Uranium up!

Uranium has made a decided move up in the last few sessions. Could this be the start of something big?

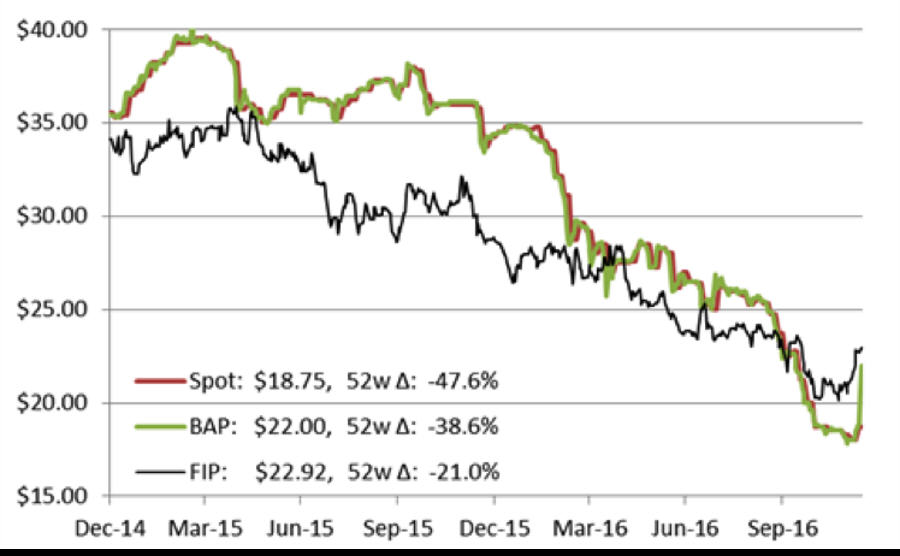

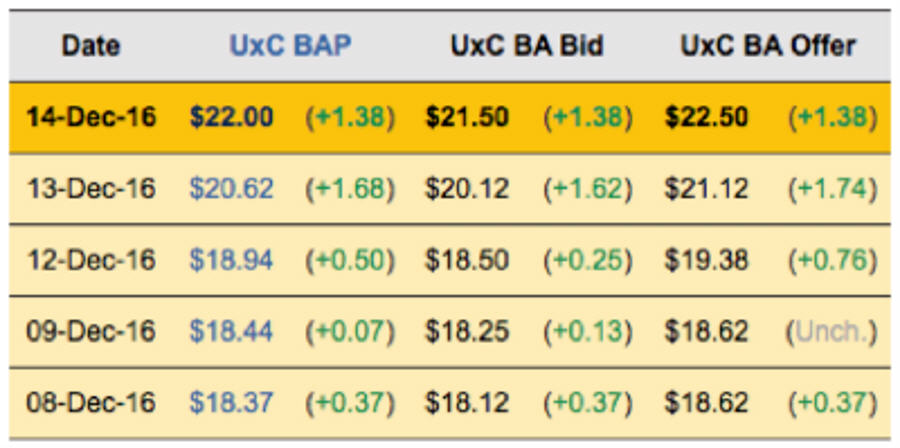

Perhaps. The Broker Average Price (BAP) of uranium is up 19.3% in the last three days, including a 9% move on Tuesday night that represented the biggest one-day uptick in 2.5 years. The BAP finished today at US$22 per lb. U3O8, up $1.38 per lb. on the day.

We quote the BAP when talking daily moves because the spot price is only reported weekly. Its last number came out on Monday at $18.75 per lb. The BAP is calculated from the daily bids and offers as posted by two major uranium market players and it is the only estimate available for daily changes in the spot uranium price.

You can see the moves in the BAP in this table of prices, bids, and offers.

The moves come off last week’s new 12-year spot price low of $18 per lb.

Contrarian investors seem to think this is the bottom. Uranium equities started moving up two weeks ago and Uranium Participation Corp (TSX: U), which simply owns uranium to give investors a way to get exposure to the commodity, is trading at an almost 20% premium to spot.

In other words, investors are willing to pay a premium of almost 20% to get exposure to physical uranium at this level. That premium – paying $3.90 per share of U – values the company’s uranium holdings at $22.68 per lb. U3O8.

