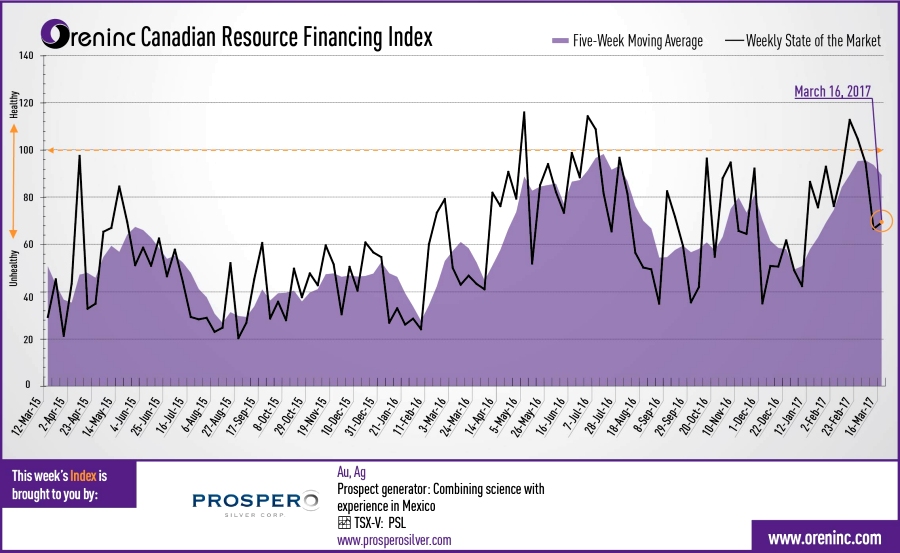

Last week index score: 65.62

This week: 69.20

The Oreninc Index increased in the week ending March 16, 2017 to 69.20 following the previous week’s strong retrenchment to 65.62 as gold consolidated above the US$1,200 per ounce level to close the week at US$1,228.

Gold, silver and copper increased mid-week after the US Federal Reserve announced a 0.25% increase in interest rates. Market analysts say that this increase was expected and already priced into the market, and the fact that the press conference comments by Federal Reserve Chair Janet Yellen were dovish, provided a sell-the-rumour, buy-the-fact trading action. Whilst the Federal Reserve is expected to continue raising rates throughout 2017 and 2018 market observers believe that rate increases will now happen at a slower pace than previously thought.

The period following the PDAC (Prospectors and Developers Association Conference) in Toronto in early March has traditionally corresponded to the shutting of the first significant financing window of the year, with deals dropping off after the conference, known as the PDAC curse. Evidence of this was present this week as the number of financings fell to 27, a nine-week low, even though the total dollars increased to C$128.9m, a two-week high and the average offer size doubled to C$4.7m, a two-week high. This latter figures were skewed however by a financing by oil company Painted Pony. Of the 27 financings announced, there were two brokered financings for C$102.8m, a four-week high, and one bought-deal financing for C$98.8m, a seven-week high. The PDAC curse of reduced financings usually recovers in April.

With gold having a stronger week, the industry’s leading benchmark index, the van Eck GDXJ saw growth resume and is now up 14.99% so far in 2017, as did the inventory of the SPDR GLD ETF which increased from 825.22 tonnes a week ago to 834.1 tonnes this week.

With strikes continuing at some of the world’s largest copper mines the copper price strengthened slightly to close at US$2.69 per compound compared to US$2.60 per pound a week ago. With management and the union at Escondida no closer to negotiation than when the strike started over a month ago, management is considering a lock-out and closure of its installations.

WTI crude remained under US$50 after falling below that psychological level last week for the first time since December 2016.

The Dow Jones Industrial Average continued above the 20,000 mark and consolidated at 20,914 after closing the previous week at 20,902. In Canada, the S&P/TSX Composite Index also had a week of consolidation although trending down on the previous weeks’ 15,506 to close at 15,490. In the junior space, the S&P/TSX Venture Composite Index closed up on the week at 810.59 from 799.19 the previous week. This index hit a year high of 844.96 on 21st February.

This past week, Oreninc published its latest podcast with The Mercenary Geologist Mickey Fulp recorded at the PDAC, to get his observations on the event, which is available on www.oreninc.com.

Financial news highlights

Trevali Mining (TSX: TV) entered into an agreement with BMO Capital Markets for a bought deal private placement of C$230 million. The proceeds will be used to pay for the purchase of a portfolio of zinc assets from Glencore for an aggregate purchase price of US$400 million. Traveli also expects to fund a portion of the cash consideration through a new senior secured credit facility of US$190 million.

K92 Mining (TSX-V:KNT) arranged a non-brokered private placement to raise up to C$10.0 million to raise funds for grade control, expansion and exploration drilling, work on the underground incline drive at its Kora deposit of its Kainantu project in Papua New Guinea. K92 began an underground drive at Kora in early March that is a a continuation of the Irumafimpa incline drive. Kora is a high-grade gold deposit with a resource estimate of 4.36 million tonnes grading 7.3 g/t Au, 35 g/t Ag & 2.23% Cu. K92 is targetting first production from Kora oin 1H18.

Summary:

Major Financing Openings:

Major Financing Closings:

Company news

Kootenay Silver Inc. (TSXV: KTN) C$0.28, Mkt Cap C$48.9 million

Kootenay Silver is an exploration company with projects in the Sierra Madre region of Mexico and in British Columbia, Canada. Its leading properties are the La Cigarra silver project and the Promontorio Mineral Belt, in Chihuahua, Mexico and Sonora, Mexico. The Promontorio mineral belt includes the La Negra high-grade silver discovery and its Promontorio silver resource that is under option to Pan American Silver.

Conclusion:

If phase II leach testing of oxide and sulphide silver mineralization is successful, Kootenay will have a strong handle on a key cost component as it looks to prepare a preliminary economic assessment for La Cigarra going forward in addition to be able to factor in higher silver recoveries.

AuRico Metals Inc. (TSX: AMI) C$1.13, Mkt Cap C$178.6 million

Conclusion:

The main permitting hurdle to Kemess is now overcome giving the company a line-of-sight on being able to complete the paperwork and be in a position to make a construction decision.