Mining’s old guard needs strong medicine

A new report details subpar investor returns in the mining industry over the last decade, particularly big cap diversified companies which have not adapted to new realities.

Now that we have two weeks of the New Year under our belts, we wanted to take a look back at 2016 and extend a hearty thank you to all our Sprott clients and Sprott’s Thoughts readers. Natural resource investing is never a dull affair, and 2016 was certainly no exception. Without a doubt 2017 will provide a new set of opportunities and challenges, and we are encouraged by a return of outside capital and interest to our space. Below we highlighted some of the major events impacting our industry in 2016, the lessons we’ve learned, and our expectations for 2017.

1H 2016

For commodities, 2016 was a tale of two halves. The first six months of the year were marked by an astonishing uptick in spot prices that reignited investor interest and brought capital back into the system. Gold in particular led the way, up nearly 20% in six months. Oil prices climbed 25% from $39 per barrel at the end of March to nearly $50 per barrel. Agricultural commodities, such as soybean meal, sugar, corn and cotton, posted gains for the second quarter. Lumber finished the first half of 2016 up nearly 18% for the year. Base and precious metals expanded upon first quarter gains to advance their rebound from 2015’s doldrums[i].

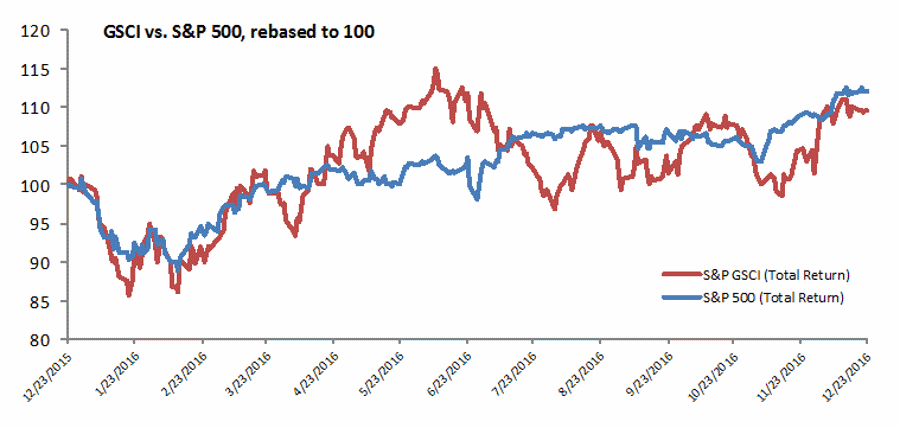

Altogether, commodities far outpaced the rest of the U.S. economy. The S&P GSCI Index, a barometer for the commodity sector, finished the first six months of 2016 up 19.1%, double that of the S&P 500, which rose 9.6% in the same period. In all, investors were reminded of the role natural resources can play in a well-balanced portfolio. Specifically, that natural resources can not only outperform the more broad based market but can also smooth out returns over time since they are less correlated, resulting in a more stable long term portfolio.

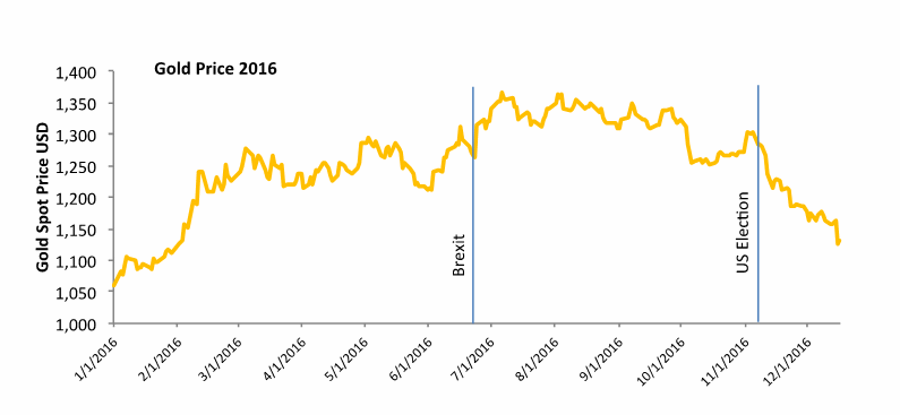

2H 2016 The second half of 2016, with headlines crowded with political surprises on both sides of the Atlantic, gave back many of the gains made. First, the news of Brexit on June 23rd, sent shockwaves throughout the world’s markets, and investors moved strongly to gold as their safe haven asset, trading up an astounding 8.2% in a mere 13 days after the vote to the year’s high of $1366. Silver followed suit. Over the same time period, the GBP/USD plummeted 11% and U.S. 10-year yields dropped almost 20% that night. Anecdotally, this demonstrates gold and silver’s special treatment in the market. Amid growing geopolitical uncertainty, precious metals are seen as not only a safe haven asset, but as liquid currencies as well.