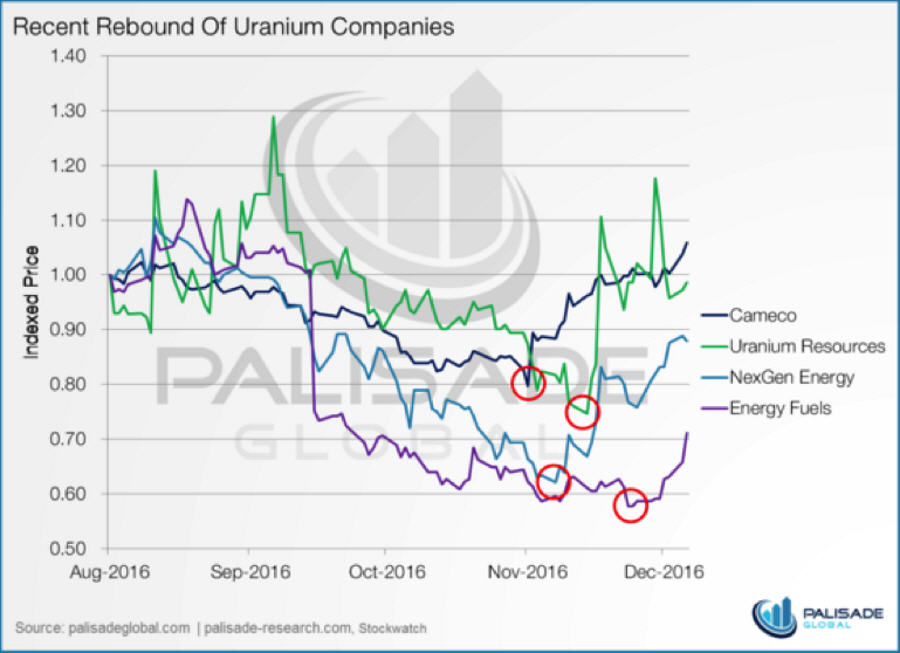

U isn’t the only uranium equity feeling the love of late. This chart from Palisade Global highlights a few rising uranium stocks.

What gives? The obvious force is Trump. The United States is the biggest uranium consumer in the world and Trump’s pro-nuclear stance is having an impact. The President Elect has voiced his direct support for nuclear energy many times in the past and his approach to the Environmental Protection Agency is likely to help uranium miners, developers, and consumers.

One specific example: President Obama and Democratic Senator Harry Reid have actively opposed the Yucca Mountain nuclear waste site, which prevented the facility from opening. That will likely change with their departure, giving nuclear plants clarity on where they will store spent fuel going forward.

I know that seems like a detail, not the kind of thing catalyst needed to reverse uranium’s nine-year price slide. But changing sentiment in America could actually be that catalyst.

Uranium has not been the most logical market. Most people blame Japan for uranium weakness, pointing to excess supply in the spot market since Fukushima forced the shutdown of all of Japan’s reactors as the problem. And yes, Japan has been a major overhang. But it is very hard to know exactly how much Japan has added to spot supplies.

Secondary uranium supplies are a murky market to start, so tracking is tough. Then there’s the fact that Japanese utilities usually bundle uranium into the specific packages needed by each reactor shortly after they take deliver. To disassemble those bundles and generate sale-able uranium again – prices have been so low that it’s difficult to see it being worth it.

Not knowing exactly what Japan is doing with its excess uranium is possible because the entire market for secondary uranium (everything that doesn’t come directly out of a mine) is so opaque. There is supply from downblending old warheads and from upgrading previously processed supplies and from stockpile sales, but figuring out how much there is and what is happening with it is very difficult.

Utilities add to uranium’s illogical-ness. Uranium is ridiculously cheap right now. Are utilities taking advantage and buying? Nope. They are all buying from the spot market to supplement contract supplies, complacent in their current low costs while unfilled needs in 2019 inch closer and closer.

Those needs are real. Utilities cannot run out of uranium – that’s when nuclear reactors melt down. Not an option. The absolute need to have fuel is why utilities usually cover all of their requirements at least three years out and often as much as ten years out.

Right now they are unusually uncovered two years out…which is right when increasing Chinese demand and sliding production because of a lack of investment in new mines means the world starts to run short of uranium.

That means utilities need to sign new contracts.

Nuclear utilities operate as a herd. It’s amazing, actually, how they all move as one. So we will know the uranium boom is starting when we see the first few new contracts.

Soon after that will come a flood of contracts. Sellers understand this situation very clearly – and will crank up prices. They know as well as anyone that supplies will be limited from 2019 forward and they will use that fact to justify higher prices.

So this jump in the BAP is a good start. Next we want to see the jump realized in a higher spot price on Monday and continuing up from there. Third we want to see new contracts signed, which will push the contract price up. That third event is possible in January, which is a classic uranium contracting season.

These oddities in the uranium sector – the herd mentality of buyers, the lack of information on secondary supplies, the overhang of social and political pressures – these all generate a market with the potential for incredible price spikes.

In 2003 uranium cost $9 per lb. Over the next four years it shot up 1300% to reach $130 per lb. That is the kind of price move that is possible with uranium. Then imagine the gains that uranium explorers, developers, and miners offer when that happens.

I am not ready to say that uranium has bottomed and its skyward from here, but it is very heartening to see these price gains, especially since uranium equities led the increase. That’s a classic pattern when contrarian investors step in. Now we watch for:

1. These gains to hold up, and continue.

2. Utilities to start signing contracts, boosting the contract price.

Once both of those requirements are met, it will be game on.

More News

US delays Canada, Mexico tariffs

The announcement comes a day after Trump gave a 30-day tariff reprieve to the big three automakers.

March 06, 2025 | 02:23 pm

Video: Seabridge CEO on KSM progress, questioned permits

The project, in the Golden Triangle of British Columbia, is one of the world’s top undeveloped gold deposits.

March 06, 2025 | 01:34 pm

Video: VRIFY’s new AI tool cuts exploration timelines from weeks to seconds

The platform provides real-time probability and variance metrics, which, VP says, challenges the old geological bias.

March 06, 2025 | 12:47 pm

{{ commodity.name }}

{{ post.title }}

{{ post.excerpt }}

{{ post.date }}

Comments