Iron ore weakness to continue into 2025 and beyond, says Fitch Solutions’ BMI

Looking beyond 2024-2025, BMI analysts maintained their view that iron ore prices will likely follow a multi-year downtrend.

The China Lithium-Ion Battery market has seen a massive surge in growth over the last years, with a CAGR in excess of 50% since GCiS’ previous research conducted in 2011. In our 2015 update, this rapid growth has been driven primarily by EV (Electric vehicle) subsidies. The result has been a shift in emphasis away from 3C (Computers, Cell Phones, Consumer Electronics) applications. Said EV applications have driven a surge in market size and the hype surrounding EV applications has led to the potential for substantial overcapacity.

The upstream market (cathode material) is currently in a state of oversupply, but the increased capacity expansion amongst LIB suppliers means that this overcapacity will be steadily chipped away over the next few years. Almost all the leading LIB suppliers are expanding production capacity in NCM, LFP or a combination of the two. This article discusses the drivers behind current lithium-ion battery exponential growth and examines its future sustainability.

This market research conducted by GCiS in 2015 covers the four main types of LIB used in China: Lithium Cobalt Oxide (LCO), Lithium Iron Phosphate (LFP), Nickel Cobalt Manganese Oxide (NCM), and Lithium Manganese Oxide (LMO). These products only include the cells themselves, and do not include battery packs or systems, as well as battery management systems. The research also investigates in depth the upstream cathode materials market in China for each of the four LIB cathode materials.

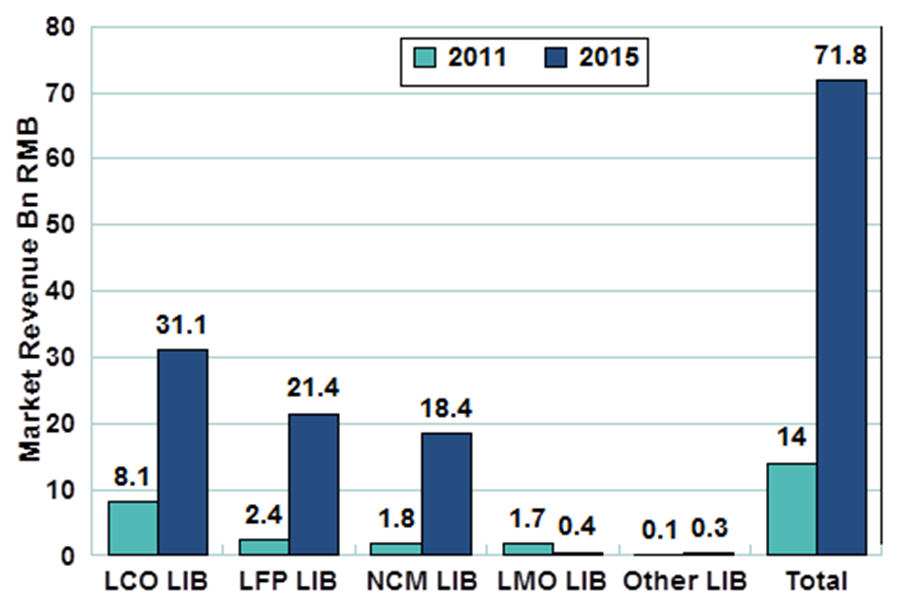

The development from 2011 to 2015 shows substantial growth overall in addition to the development of the EV segment. What really stands out is the stark contrast between the size of the LIB market in 2011 and 2015. The 2011 total market size was RMB 20.6 Bn, while the domestic market was RMB 14 Bn. In 2015 the total revenue market size was RMB 106 Bn and the domestic market size was RMB 71.8 Bn. For the domestic market only, this is an increase of 413%, with a CAGR of 50.5%.

Of the four battery types, LCO had the largest market share at 58% of the total domestic market, while LFP, NCM and LMO had revenue market shares of 17%, 13%, and 12%, respectively. Looking at the market in 2015, little has changed in terms of the relative position of the different battery types.