In response to the Brexit surprise, the markets cooled as the world took on a “wait and see” approach. The Bank of England hoping to keep the markets buoyant and calm recession fears, recently announcing a cut in interest rates from 0.5% to 0.25% – a record low and the first cut since 2009. Meanwhile, the U.S. Fed announced a much-expected bump in interest rates in December. As the Bank of England and the Fed diverge in their accommodative approach, we expect continued interest in gold, silver and other safe haven assets as economic uncertainty prevails.

Following the Brexit tumult was the surprise to many of the U.S. federal election in November. Since then, gold, one of the biggest gainers in the first half of the year, has pulled back. Though still up for the entire year, gold has fallen a precipitous 12% since Election Day, down to $1131 by mid-December. There are several likely explanations for the price drop including:

The result of higher metals prices has not had quite the same impact on mining production, but interestingly has sparked a greater number of acquisitions and mergers. Activity increased every quarter of the year, a trend likely to continue into 2017, as there were 121 merger deals in the third quarter of 2016 valued at nearly $8 billion in transaction value. This suggests that, even if miners aren’t yet optimistic enough to invest capital to increase their output, they are seemingly willing to buy that production from juniors and mid-tiers, often a cheaper or quicker way to bring more production online.

The junior miners meanwhile provided the characteristic leverage to the space, beating nearly every other market metric. The Sprott Junior Gold Miners ETF (NYSE: SGDJ) increased a remarkable 150% from December 31, 2015 until its yearly high on August 18, 2016, beating even the performance of the Sprott Gold Miners ETF (NYSE: SGDM), which improved 132% from the end of the year to its high on August 2, 2016.

Predictions for 2017

2016 was a year of volatility for all metals prices, and we expect 2017 to be no different. While this will provide ample investment opportunities for investors in the space it will require us to continue to practice vigilance for the best priced opportunities.

As metals prices were certainly active, political and economic uncertainty is somewhat to blame for the price peaks and valleys, driving some of the speculation in the natural resource space. While many eyes have been on the precious metal space, 2017 is likely to provide some interesting opportunities in bulk materials.

Bulk Materials

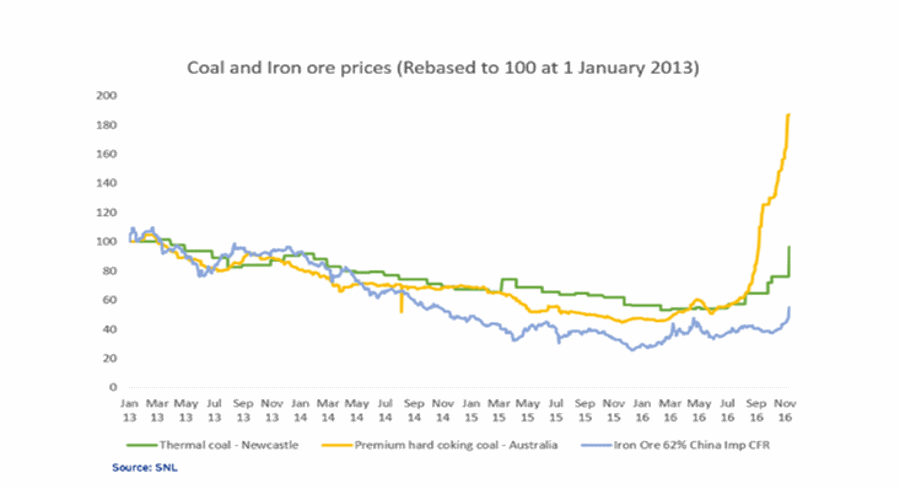

Bulk materials, such as thermal and metallurgical coal, surged in price in the last quarter of 2016 following some supply cutting initiatives in China. Metallurgical coal is up by over US$300/t, and thermal coal has doubled to over US$70/t.[1] China has increased its regulations on coal production, which has led to production cuts and the beginnings of a supply deficit. The country is beginning to demand higher quality coal in order to achieve maximum value. China itself produces mostly low-grade coal, and as supply of low-grade in China has fallen about 6% this year, there may be greater importation opportunities. In fact, with fears of a “hard landing” in China easing, commodity prices in general have bounced off the multi-decade lows we saw in January 2016.

