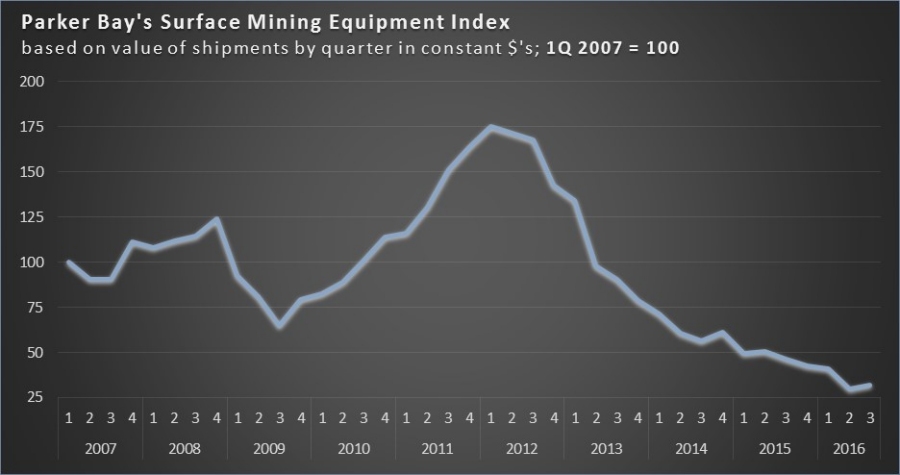

Parker Bay’s Mining Equipment Index showed a gain of 6.5% (US$-weighted basis) for the third calendar quarter of 2016 vs. comparable deliveries during the second quarter of the year. On an unweighted basis (number of units delivered), the gain was much more impressive at 13%. The difference reflects the much greater gains for smaller machines (though still large by most standards). While these figures are encouraging, in part they reflect the extraordinarily low level of shipments in the first half of this year. Even with further gains in Q4, full-year 2016 shipments are likely to fall below the already depressed 2015 level. But combined with other measures of mining market activity, these gains may be the start of an industry recovery.

The Index, which tracks shipments of only the largest mobile equipment delivered to the largest surface mines worldwide, covers mines and machines that produce a significant (and in some instances a majority) share of the world’s coal, copper, iron, gold and other minerals. It is believed to be representative of the mining industry’s new equipment purchasing activities as a whole. But it does not take into account used equipment that mines have removed from service and reapplied either at their own operations or through resale. This secondary market has accounted for a substantial share of miners’ capacity additions during the current industry down-cycle, and some measures of this market also show signs of improvement.

Deliveries of large mining trucks, by far the largest component of the Index, increased by 16% over second quarter shipments. But the average payload of these units was 14% smaller than that of units shipped during 2011-2015 and the number of ultra-class trucks (290-mt payload and greater) declined to just 18 units in Q3 – one-fifth of the quarterly rate since 2011. In contrast there was no sign of recovering shipments of large excavating/loading equipment with Q3 deliveries modestly below the numbers achieved in the first half of the year. As with the trucks they are paired with, the average capacity of these loading tools fell roughly 10% below historical averages. Other mobile equipment in the Index showed significant gains vs. Q2 with shipments of large dozers increasing by more than one-third. However, these gains left them modestly below the Q1 level.

Recent shifts between regional mining markets are substantial The largest mining regions – Australasia, North and Latin America – accounted for nearly 60% of global demand over the past five years, but just 45% of deliveries year-to-date and 35% of Q3 shipments. In contrast, mines in Asia and Russia/CIS accounted for fully half of Q3 shipments vs. just 25% of the market over the past five years. Significant gains have been recorded to Indian coal customers and to Russian miners of several major minerals. But owing to the short time-frame and low level of shipments, conclusions about possible long-term shifts among regions are tenuous at best.

After experiencing major contraction across virtually all regions and countries, coal mining resumed its position as the largest single mineral sector accounting for more than 40% of Q3 deliveries. Demand was concentrated in India and Indonesia, both sectors heavily dependent on utility coal demand rather than the recently ebullient met coal market. Mines supplying the latter product have not yet been compelled to add new equipment but may be doing so the near future in response to sharply higher prices and the reopening of mines that had been placed on ‘care-and-maintenance’.

Among the major metals, iron ore shipments rebounded in Q3, but for the year as a whole, deliveries to gold mines have outstripped those to the typically larger copper and iron sectors. Demand from Canadian oil sands miners remained depressed, reflecting weak oil prices and reduced miners’ capex. But a cycle of replacement of existing fleets appears to be underway, including a potentially large number of autonomous-drive haulers slated for delivery over the next several years.

Interested parties are encouraged to contact Parker Bay at [email protected] or by visiting the Company website www.parkerbaymining.com. Additional details on the Surface Mining Equipment Index are available at: http://parkerbaymining.com/industry-information/surface-mining-equipment-index.htm