Chart 1: Domestic Revenue Market Share by Battery Type – 2011 & 2015

source: GCiS

The Power of Policy

LIBs in China are at the confluence of two very strong and deep-seated goals of Chinese policy makers. The first goal is to reduce pollution across China, and one part of this goal includes reducing pollution from motor vehicles. The other is the stated goal of the Chinese government to move manufacturing in China up the value-chain: from low-cost, low-tech products to products that require higher levels of skill and technology to produce. One of the 10 industries mentioned in the Made-in-China 2025 program – a policy that outlined the sectors target for a manufacturing upgrade – is new-energy vehicles and equipment, the former is a main downstream market of the LIB manufacturing industry. The figures show how this policy has been put into practice: the EV sector has grown from having a 10% revenue market share in 2011 to having a 34% share in 2015, making it the largest single downstream sector of LIBs in China.

This dramatic growth has been accomplished through subsidies from the government to stimulate demand for EVs. The result of these subsidies is a massive boost to sales of commercial and passenger BEVs (pure Battery Electric Vehicle). PHEVs (Plug-in Hybrid Electric Vehicles) are also a feature of this market, but currently their market share is well behind that of BEVs. In 2015, the total sales volume of EVs was 331,092 vehicles, which is 3.4 times the amount in 2014. The 2015 sales volume market share segmented by type was: BEV passenger vehicles 44%; BEV commercial vehicles 31%; PHEV passenger vehicles 18%; PHEV commercial vehicles 7%.

The current situation did not come about by accident. The subsidies for 2016 issued by the Ministry of Industry and Information and Technology (MIIT) give higher amounts to BEVs than PHEVs. The highest available subsidies for passenger vehicles are RMB 55,000, and RMB 500,000 for commercial vehicles. In comparison to this, the highest available subsides for passenger PHEVs are RMB 30,000, and RMB 250,000 for commercial vehicles.

Chinese EVs have received a lot of attention for its high growth, but there are serious and persistent questions regarding the quality of this growth. An in-depth look at this sector throws up some warning signs. Currently demand is driven by government subsidies, and this has caused EVs to grow rapidly, but the quality of the cars being produced is under question. Most of the EVs being produced by a lot of Chinese manufacturers are small-scale vehicles that are nowhere near the large passenger cars that are common with gas engines. The lack of larger saloon, sports cars and SUVs is shown by the sales volume market share going to smaller vehicles (A0 class – wheel base 2.3-2.45m & A00 class vehicles – wheel base 2-2.2m) which was 90% of all passenger BEV sales in 2015. This suggests that domestic EV manufacturers are trying to take advantage of generous subsidies by producing low-quality, small cars. This potentially indicates that when subsidies are reduced in 2017 by 20%, and again by 40% in 2019, the rapid growth of the EV sector, as well as demand for NCM/LFP LIBs may drop.

Another issue has been widespread subsidy abuse. One telltale sign of subsidy abuse is massive spikes in output just before subsidies are set to expire (or be reduced). Notable examples of this are the production spikes in November and December 2015, with the combined EV output for these two months reaching 48% of the total EV output in 2015. The subsidy program that ended in 2015 was more generous than the newly established one, with total subsidies falling by at least RMB 5,000/unit. There are also questions regarding the accuracy of production numbers, as several substantial cases of subsidies being paid for undelivered vehicles have been uncovered. The upshot of this is that when subsidies are lowered in 2017, and again in 2019, the high pace growth and sales seen in 2014 and 2015 are likely to fall. There may be tighter regulations even sooner than 2017 in light of the subsidy abuses.

Another area of policy emphasis and market buzz is the energy storage sector, both on and off-grid. Development here has been slow, and looks to remain such for the foreseeable future. LIB’s role in primary frequency regulation is very limited. Barriers to grid access are substantial in technical, economic and political terms. Storage application subsidies are low, and kWh costs from storage systems higher than peak-to-trough spreads. There are a variety of small scale distributed PV system demonstrators and a number of companies are competing in test and demonstration projects for connecting Wind and PV farms to the grid, but low feed-in tariffs and the less-than-enthusiastic cooperation of the State Grid prevent commercial scale installations.