Bulk metals may be getting a bump out of the U.S. as well. As President Elect Donald Trump had proposed massive infrastructure spending and improvements, speculators have been moving meaningfully into iron, copper, aluminum and steel (met coal). Iron ore prices bumped to a two-year high in mid-November. The markets remain somewhat shaky however, as rumors of trade disagreements and protectionism flourish. We have noticed a certain dearth of the availability of copper assets – mines are no longer “on sale”.

Energy

Potentially even more “hated” than miners in 2016 were the energy producers. Similar to bulk metals, prices seemed to have hit a floor in 2016. Natural gas, crude, and even uranium prices all popped toward the end of the year, marking at the very least, a stabilization in the market.

Precious Metals

Since yields and precious metals are generally inversely related, historic low and even negative interest rates in some parts of the world provided a lift for both gold and silver in 2016. The Fed’s predictably hawkish comments in December seem to diverge from the rest of the world’s central banks’ continued accommodative stance.

We believe gold will continue to be viewed as a safe haven asset throughout 2017. In fact, gold investment demand was estimated at 2,024 mt in 2016, a year-over-year increase of nearly 200% since 2015. Conversely, gold fabrication demand was estimated at 2.395 mt, only a 19.4% increase over last year. (Mined supply was only 3,046 mt, by the way, already not enough to appease total demand)[1]. What appears to be changing is the consumer’s appetite for how to hold onto gold.

Conclusion

While political predictions are not our specialty, it’s not difficult to foresee that 2017 will be an interesting year for public officials across the globe. Economically, the impact of the world’s central banks on the market’s psyche is starting to erode. Their policies are beginning to diverge, particularly in the developed world, as the U.S. outstrips growth in Europe and developed Asia. China, which has become a major catalyst for many metals prices, appears to have stabilized after a hectic 2015, and the monumental consumption pace of its people seems set to continue for the foreseeable future, albeit at a slower pace.

We know that the natural resource sector requires greater patience and often more research than the typical investor is willing to expend. We thank you for placing your trust in us to help you navigate this space.

Natural resources have historically shown a low correlation to traditional asset classes. Additionally, precious metals have served as a historical store of value which is why we believe they should be an integral part of a well-structured and diversified portfolio.

On behalf of all of us here at Sprott, thank you for another year with us. We look forward to a prosperous new year, and offer our best wishes to you and your families.

Robert V. Villaflor

CEO, Sprott Global Resource Investments & Sprott Asset Management, USA

[1] http://www.ey.com/gl/en/industries/mining—metals/ey-mining-and-metals-trends-and-updates#gold

[i] Data to support the above claims can be found here: Timber, WTI Crude, Corn and other grains

This information is for information purposes only and is not intended to be an offer or solicitation for the sale of any financial product or service or a recommendation or determination by Sprott that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the objectives of the investor, financial situation, investment horizon, and their particular needs. This information is not intended to provide financial, tax, legal, accounting or other professional advice since such advice always requires consideration of individual circumstances. The products discussed herein are not insured by the FDIC or any other governmental agency, are subject to risks, including a possible loss of the principal amount invested.

Generally, natural resources investments are more volatile on a daily basis and have higher headline risk than other sectors as they tend to be more sensitive to economic data, political and regulatory events as well as underlying commodity prices. Natural resource investments are influenced by the price of underlying commodities like oil, gas, metals, coal, etc.; several of which trade on various exchanges and have price fluctuations based on short-term dynamics partly driven by demand/supply and nowadays also by investment flows. Natural resource investments tend to react more sensitively to global events and economic data than other sectors, whether it is a natural disaster like an earthquake, political upheaval in the Middle East or release of employment data in the U.S. Low priced securities can be very risky and may result in the loss of part or all of your investment. Because of significant volatility, large dealer spreads and very limited market liquidity, typically you will not be able to sell a low priced security immediately back to the dealer at the same price it sold the stock to you. In some cases, the stock may fall quickly in value. Investing in foreign markets may entail greater risks than those normally associated with domestic markets, such as political, currency, economic and market risks. You should carefully consider whether trading in low priced and international securities is suitable for you in light of your circumstances and financial resources. Past performance is no guarantee of future returns. Sprott, entities that it controls, family, friends, employees, associates, and others may hold positions in the securities it recommends to clients, and may sell the same at any time.