While real questions regarding EV energy storage remain, other more traditional sources of demand remain important. The 3C sector (Consumer electronics, Cell Phones, and Notebook Computers) is still the largest source of demand, taken together these three sectors account for 53% of total market revenue. Although total growth for these 3 sectors is relatively stable, there is still some expansion, and while these will not drive strong total growth, the large size of these markets will ensure a stable source of demand for battery suppliers.

The Upstream Squeeze

There are several stages to the LIB value chain, and these all have a large impact on the price of LIBs. The first stage is the mining of the cathode raw materials, such as Lithium, Cobalt, Nickel, Iron, and Magnesium. There are less than 10 major suppliers worldwide that are capable of extracting these minerals, and processing them for further sales. The relatively high concentration and large, growing demand mean that these companies have a fairly tight stranglehold on prices, and can raise them without fear of a backlash. For example the price of Lithium Carbonate, one of the main input materials at the cathode materials processing stage, has increased in price by 250% compared with Feb 2016. Lithium Carbonate is not alone in seeing large price rises: Lithium Hydroxide has seen steep price increases according to industry sources. These prices will remain the same for the near future, as China relies on Lithium imports, and although it has large domestic reserves these are not being developed.

Cathode materials processors in China show the classic symptoms of overcapacity. Downstream demand has not kept pace with investment, while supplier prices have held steady. The squeeze is on. They have been able to pass some of this on to the LIB manufacturers, who are have also overinvested. Thus the squeeze on margins is seen up and down the manufacturing chain. Short of much more rapid market acceptance, there is serious consolidation in the making.

Costs for other components of the LIB chain are mixed, with some prices dropping while others have risen. Of the big four costs of a LIB – Separator, Cathode Material, Anode Material, and Electrolyte – manufacturing costs for separators and anode materials fell early 10% and 20% respectively over 2015. However there have been cost increases in the manufacturing costs for cathode materials (10%) and the electrolyte used for batteries (15%). Like the cathode materials market, cost of electrolytes has been affected by the price of Lithium Carbonate which is used in the production of one of the key inputs for manufacturing electrolytes: Lithium Hexafluorophosphate. This cost accounts for about 35% of the total cost for electrolytes, so any change in price will have a large effect on the overall cost of electrolytes. Despite this price rise, as the cost of electrolytes is about 9-13% of the total cost of the battery, price fluctuations will have only a moderate effect on the overall cost of LIBs.

Capacity Expansion

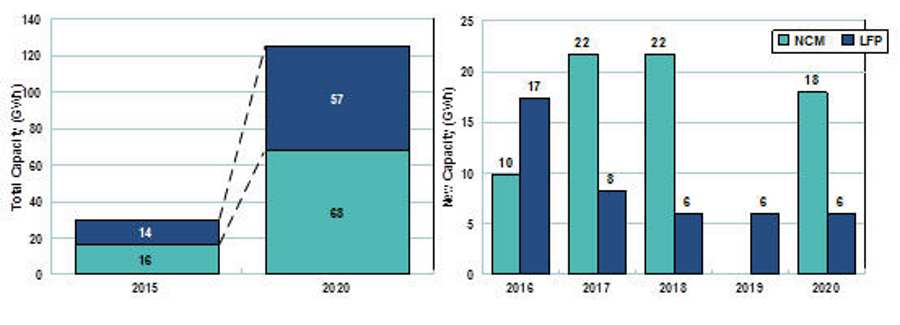

There has been and will continue to be a vast swathe of capacity expansion across the two main LIB segments: LFP and NCM. Currently total market capacity is roughly 55 GWh, and major market players plan to increase capacity by 109 GWh between 2016 and 2025. Domestic companies are increasing their capacity in both the NCM and LFP segments, but the majority are focusing on LFP. Foreign companies on the other hand are almost exclusively expanding their NCM capacity. Both LCO and LMO will see no capacity additions, due to their low levels of growth. In addition, due to cost advantages, LCO is slowly being replaced by NCM batteries. The net result of this capacity expansion will be an increase in the total LIB capacity by over double its current size. The capacity is set to come online between now and 2025, with most scheduled to be finished before 2020.

Many domestic suppliers are expecting that the government’s EV capacity goal will be met. They believe that current capacity will not be able to meet this demand. They further believe that the resulting economy of scale will further increase LIB demand through lower prices, enabling the widespread adoption of BEV.

Figure 2: Capacity Expansion (2016-2020) by Battery Material Type

Source: GCiS

Most new planned capacity will be LFP, with the sole exceptions being in 2018 and 2020, where NCM has the larger share of new capacity addition. The large amount of new capacity added so quickly leaves several segments exposed to the risk of overcapacity. Currently the segment that has the highest risk of overcapacity is LFP. This is due to the EV sector making up over 3/4 of total segment revenue. If the status quo remains the same then there should be no problem, and there may even be a need for additional capacity expansion. However, the drop in subsidies scheduled in 2017 and 2019 may heavily reduce EV demand growth, dealing a strong blow to total segment growth.

Another factor determining the extent of the growth of the EV sector is the coverage of the charging station network. Currently there are 26,000 charging poles in China, which are scattered throughout major cities in China. According to recently released policies like “Guidance and Suggestions on Speeding up the Construction of Electric Vehicle Recharging Infrastructure”, the government aims to have 4.8 Mn charging poles by 2020, equivalent to adding early 1 million charging poles every year from 2016 to 2020, and roughly 12,000 charging stations constructed by 2020. It remains to be seen whether or not this target will be achieved, and even if it is, it will still be a few years before the infrastructure is in place.

With this rate of capacity expansion, GCiS expects capacity utilization will drop from current high of 90% to 75% by 2020. This is the best case scenario under the circumstance that EV production and sales will reach government targets. If, due to drop in subsidies and insufficient infrastructure, such projections do not come to pass, there will be heavy overcapacity as LFP LIB manufactures see their main downstream market shrink. The NCM sector is also exposed to the EV sector, but not as heavily as the LFP segment. Less than half of the total NCM segment revenue is from the EV sector, and the continuing replacement trend of LCO LIBS in 3C products by NCM means that there will still be growth in key downstream markets should EV sector growth be curtailed.

Conclusion

The key takeaways from the LIB research are two. First, the market is far from maturity and as demand segments continue to develop, further impressive growth can be expected.

Secondly, the LIB industry in China does not exhibit much technical innovation and all raw materials are imported. Thus they are dependent upon the success of government policies. The path forward is seen as large scale manufacturing to drive costs and expansion plans universally depend on the continued success of government support policies.

Thus, in conclusion we can anticipate an upcoming industry shakeout where many marginal players will be unable to compete with larger and state-sponsored competitors. Vertically integrated competitors of substantial scale will also fare better. This will happen regardless of the success, or lack thereof, of government policies in the EV sector.

Additionally, there is a real risk that current capacity expansion will be far in excess of actual demand as government policies continue to face market realities. The government has found it possible to spark the initial rounds of development through a wide variety of policy supports, including large direct per-vehicle subsidies. There are real questions as to whether this can be sustained financially and technically. If not, LIBs may join the ranks of PV and LEDs as promising new technologies that over-invested.

By Jessie Jiang, Senior Analyst at GCiS China Strategic Research

About GCiS China Strategic Research

GCiS (www.GCiS.com.cn) is a China-based market research and advisory firm focused on business to business markets. Since 1997, GCiS has been working with leading multinationals in sectors including industrial and machinery products, chemicals, power and resources, building and constructions and a few others. This article is based on a recently published China lithium-ion battery market report.